Owl Rock’s Lipschultz Says Direct Loan Funds Will Pass This Test

Owl Rock’s Lipschultz Says Direct Loan Funds Will Pass This Test

(Bloomberg Markets) -- Lending to midsize companies once seemed like the boring side of banking. Not anymore. A decade of ultralow interest rates and stricter bank regulation inspired a generation of financiers to create funds to provide companies with credit that banks no longer offer. In exchange, investors got juicier yields than almost anywhere else—as much as 5.3% more than on junk bonds or leveraged loans, according to a Goldman Sachs analysis in December.

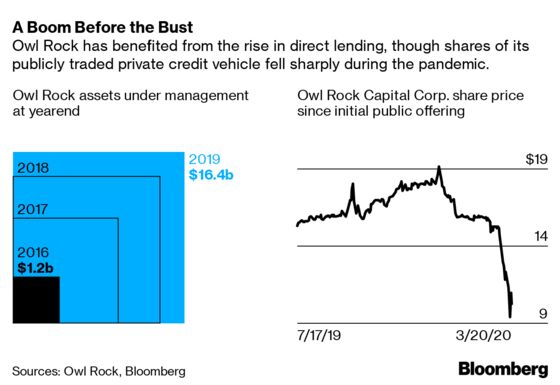

The poster child for this boom in direct lending is Owl Rock Capital Partners LP, a 4-year-old firm founded by three Wall Street veterans: Douglas Ostrover from Blackstone Group, 57; Marc Lipschultz from KKR, 51; and Craig Packer from Goldman Sachs Group, 53. By late 2019, when it sold a 20% stake to Neuberger Berman Group’s Dyal Capital Partners, the company was valued at $2.5 billion. By capitalizing on its founders’ Wall Street connections and zeroing in on one part of the $800 billion private credit market, Owl Rock built up about $16.5 billion in assets under management.

Now the coronavirus pandemic and its economic consequences are set to challenge this model in an unprecedented manner. In February—and again in early March—Bloomberg Markets sat down to talk with Lipschultz, the company’s president, about how this new business model evolved and what he expects to happen if there’s a global recession.

Kelsey Butler: Will the current market volatility impact your strategy or what kind of investments you make?

Marc Lipschultz: While none of us wish for this particular volatility, we really strove to build a business for such periods of time. We have permanent capital and a very long-term view on investing. We are, of course, extremely focused on our portfolio but are also very actively engaged in new loan origination to meet corporate capital needs when many other sources are no longer available—and we do so in a manner that doesn’t present systemic risk. At the end of the day, we remain focused on being a reliable source of capital to high-quality, stable businesses.

KB: How are you preparing for any impact on companies in your portfolio?

ML: We really are vigilant about our portfolio at all times. Because we’re often the lead financing source, we benefit from very close working relationships with our companies and their sponsors. We are all in this together with a common goal, which is to see these businesses thrive over the long term. Our team has very deep experience working with many businesses through many cycles, and [we] are fully equipped to manage our portfolio during this time.

KB: Let’s go back to the beginning. Can you take me through how the company came together?

ML: We started the business in 2016 with the observation that would found many businesses, which is that we saw a clear market need. On the one hand, there was a real need for an institutional-quality, large-scale direct lender to provide credit to middle-market companies that were seeing retreating availability of capital from traditional bank sources. At the same time, we were able to provide an institutional-quality access point to investors to be able to provide capital into that marketplace, seeking to earn a very attractive risk[-adjusted] return.

So we saw this opportunity where the need for private credit had grown, the availability of credit from traditional sources had retreated, and we wanted to build a best-of-breed provider to bridge that gap.

KB: How does the Owl Rock partnership work with you and your co-founders?

ML: We’re really a founder-led business. All three of us spend day and night, seven days a week focused on this business. That’s been the model from the beginning. We all share responsibilities, we all share accountability.

