Once Too Risky, U.K. Stocks Now ‘Too Cheap to Ignore’

Once Too Risky, U.K. Stocks Now ‘Too Cheap to Ignore’

(Bloomberg) --

So this is it, Brexit is happening. While most trade negotiations are yet to come, the symbolic date marks a decisive turn in the saga that has been a massive drag for U.K. stocks since mid-2016. With the country already setting up a clash with the U.S. over Huawei Technologies Co., and a key Bank of England rate decision Thursday, here’s a look at where U.K. stocks stand in this crucial week.

U.K. shares are “too cheap to ignore,” say Morgan Stanley strategists. “While Europe in aggregate may not look fundamentally cheap, the U.K. does”. According to them, the U.K. remains one of the most undervalued major stock market in the world and a normalization to the 10-year average would mean a 13% re-rating. In term of P/E, the MSCI U.K. is trading at 20% discount to the MSCI World.

Sector-wise, Morgan Stanley strategists say media, household products, food retail and banks look the cheapest compared with European and global peers. U.K.-listed companies make up about a third of the bank’s 25 overweight-rated European stocks trading in the bottom-half of their 10-year P/E range relative to global competitors: Weir Group Plc, Royal Bank of Scotland Group Plc, Unilever, Reckitt Benckiser Group Plc, BP Plc, Associated British Foods Plc, Johnson Matthey Plc and Prudential Plc.

Cheapness aside, there are still risks ahead, particularly around trade talks. European negotiators are already suggesting more time will be needed, while the U.K.’s green light for Huawei to help develop parts of its 5G wireless networks risks a rift with U.S. President Donald Trump.

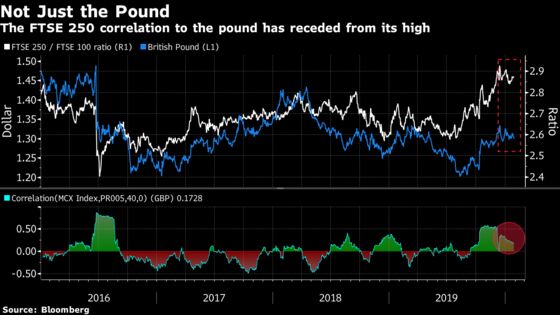

UBS strategists see Brexit as a “work in progress,” and stay skeptical about a potential macro pick up. They say U.K. equities, particularly domestic and cyclical stocks, have already rallied in anticipation of a turn in the economy, which puts them at risk should that fail to materialize. The domestic-heavy FTSE 250 Index has outperformed the more international FTSE 100 Index in the past year.

Not everyone agrees. Goldman Sachs Group Inc. and JPMorgan Chase & Co. strategists are more positive on domestic stocks, with JPMorgan favoring homebuilders, domestic banks, real estate and retail.

Goldman strategist Sharon Bell says the U.K. economy has returned to growth with the flash PMI climbing to 52.4 in January, well above consensus expectations, while the renewed optimism of manufacturers also bodes well for domestic stocks. Goldman sees U.K. GDP accelerating from the second half of the year onwards.

Expectations of a better outlook have boosted the FTSE 250 Index even as the pound has fallen amid speculation of an interest-rate cut. As seen in the chart below, the correlation between the mid-cap index and sterling has sharply receded.

Overall, the reduced political uncertainty and Brexit risk following a decisive Tory victory last month has revived investor’s interest in U.K. equities. That has made the market “investable once more,” HSBC strategists say, seeing the rally as likely to continue given the current discount to long-term average. They see the pound reaching $1.45 by the end of the year as growth picks up. A higher pound could still prove a drag for the FTSE 100.

Still, the benchmark’s P/E is below that of the broader Stoxx 600, signaling more room for a re-rating, while the FTSE 250’s relative valuation is also some way away from its 2013 peak.

While the consensus expectation is for no change at tomorrow’s Bank of England decision, Deutsche Bank economists expect policy makers to be dovish and cut rates by 25bps, which could keep the pound in check.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Namitha Jagadeesh

©2020 Bloomberg L.P.