Options Show Complacency Reigns Supreme in Battered U.S. Stocks

Options Show Complacency Reigns Supreme in Battered U.S. Stocks

(Bloomberg) -- It’s just a correction -- not the start of something deeper.

Looking at trading in U.S. equity derivatives, there are few signs of fear even on the heels of a double-digit drawdown in the S&P 500 Index and Nasdaq 100 Index.

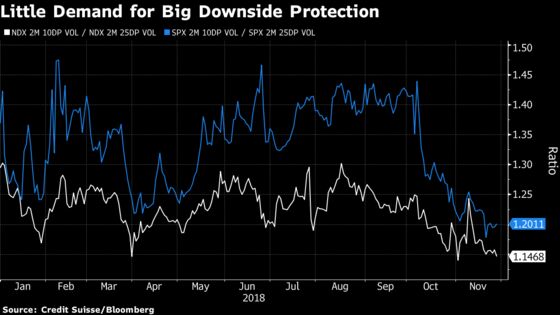

Options that provide protection against a further 10 percent decline in the benchmark U.S. equity gauge and its tech-heavy counterpart aren’t in high demand. The ratio between the implied volatility -- a proxy for cost -- of 10-delta versus 25-delta two-month puts has plummeted to near 2018 lows for both the Nasdaq 100 and S&P 500 Index.

JPMorgan Chase & Co. agrees. The S&P 500 put/call open interest ratio, which measures the amount of bullish versus bearish options outstanding, has plunged -- but that drop signals caution instead of underhedging because it’s accompanied by sharp deleveraging and is explained mostly by increased demand for calls, strategists Bram Kaplan and Marko Kolanovic wrote in a note Monday.

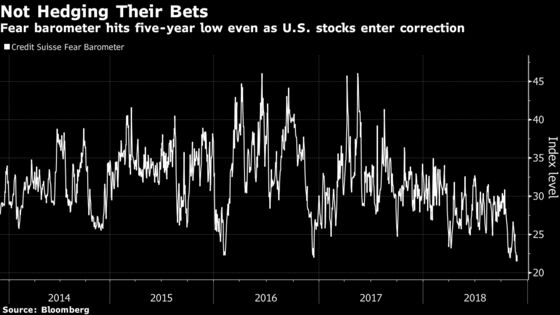

“Along with a lack of demand for VIX hedges, we’ve also seen muted demand for protection in the equity index space,” wrote Mandy Xu, chief equity derivatives strategist at Credit Suisse. The Credit Suisse Fear Barometer, which tracks the cost of downside three-month protection relative to upside options, “fell to a new five-year low last week as investors took advantage of the sell-off to monetize hedges and add to upside bets.”

The meager demand for puts speaks to how much this equity sell-off involved, well, a lot of selling.

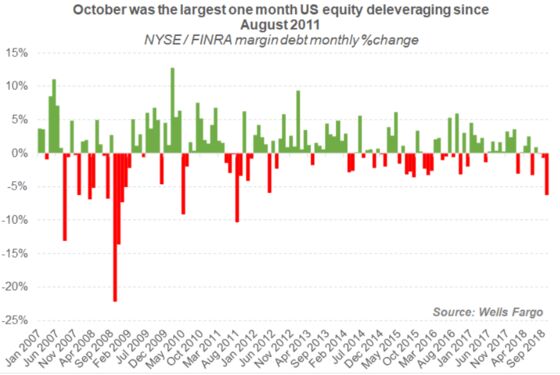

October saw the biggest monthly deleveraging as well as the worst hedge fund performance since August 2011, said Wells Fargo & Co. equity derivatives strategist Pravit Chintawongvanich. That crunch in margin debt points to large investors liquidating en masse, cutting exposure as their favorite stocks got pummeled.

“On the one hand, deleveraging rarely happens in a vacuum, and usually leaves high volatility in its wake. But we do not think this risk-off episode becomes systemic,” he wrote. “There might be a bit more ‘purging’ to come as witnessed by the violent sell-off in tech stocks last week, but we’re incrementally closer to the equity de-risking being complete.”

Weeden & Co. Chief Global Strategist Michael Purves thinks the current read from the markets makes sense.

“Even with the recent technical violation of the the S&P 500’s key support level and choppy trading, a December rally could easily post a solid return while historical data suggests downside risk is relatively modest,” he said. “Hedging is in order, but so is hedging discipline.”

But where some see a light at the end of the tunnel for U.S. equities, others see an oncoming train.

“With equity-implied volatility futures curves still being flatter, and low relative to history, this suggests there is still a fairly high degree of complacency among investors,” write HSBC multi-asset strategists led by Max Kettner.

Realized volatility that’s creeping higher across the spectrum implied “that there is still more downside for risk assets in the coming months,” he said.

--With assistance from Sid Verma.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Joanna Ossinger, Eric J. Weiner

©2018 Bloomberg L.P.