We’re all responsible for making sure, most important, that we’re exceptional stewards of the capital, that we’re doing vigorous underwriting, that we’re originating so we can see all the best opportunities, and that we’re managing our portfolio very carefully. We all really try to team up and make sure that at any given time we always have one or more of us available to address the task, the question, the opportunity of the moment.

By being a dedicated firm with three co-founders, we’re able to deliver that boutique experience. But at the same time we draw from what we have learned as the best practices from spectacular firms like KKR, Blackstone, and Goldman Sachs, which are the origins of our founders, plus our CFO and COO [Alan Kirshenbaum], who comes from TPG.

KB: Is there a story behind the name? Where did Owl Rock come from?

ML: When it comes to naming companies, it’s not easy—both in terms of [deciding on] the name you want to have and in terms of what’s, in fact, available. So we thought we’d have these very intelligent-sounding names with Greek words or Latin words, and of course all of those were long gone. And then we went through a variety of different phases and ultimately settled on something simple but aspirational that I think captures who we are and intend to be. We like the vigilance, wisdom, and watchfulness of the owl and the stability and durability of the rock.

It turns out that owls have two really interesting attributes beyond that. One is that a lot of people really like them. And it also turns out to be a word that has a lot of really great puns associated with it. So when we do our fantasy football league at the office or other team activities, everyone gets to name their own team and you can do things like “Going Owl the Way” or “I’m Owl In.”

KB: Last year was a big year. One of your private credit vehicles, a business development company called Owl Rock Capital Corp., went public in 2019. You also secured an investment from Dyal Capital that confirmed the firm’s status as a unicorn. What made it possible for you to be that big in a relatively short time?

ML: We saw an opportunity in the market, both for investors to earn attractive returns and for borrowers to have a superior solution, a private market solution for their borrowing needs. And that’s proven true. I hope and like to think that a meaningful part of it has been just the intensity of focus, dedication, and commitment to direct lending as a business. It’s all we do.

KB: Private credit can mean many different things. How do you define it?

ML: The conversations about it can be very confusing because it can run the gamut from distressed-for-control strategies [buying a company’s distressed debt to gain control of its equity in a restructuring or bankruptcy] all the way up through project finance and every flavor in between. Our model remains fully focused on direct lending—we are providers of senior secured loans to larger middle-market companies, high-quality companies. We’re really in it to make sure that we protect our capital and that we’re always managing the risk and earning an attractive return for our investors along the way. So we’re in a very defined slice, and we’re focused on the U.S.

The amount of capital raised for direct lending has paled in comparison to the amount of capital raised in private equity, and they’re our primary client base. So demand for our product is growing much faster than supply.

KB: Borrowers and sponsors often say direct loans can be tailored to the business of the borrower. What allows direct lenders to create more bespoke loans?

ML: We are deeply engaged over a long period of time in structuring the loan. So if we think about the alternative—syndicated loans—it’s a very different business. [For syndicated loans,] things happen in days, maybe hours, in terms of the time that an issue comes to market and someone has to make a decision. Our typical transaction takes months to assemble because we’re doing the same depth of work that our private equity partner is doing, augmented by our own independent diligence and expert calls and checks. It’s a very involved process. We can then create an answer that matches the very particular facts of that opportunity, and we have the time to do it.

KB: How has the alternative investment space evolved during your career?

ML: The world has evolved dramatically. From 1995, I was blessed and fortunate to join KKR, which in my view is one of the best investment firms that ever existed. I spent 21 years there, from a time when there were a handful of so-called LBO [leveraged buyout] firms that have since been rebranded as private equity firms. KKR, Blackstone, TPG, and Goldman have created an entire industry and institution out of these great practices of private capital to help support long-term development of companies.

Now there are thousands of private equity firms but very, very few like KKR. There are thousands of firms in the middle market. And what you saw, particularly since the [2008] crisis, was that those firms are thriving and doing wonderful work and buying great companies, but they too need credit. And there has been a decrease in the availability of borrowing from banks. Banks aren’t lending directly to these companies. And that’s been an evolving part of the landscape for coming up on 25 years in terms of my personal experience: a secular move from banks being lenders to middle-market businesses to really being intermediaries and syndicating [loans], or being lenders to very large companies.

