Painful Shorts Don’t Mean That All Bets Are Off

Painful Shorts Don’t Mean That All Bets Are Off

(Bloomberg) -- The European market is hovering near its 2019 high, buoyed by central banks’ dovish tone and resumed U.S.-China trade talks. But short covering is also lending support to the market. Over the past two weeks, there’s been a near $10 billion drop in the total value of Stoxx 600 shares out on loan, representing a 7.8% decline in the overall value of short-selling bets, data from IHS Markit show. Should a full capitulation by short sellers happen, it could trigger erratic moves, particularly for single names.

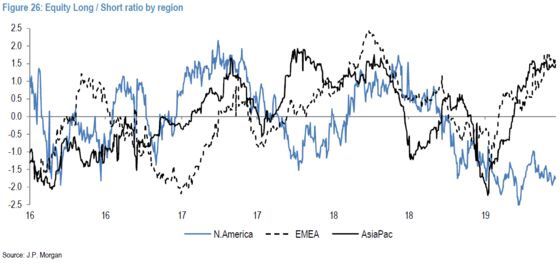

According to JPMorgan data, the equity long/short ratio for their prime brokerage clients has returned to a relatively high level at about 1.5, similar to early 2018. By contrast, the ratio has stayed negative for U.S. stocks.

The case for European equities has continued to build, especially on a relative basis. Yesterday, Morgan Stanley strategists cut their global equity allocation to underweight on growth concerns, but said that European equities may outperform given their low positioning, valuations and “less bad” macro and earnings trends.

Looking at single stocks, data for the usual short-selling targets haven’t materially changed in recent weeks. Casino remains a top short, while H&M and Iliad are still among the most-shorted names.

| Name | Short Interest as % Free Float | Days to Cover Ratio | YTD Return |

| Casino | 38% | 27 | -13% |

| BIC | 25% | 45 | -21% |

| Ambu | 26% | 16 | -32% |

| Eurofins | 26% | 60 | 20% |

| Boskalis | 19% | 60 | -8.8% |

| Osram | 18% | 13 | -12% |

| AMS | 16% | 14 | 69% |

| H&M | 16% | 30 | 35% |

| Iliad | 16% | 23 | -19% |

| Source: IHS Markit; Data as of July 5 | |||

Some positions may have become painful, however. Zalando, one of the best performers of the Stoxx Europe 600, is up 84% since the start of the year. The short base remains elevated, at 13% of free float, but has fallen fast as the stock rose and JPMorgan analysts see strong revenue growth in the second quarter.

Osram is a different case: the lighting company is subject to a takeover bid from Bain and Carlyle, and was a laggard following a series of profit warnings. The shares have soared 34% since their bottom on June 7, while the short interest has jumped 2.1 percentage points between June 28 and July 5, right before the takeover bid was made.

Another takeover development to keep an eye on is German food distributor Metro. The short interest surged after the company received an approach from Czech billionaire Daniel Kretinsky on June 21, which was rejected by the board. The shares are trading near the offer price, which could leave the stock vulnerable unless the bid is raised. Metro had the biggest surge in short bets among Stoxx Europe 600 members over the past two weeks.

Still in the food retail sector, Ocado, which reported today, is another interesting case to watch. The short interest is about 7.3% of float after a surge from 2.4% at the end of May. The company kept its guidance but partnerships and future revenue will continue to be scrutinized, especially after the share price rocketed 50% this year.

In the meantime, Euro Stoxx 50 futures are trading down 0.3% ahead of the open.

- Watch European chemicals after BASF cut its 2019 sales and profit forecast, citing deepening economic slowdown, a weakened automotive market and the fallout from the China-U.S. trade spat. Citi says BASF guidance cut has “troubling implications” for the chemicals sector. Watch peers Covestro, Bayer, Clariant, Croda, Solvay, Lanxess and others.

- Watch Nordic banks after Danske Bank cut its profit forecast for this year, blaming “weak momentum” in revenue and heightened compliance costs. Watch peers including SEB, Nordea, Swedbank, Handelsbanken and DNB.

- Watch the pound and U.K. stocks after Bloomberg survey showed the U.K. economy probably shrank for the first time since 2012 in the second quarter. Separately, U.K. Conservatives working to prevent a chaotic Brexit have proposed legislation to stop the next prime minister suspending Parliament to force a no-deal break from the European Union.

COMMENT:

- “The key change in our outlook is that we now see trade and geopolitical frictions as the principal driver of the global economy and markets,” BlackRock Inc.’s Investment Institute says in its mid-year 2019 outlook, taking a “modestly” more defensive investing stance.

