Paying 10% Dollar Yield, Obscure Vale Bond Is Now Talk of Brazil

Paying 10% Dollar Yield, Obscure Vale Bond Is Now Talk of Brazil

(Bloomberg) -- It’s a very odd security, technically a perpetual bond from Vale SA that pays out when the Brazilian mining giant’s ore output reaches certain thresholds. And for years, few in Sao Paulo financial circles seemed to notice it, with prices stuck at just a few cents in thin trading.

But investors are giving the notes a fresh look, and prices are soaring. The appeal is that while the bonds are sold in the local currency, the payout is based on Vale’s dollar revenue. That means securities from an investment-grade company will pay a dollar yield of about 10% this year, an almost unheard of figure in a world where global central banks have done their best to hold down interest rates.

Now, a fresh supply of the notes is about to hit the secondary market, increasing liquidity and providing an opportunity for new investors to jump in just as prices for industrial metals seem on the cusp of a new supercycle. Brazil’s government and state development bank BNDES, which own about 55% of the outstanding amount, plan to sell their stake next month, worth about 12.9 billion reais ($2.24 billion) at current prices. It’s part of a plan to shed state assets championed by Economy Minister Paulo Guedes.

“The notes are very attractive right now,” said Ulisses de Oliveira, a money manager at Sao Paulo-based Quasar International Cap Mgmt Ltd., which owns the debt. “The BNDES sale brings liquidity to the trade.”

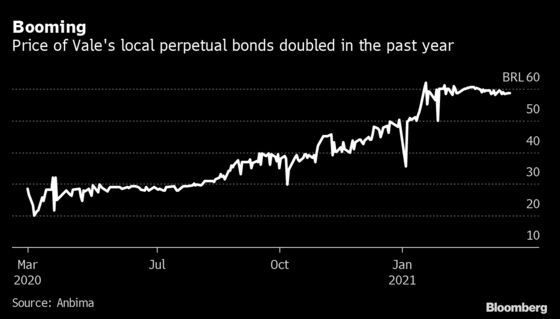

The securities now fetch almost 60 reais after more than doubling over the past 12 months, according to data compiled by Anbima, the country’s capital markets association.

The notes were issued with a face value of 0.01 real each in 1997, just before Vale’s privatization, with owners given one for each equity share they held. The idea was that investors would be directly rewarded as Vale ramped up production, and would get windfall payouts in years when output and metals prices were particularly robust.

The notes don’t have a fixed coupon and instead pay holders a dividend equal to 1.8% of net revenue from some iron-ore sales and 2.5% of net revenue from copper and gold after certain production thresholds are met, some of which are tied to where the ore is being mined. The revenue is calculated in dollars, then converted to reais for the distributions to investors.

While output thresholds haven’t been reached in the region that encompasses southern Brazil after a deadly dam rupture in Minas Gerais curbed production, the northern region alone is providing bondholders with attractive yields, according to Oliveira. In October last year, Vale payed 1.27 reais per note in dividends. The first payment this year will be for 2.76 reais on April 1, and Oliveira estimates a payment of at least 3 reais this October, which would provide a dollar yield of 9.6% given a price of 60 reais for the security.

That’s an extraordinary level when considering that Vale’s longest term overseas bonds, due in more than 20 years, yield just 4.2%. The perpetual notes also pay more than three times the 2.8% average dollar yield for emerging-market companies rated in the BBB bucket, according to data compiled by Bloomberg.

With an increase in production volumes at Vale’s northern mines and considering the 80% jump in iron-ore futures over the past year, the securities represent a great value, according to Jorge Junqueira, a partner at asset management firm Gauss Capital Gestora de Recursos Ltda., which owns the notes.

“Those notes are very peculiar, and some time ago there was a total lack of knowledge of those assets, even from some of Vale’s top equity analysts,” he said. “With the dollar at this level, this asset is very interesting for investors.”

Of course the payouts to noteholders are painful for the Rio de Janeiro-based company. Chief Financial Officer Luciano Siani Pires said in a conference call with analysts in October that Vale planned to repurchase the securities at some point, a prospect that concerns bondholders since it could reduce liquidity.

At a bondholder meeting March 19, the government and BNDES voted their majority stake in favor of changing the clauses of the securities -- without paying any compensation to bondholders -- so that Vale can repurchase them. Oliveira and Junqueira say they voted against the proposal and now that it was approved are considering legal options to try to revert the decision.

In a emailed response to Bloomberg, Vale said repurchases aren’t a priority for now, and it would do “a public and transparent” tender offer if it decides to buy back the notes in the future. It said capital market regulations forbid the company from bidding on the notes being sold by the government and BNDES next month, and also don’t allow Vale to buy the securities slowly on the secondary market, denying speculation it was doing so.

BNDES, also based in Rio de Janeiro, mandated banks in September to organize the sale, with presentations to investors running from March 30 to April 9.

“If Vale wants to buy back the notes, they will have to come up with a very attractive proposal,” Oliveira said.

©2021 Bloomberg L.P.