That’s left this space, in terms of the middle market that still absolutely needs credit to thrive and grow, available for an alternative set of providers. And we’re one of those. But also we don’t have deposits. We don’t present any sort of systemic risk. We’re very low leverage. Our vehicle, Owl Rock I, is less than one turn of leverage [the ratio of debt to equity]. Banks before the crisis had 30 turns of leverage, and the government [served as an] effective backstop. We’re on our own. We have institutional capital, everyone understands what’s being committed, it’s low leverage, it’s long term. Our capital is locked up. There’s no run-on-the-bank risks.

So we really have taken the risk out of the system that became a contagion in 2008, 2009. We aren’t linked to these other parts of the system. It’s not the government’s risk. And it’s not the people of this country’s risk.

KB: You spent most of your career at KKR and had a breadth of experiences there. What were some highlights?

ML: When I came on board at KKR, there were really two PE firms of scale in the country: KKR and Forstmann Little. KKR obviously has become an absolute global powerhouse in investing. It’s been incredible to have been a part of that evolution. From 1995 until I started Owl Rock, I was involved in private equity. I was lucky enough to be involved in the development of KKR’s infrastructure business and had a chance to see the evolution from LBOs in the U.S. to all types of alternatives across all geographies.

I benefited greatly from the wisdom of Henry Kravis and George Roberts, who are incredible mentors to me and dear friends. I’ve been through a lot of cycles. I’ve been through a lot of wins, and I’ve been through some losses, and it definitely gives a perspective that I think ultimately benefits the development of Owl Rock and the way we’ve approached the business.

KB: A lot has been written about how risky private credit and direct lending is. What’s your response?

ML: I largely believe that’s a very misunderstood topic. Now to be crystal clear, we’re in a risk-managed business. This is not Treasuries, and this is not owning gold. So of course there’s an element of risk to this business, but what we do, the depth of work and the vigor of that work and the intensity of focus on managing our portfolio and the fact that our capital is locked up. We focus particularly on BDCs [business development companies], that’s permanent capital. So we have capital in perpetuity. So in a way we have the perfect pool to match any borrower’s needs, and we don’t have the sort of risks that go with funds that may come and go with institutions that may or may not have an interest in this sector.

As for the risk of a given borrower, that all gets down to having 140 people who wake up every day and think about what makes for a good borrower and what are we looking for? And we have a lot of pattern recognition and a lot of experience. [That includes] Doug Ostrover, Craig Packer, and I and the rest of our very experienced team who’ve spent decades in this business. We’ve been through the crises, ’08, ’09 for sure, which was painful and recent. But we also were around for ’01, and we also were around for the late ’90s and the Asian flu. So we’ve seen these challenges, and we focus every single day on being ready. The key in our business is to manage that risk.

So there certainly is an element of risk to any investment business. But the strength of the credit agreements that we write are far, far, far more protective of the lender than what exists in the syndicated market. We do spend months working on the agreements and tailoring them. It also means we get to write a credit agreement that protects us for the particular elements of that business that we need to be mindful of.

KB: Are there any terms in credit agreements that are alarming to you?

ML: When I look at the documentation and credit agreements that we sign up to, the answer is a flat no, I don’t see any deterioration in what we’re prepared to do. We know where the line is for us. We won’t sign up to credit agreements that have the ability to strip out important assets or do damage to the layering of us as a lender. That said, I think the syndicated market [until recently was] tolerating a lot of terms that I would consider reasonably risky. The visible market is the syndicated market. When people talk about leveraged lending, they really aren’t talking about direct lending. They don’t know the details of these credit agreements. They don’t understand the depth of the work. So all they can really observe is the liquid syndicated market. Many of the challenges you’re describing and the attendant risks are exhibited in the syndicated market.

I genuinely don’t see it in the private credit market. I don’t think our documents look meaningfully different today than they did four years ago. And certainly the rigor of our work hasn’t changed.