COMPANY NEWS AND M&A:

- BASF Joins Chemical Makers Cutting Targets as Demand Plunges

- Danske Bank Cuts Profit Forecast, Blaming Weaker ‘Momentum’

- UniCredit Raises $1.2 Billion Selling Remaining Fineco Stake

- WPP Is Said to Near Agreement to Sell 60% of Kantar Unit to Bain

- L’Oreal CEO Says Nestle Is Happy With Its Stake in FT Interview

- ABB Sells Solar Unit to Italy’s Fimer; Books $430 Million Charge

- Genmab Says Daratumumab in Combination Met Primary Endpoint

- Airbus, Boeing May Pull Out of Canada Fighter Jet Bid: Rtrs

- Airbus Asks Airlines to Check Wings of Older A380s for Cracks

- Salini Prepares $1.7 Billion Bet to Save Italy’s Building Sector

- Groupe Bruxelles Lambert in Exclusive Talks to Buy Webhelp Group

- Wumart, Yonghui Said to Be in Final Race for Metro’s China Unit

- Brazil Regulator Fines Alstom, Caf, Bombardier on Subway Cartel

- Orsted Among Power Companies in Danish Price-Setting Probe: JP

- Belgian Fintech UnifiedPost to Seek Listing on Euronext: L’Echo

- AB InBev Asian Unit IPO Draws HK$9.4B of Margin Loans: HKEJ

NOTES FROM THE SELL SIDE:

- Danske’s cutting of its FY profit wasn’t a surprise given the headwinds the bank faces, including expected weaker trading income, compliance costs, compensation to Flexinvest Fri customers, and falling rates, says Per Hansen, analyst at Nordnet Bank.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 397.9 (May 2018 high); 403.7 (2018 high)

- Support at 385.7 (76.4% Fibo); 381 (50-DMA)

- RSI: 62.7

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,596 (May 2018 high); 3,687 (2018 high)

- Support at 3,519 (76.4% Fibo); 3,412 (50-DMA)

- RSI: 66.8

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Babcock upgraded to neutral at Citi

- Galp upgraded to buy at Kepler Cheuvreux; Price Target 16 Euros

- Generali upgraded to neutral at Goldman; PT 16 Euros

- ICADE upgraded to neutral at JPMorgan; PT 89 Euros

- Ingenico Group upgraded to add at AlphaValue

- LafargeHolcim upgraded to buy at Kepler Cheuvreux; PT 53 Francs

- Orange Belgium upgraded to buy at SocGen; PT 22 Euros

DOWNGRADES:

- Adecco downgraded to sell at Goldman; PT 51 Francs

- Antofagasta downgraded to neutral at Macquarie; PT 9.45 Pounds

- BASF downgraded to neutral at JPMorgan; PT 59 Euros

- Central Asia Metals cut to neutral at Macquarie; PT 2.10 Pounds

- Chr. Hansen downgraded to sell at Berenberg; PT 575 Kroner

- Deutz downgraded to hold at Kepler Cheuvreux; PT 8.50 Euros

- Diageo downgraded to hold at Kepler Cheuvreux; PT 34 Pounds

- HeidelbergCement cut to hold at Kepler Cheuvreux; PT 73 Euros

- Intertek downgraded to sell at Goldman; Price Target 54 Pounds

- Just Eat downgraded to hold at Berenberg

- Orkla cut to hold at Kepler Cheuvreux; Price Target 80 Kroner

- Randstad downgraded to sell at Goldman; PT 45 Euros

INITIATIONS:

- ASML rated new buy at SocGen; PT 220 Euros

- Alpha Finl Markets rated new outperform at Macquarie

- BPER Banca rated new neutral at MainFirst; PT 4.15 Euros

- Banco BPM rated new neutral at MainFirst; PT 2.10 Euros

- UBI Banca rated new outperform at MainFirst; PT 3.10 Euros

MARKETS:

- MSCI Asia Pacific down 1.4%, Nikkei 225 up 0.1%

- S&P 500 down 0.5%, Dow down 0.4%, Nasdaq down 0.8%

- Euro down 0.01% at $1.1213

- Dollar Index little changed at 97.39

- Yen down 0.06% at 108.78

- Brent little changed at $64.1/bbl, WTI down 0.2% to $57.6/bbl

- LME 3m Copper down 0.3% at $5875.5/MT

- Gold spot down 0.2% at $1393.2/oz

- US 10Yr yield down 1bps at 2.03%

ECONOMIC DATA (All times CET):

- 9:30am: (UK) Bloomberg July United Kingdom Economic Survey

- 10am: (IT) May Retail Sales MoM, prior 0.0%

- 10am: (IT) May Retail Sales YoY, est. -0.6%, prior 4.2%

* For a daily wrap on developments in European equity capital markets, click here

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.