PGIM Sees Twin Forces of Stimulus Upending Stock-Bond Link

PGIM Sees Twin Forces of Stimulus Upending Stock-Bond Link

(Bloomberg) -- The combined forces of central bank and government stimulus could shake up the relationship between stocks and bonds that’s helped make the 60/40 portfolio an investing stalwart, according to asset manager PGIM.

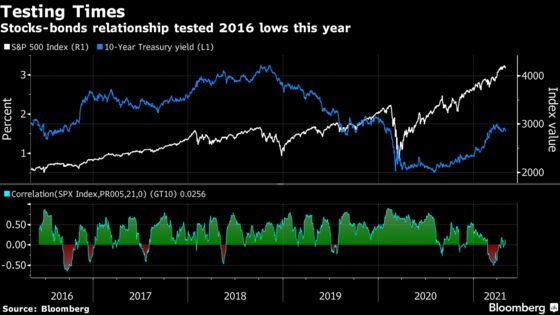

For the past couple of decades, bond-market gains have helped to offset losses on risk assets -- hence the popularity of the equities/bonds split in the traditional strategy. Coordinated policies to spur economic growth could upset that balance, causing both markets to move in the same direction, and shaking up asset allocations across the industry. That’s the view from a research paper by Junying Shen and Noah Weisberger at PGIM’s institutional advisory and solutions group.

“Currently, both fiscal and monetary policy settings seem to be in flux and may echo policy regimes of an earlier era less familiar to today’s CIO,” the analysts wrote. “Increases in the debt-to-GDP ratio harken back to the late 1960s and 1970s, which would tilt the balance of risks toward higher interest rates, lower growth, and positive stock-bond correlation.”

That’s not to say that PGIM expects worse times ahead for the traditional portfolio. It’s simply that investors should be alert to the risks of a regime shift. “A return to positively correlated stock and bond returns may require CIOs to rethink their asset allocation,” the paper advises.

This latest research comes at a tough time for the 60/40 portfolio’s reputation, as critics have argued that the slide in bond yields to historic lows in recent years made them ineffective hedges. The strategy’s losses in 2018 led to increased calls for an overhaul -- the latest suggestions include adding derivatives or even Bitcoin to counter inflation risks. The volatility stirred by sharply higher growth expectations of late has provided another test, though the strategies tracked by Bloomberg are in the green year-to-date, including close to a 5% gain for the global portfolio.

The market outlook is complicated by uncertainty over the path of growth and inflation as policy makers around the world struggle to get the pandemic under control and spur a recovery.

“The difficulty we have, if we think about forecasting regime changes, we’ve only seen three regime changes in the last 70 years after regimes that lasted a very long time,” Weisberger said in an interview. “But when it shifts, it does shift.”

The report simulated a range of outcomes for a balanced portfolio with unchanged expected returns. If correlations turned positive, the research showed a manager with a 60/40 portfolio might have to lower the stocks weighting to as little as 40% to maintain the same level of risk.

“If you are a multisector investor the biggest risk that you run is that correlations go positive, where you lose money on both risky assets and your rates positions,” said Pilar Gomez-Bravo, director of fixed income at MFS Investment Management in London.

One key indicator for investors to watch is how interest rates are behaving relative to changes in economic growth, Weisberger said. Artificial suppression of interest rates to engineer growth and higher inflation could lead to higher interest-rate volatility, in his view.

“A shift from negative to positive stock-bond correlation means that stocks and bonds no longer hedge each other,” which could boost the volatility and risk of losses for a balanced portfolio, the paper noted.

©2021 Bloomberg L.P.