One Call Defined Investing in 2019. Now ‘Bubble’ Trouble Mounts

One Call Defined Investing in 2019. Now ‘Bubble’ Trouble Mounts

(Bloomberg) -- When Tim Rudderow settles into his office in a small town outside Philadelphia, the hedge-fund manager has a shortcut these days to figure out what’s been happening in the stock market.

He just sizes up the bond market.

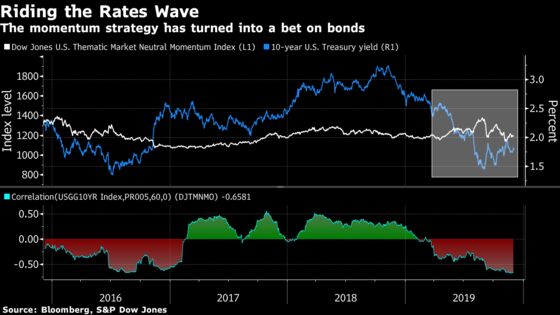

“I can come in the morning and look at the bond market and know whether or not momentum is outperforming value,” the chief investment officer for Mount Lucas Management LP with $1.5 billion overall said on the eve of Thanksgiving.

This rule of thumb was on the money hours later as higher yields powered a market-neutral strategy that favors cheap equities over high-flying peers by half a percentage point.

Bond-driven rotations like this have gripped quant and discretionary investors all year. Under the calm surface of the unstoppable global equity rally, interest rates have crowned stock winners and losers with exceptional force for this bull market. And it’s spurring more angst than usual on Wall Street that gyrations in government debt could upend a slew of investing styles in 2020.

The same recession fears that have fueled demand for Treasuries have rocked riskier equity strategies like value and pumped up havens including shares offering muted price swings. At the same time falling interest rates have boosted companies offering steady payouts like real estate and utilities to records.

Funds riding the bond rally in the U.S. and euro area like trend followers and risk parity are on course for some of their best returns this decade -- but could get punished in a protracted Treasury sell-off.

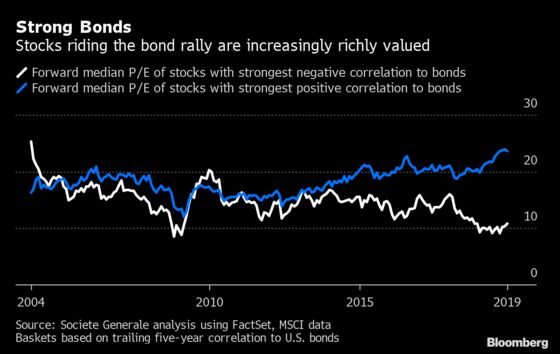

All told the world’s largest stocks that win from low yields are near their most expensive relative to the losers in at least 15 years, according to Societe Generale SA citing their five-year link with Treasuries.

The bank’s quant guru Andrew Lapthorne is worried. He warns the outperformance of shares that move along with bonds looks extreme -- making now a good time to take profits on interest-rate positions and bond-proxy stocks.

“The equity investor is buying bond risk, not cash flows,” the SocGen strategist wrote in a note.

Rudderow, who invests in macro, trend following and value strategies, is staying a safe distance from companies coveted for their consistent payouts when rates are low because of their soaring premiums. “It’s created this huge bubble -- it’s the only way to describe it,” he said.

Treasury gains and gyrations in yield curves -- fueled by bets on Federal Reserve easing -- have spurred violent stock rotations this year. And back again during bond sell-offs. In September there was a once-in-a-decade equity shift in favor of value over momentum -- a trial run of what could ensue should rates rebound sharply on better economic growth.

And the case for 2020 reflation is gaining momentum. Manufacturing surveys are showing some green shoots, American job growth just trounced expectations, and a phase-one U.S.-China trade deal could be in the offing.

Investors who dissect stocks by their traits known as factors typically don’t time their strategies to ride cyclical shifts in economic data or interest rates. Alessio de Longis at Invesco Ltd. does.

His quant models flashed a shift in the economic cycle after bond yields appeared to have found a bottom in the fall. It’s prompted a more risk-on allocation, favoring value and small caps at the expense of low-volatility shares as well as momentum strategies which have had a defensive bias. The Invesco Russell 1000 Dynamic Multifactor ETF has outperformed the benchmark by 5 percentage points this year.

That higher bond yields have spurred a more risk-on rotation of late is no “coincidence,” de Longis said in an interview.

Overall the interest-rate cycle is proving something of a foe for most other active systematic managers, especially the market-neutral crowd. They’re on course for another year to forget. Figuring out why is far from easy, but Joseph Mezrich at Nomura Instinet LLC proffers one theory from the quant data he’s been tracking all year.

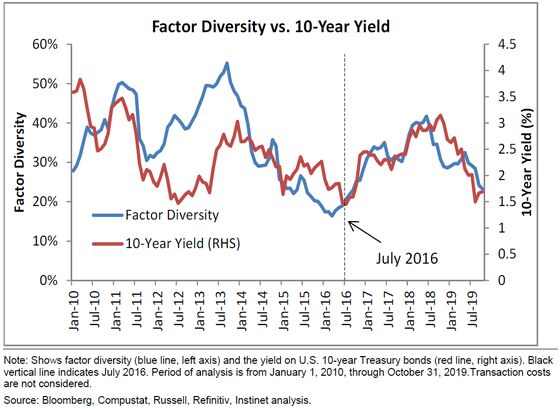

As yields plunged, factor styles have been increasingly influencing each other, making it harder for investors to diversify their risk, according to the strategist. “The fortunes of factor investors, who rely on the diversification benefits of factors, are affected by changes in the level of the 10-year yield,” he wrote in a note.

That correlation challenge is one reason why Sanford C. Bernstein reckons quant and fundamental funds will probably see returns near the bottom of their decade range over the coming year. Their estimates are based on a model that considers how much stocks and factors are moving together and the dispersion in returns.

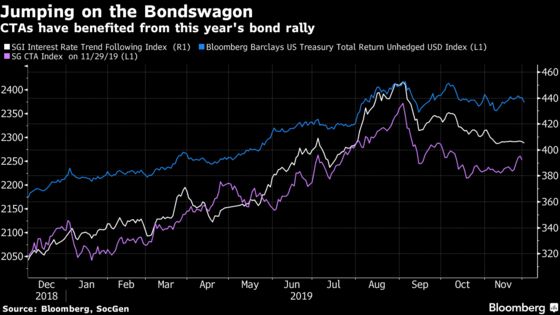

The good news is that bond mania is proving a boon for strategies that jumped on the bandwagon.

Commodity trading advisers, a breed of quant that uses futures contracts and typically surfs the market momentum, are on course for their best year since 2014, according to a SocGen index. Risk-parity funds, which allocate based on volatility levels and hold large fixed-income positions, are heading toward their biggest annual gain since 2005, an S&P index shows.

Among the beneficiaries, there’s a sense that the easy gains are over.

Roberto Croce, a fund manager at BNY Mellon Investment Management, says risk-parity portfolios have pared bond longs given higher volatility in fixed income. The CTA index has dropped 6% since reaching a 19-month high in early September when the bond rally eased up.

As for Rudderow at Mount Lucas, his conviction is growing that value stocks are turning the corner as yields rise -- potentially signaling good news for the economic expansion and bad news for bond-proxy shares.

“You get a few times in your trading career where things are this out of whack,” he said. “If there’s anything positive on the economic growth front, that whole trade isn’t going to end well.”

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Sid Verma

©2019 Bloomberg L.P.