Only a Trickle of Wall Street Workers Return for NYC's Reopening

Only a Trickle of Wall Street Workers Return for NYC's Reopening

(Bloomberg) -- Editor’s Note: No city is more important to America’s economy than New York, and none has been hit harder by the coronavirus. “NYC Reopens” examines life in the capital of capitalism as the city takes its first halting steps toward a new normal.

At Citigroup Inc.’s headquarters, Monday morning rush hour meant only a few dozen bankers entering the Lower Manhattan tower.

A few blocks away, a worker at Greenwich Cleaners said customers were bringing in clothes that weren’t even dirty, just to support the business. Inna Lipovsky, a florist on Wall Street, said her City Blossoms had received just two orders by mid-morning.

“It’s better than nothing, but we’re hoping it’s going to get better,” Lipovsky said.

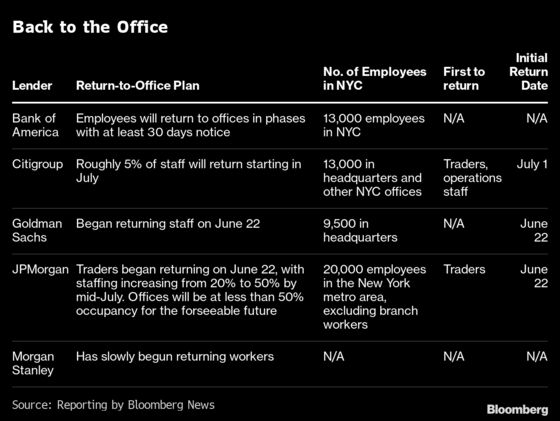

New York may have entered the second phase of its gradual reopening this week, but in major office districts, many of the biggest employers aren’t rushing to bring people back. Citigroup, with more than 13,000 workers in New York, won’t start ramping up its return until next month and even then will just have 5% of staff in its offices.

At Royal Bank of Canada’s capital markets business in New York, the firm still has just 17 people — or less than 1% of total staff — in the office. Blackstone Group Inc. doesn’t plan to open offices even to a small subset of its 2,200 employees until next month and Carlyle Group Inc. has told staff in New York to wait until at least September.

Visa Inc. still hasn't opened its offices in New York. Marsh & McLennan Cos. doesn't plan to open its New York location until July 13, and even then only about 10% of employees will return as part of the company's pilot program to reopen offices.

Office occupancy across Rudin Management Co.’s 14 buildings in New York peaked at 5.4% Monday. That's double or triple the occupancy of a couple of weeks ago, said Nicholas Martin, a company spokesman. Many major tenants are planning to return in early July, he said.

Since the lockdown began in March, financial firms have eschewed their option as essential businesses to bring more staff into their offices. Hopes that the city’s phased reopening would inspire a quick rebound of the bustling economy are running into the realities that big companies are going to be cautious. In a recent workplace survey of 60 companies conducted by the Partnership for New York City, employers said they only anticipate having 10% of employees back by Aug. 15. By year-end, they expect just 30%.

Many firms have been pleasantly surprised at employees’ ability to work remotely and some want to avoid putting a strain on public transit with workers who don’t have to be in the office. Companies are also taking time to retrofit spaces for social distancing, or upgrade air-conditioning systems and bathroom hand dryers. Employers including BlackRock Inc. plan to require mandatory training for staff returning to offices.

We’re tracking everything you need to know as New York reopens after the Covid-19 shutdown. Read our explainer and sign up for alerts sent directly to your inbox.

Still, a few lenders are using the city’s second phase as a chance to roll out plans. JPMorgan Chase & Co. and Goldman Sachs Group Inc. picked this week to start bringing a small group of employees back to the office. But even for JPMorgan's 20,000 corporate employees in the New York metropolitan area, the firm doesn't plan to bring back more than 20% until after Labor Day.

Commercial real estate firms like Silverstein Properties are trying to lead the way. The owner of several World Trade Center towers has 406 employees in the city and expects 25% in the office this week. The firm’s 89-year-old Chairman Larry Silverstein already went back to the office last week.

“The desire to come back is clear,” said Jeremy Moss, head of leasing at Silverstein. “At this point, I think we’re going to see a steady flow of people come back to the office over the next month or two.”

Workers were sent home in droves starting in March to slow the spread of the coronavirus pandemic, which has sickened 8.8 million people and killed 465,000 globally.

The delay in returning workers to offices may augur a more permanent reckoning for New York office space. In a survey, the Partnership for New York City and Newmark Knight Frank found that roughly 37% of finance companies said they plan to decrease the space they occupy in the city by 20% or more. About one-fifth of professional services firms said the same. And more than a quarter of financial services companies plan to relocate jobs to the suburbs or other locations, the highest share of any industry.

At Brookfield Place — a 14-acre, 5-building complex in downtown Manhattan — many retailers and restaurants remained closed on Monday. The vast majority of stores inside the World Trade Center’s Oculus remained shuttered, and the only real noise was the screech of train cars pulling in and exiting.

Still, there were signs of life downtown. Flyers plastered across buildings advertised plywood removal services to help business owners to reopen.

And at Sola Pasta Bar on the corner of Broadway and Grand Street in SoHo, diners took refuge from the midday sun under umbrellas at sidewalk tables. Upbeat music pulsed out onto the street and the restaurant was operating a bright orange sidewalk stand where parched shoppers could pick up Aperol spritzes or other cocktails.

“It’s crazy,” said Simone Tiligna, who co-owns the restaurant with Nicola Pedrazzoli. “After four months, to start again is fantastic.”

©2020 Bloomberg L.P.