Palladium’s Hot Run Turns Cold in Metal’s Biggest-Ever Turnabout

The Coronavirus outbreak has crushed the demand prospects for one of the best performing commodities of 2019.

(Bloomberg) -- During market crashes, palladium isn’t the first commodity that comes to mind.

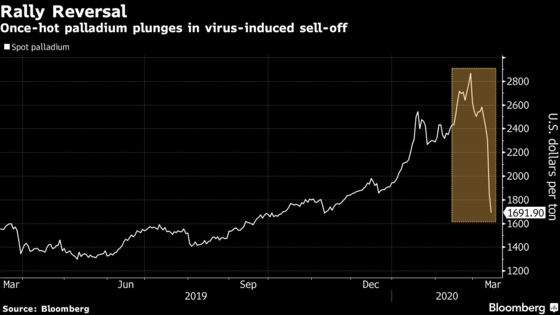

That’d typically be reserved for gold, the oldest of all safe havens, or maybe oil, a notoriously volatile asset. But while those two have garnered plenty of attention this week, no commodity has cratered more spectacularly than palladium, stunning investors with a 30% plunge that included a 20% drop in one day alone in the spot market. Futures on Friday tumbled as much as 24%.

Palladium’s dramatic ascendance in the past 13 months has turned into an equally shocking rout as the coronavirus outbreak crushes demand prospects for the metal used in cars. After fears of supply constraints sent palladium cruising through multiple record highs, making it one of the best performing commodities of 2019, concerns about auto sales sent the metal plunging into a bear market. And the fall continued Friday.

Palladium’s sell-off “was really just a good reflection of the overall panic in the market,” Ole Hansen, head of commodity strategy at Saxo Bank A/S, said by phone Friday. “I think it’s pure and simply telling the story of a typical CTA or a hedge fund -- they are selling the momentum.”

Prices slumped 20% on Thursday, the most on record, and the metal used to curb emissions from gasoline-fueled vehicles has lost almost a third of its value this week. Its rally has reversed as slumping car sales in China signal weakening demand from automakers and fears of the impact of the coronavirus hammer commodities.

Palladium made a U-turn after surging by more than half last year, the most in a BNP Paribas gauge of commodity returns. By Friday, spot prices were down about 12% this year.

The difference between the high and low on Thursday was $663.57, the most in records going back to 1993. The unraveling comes after the metal surged 88% in 12 months to an all-time high in late February.

Hansen says investors are probably still bullish on palladium’s fundamentals. The market has been in a deficit since at least 2012, but that demand overhang is expected to shrink to 125 million ounces from 2019, Citigroup Inc. analysts said Thursday in a research note. The bank lowered its price forecast on the metal by $100 an ounce for 2020.

The market, largely reliant on Chinese auto sales, has been hit by expectations of weaker industrial demand and slowing car sales as consumers stay home amid the spread of the coronavirus globally. That’s led hedge funds to slash bullish bets on the metal to the lowest on record in the week ended Tuesday, according to U.S. government data.

Spot palladium fell as much as 12% on Friday before paring losses to 2.1% and closing at $1,812.82 an ounce. Futures for June delivery slid 21% to settle at $1,509.10 an ounce on the New York Mercantile Exchange.

--With assistance from Eddie van der Walt and David Papadopoulos.

To contact the reporter on this story: Justina Vasquez in New York at jvasquez57@bloomberg.net

To contact the editors responsible for this story: Luzi Ann Javier at ljavier@bloomberg.net, Joe Richter, Pratish Narayanan

©2020 Bloomberg L.P.