KB: What does it take for a direct lender to stand out in a competitive environment?

ML: Having watched the broad alternatives industry evolve over almost 25 years, I don’t view the number of participants in the upper middle market in direct lending as very competitive at all. Public stocks, public bonds, syndicated loans, real estate, or private equity are much more mature asset classes, and the number of participants are literally orders of magnitude beyond what we experience. I think we may be distinctive in so much as we’ve become a large-scale participant. There’s been a proliferation of $1 billion funds, but those aren’t our competitors because we provide financing for borrowers that want 100, 200, 300, $500 million, and that’s a much, much smaller number of parties that can provide that reliably.

Our experience and firm belief is that larger borrowers are generally safer credits. They have more levers to work with when there are challenges, and they have more strategic value in the event that there’s a challenge and there needs to be an exit. A company with $50 million or $100 million of Ebitda has many more critical strategic suitors than a company that has $5 million or $10 million that may just go away.

We picked a part of the market that’s safer inherently in the nature of the businesses, and we work with wonderful sponsors that are really talented and have lots of capital to stand behind those companies. Typically we’re 50% of the capital structure. So the first 50% lies in the hands of the equity holders. So there’s a lot [standing] between us and risk to our dollars.

Having 140 people here doing direct lending is a huge advantage, because it means that we can provide active partnership and coverage to a huge array of potential borrowers. In a typical week, we’ll see 30 to 40 opportunities. Since inception we’ve looked over 4,000 different loans. We couldn’t do that if we weren’t so heavily invested in people.

KB: Is the investor base for direct lending changing?

ML: The investor base has moved much more institutional and high net worth. If you go back 10 years, you’d see it as much more of a retail product. Now, if done right, it’s wonderful for retail. And in fact, we have our product in the mass-affluent channel. It’s a fantastic match in a world where people are trying to earn appropriate return and recurring income in a protected way. But the change has really been the institutionalization. We’re lucky enough to count as our investors many of the biggest-name, institutional-scale family offices and public pension funds and foundations and endowments.

So part of what we tapped into in building Owl Rock was the timing and the need for institutions to come and provide capital to this expanding marketplace. That’s been a very significant change. There’s an increasing number of institutions that participate in direct lending, who recognize it’s an asset class unto itself and have separate allocations for direct lending. That’s largely happened over the last five years.

KB: In your large public business development company, fees will be going up later this year. How will that affect your dynamic with investors?

ML: Our fees aren’t going up. The fees are visible, always have been, are now, and the difference is that we’ve been waiving and giving back a portion of what we’re entitled to, to the incremental benefit of our investors. So we think we’ve developed a wonderful base risk-return proposition for all our investors at the stated and typical fee level. We’ve added on top of that this period of time where we’ve said, “We’ll reach into our pocket, and we’ll give you back part of those economics to make the investment that much more appealing.” But all of that was transparent. So I view it as a nonevent.

KB: What do you expect to happen in this downturn?

ML: That certainly will draw a distinction between lenders who’ve taken on outsize risk relative to the reward. I feel very confident saying we’re one of the people that has stayed very, very disciplined about what risks we take. So that’s why we focus so heavily on first-lien [loans] solely to larger companies in durable, stable industries. In a downturn, not only do we want to make sure we’ve protected the investments that we’ve made, but we also want to be a provider of capital to the many companies who will need it.

Syndicated loans shocked the world in terms of how well they performed through the darkest of downturns in ’08-’09, so actually we have a lot of data on that. That’s been 2% average annual default rates, 70¢ recoveries for senior loans over the long sweep of history. So there’s a lot of data on how senior credit performs. When we get to private direct lending, we’re talking about a lot of the same companies, but much more intensive diligence and much more rigorously negotiated credit agreements.

There’s plenty of data that says senior credit is very durable through even deep dark cycles, and I would say we’re going to experience private credit outperforming liquid credit in a downturn.

Butler reports on private credit and direct lending for Bloomberg News in New York.

©2020 Bloomberg L.P.