Once Hated, Now Loved: BBB Corporate Debt Is Back in Vogue

Once Hated, Now Loved: BBB Corporate Debt Is Back in Vogue

(Bloomberg) -- There was a period of time late last year when BBB rated bonds -- those securities just above junk status -- were anathema in the corporate debt market.

Investors, fearful that these bonds were about to get hit by a wave of credit-rating downgrades, dumped them day after day in November and December. But now, in a sudden and surprising turnaround, these securities have become one of the most popular slices of the corporate debt market, having handed investors gains of 5.8 percent this year.

And some of Wall Street’s bigger investors, including Loomis Sayles and T. Rowe Price, say there are still plenty of bargains to be had among the BBBs, as the Federal Reserves signals it is dovish and working to ensure the U.S. economy keeps humming.

“If the economy is still decent enough to support profits, you don’t have to worry about investment-grade downgrades,” said Matt Eagan, a portfolio manager at Loomis Sayles & Co. that has been buying BBB debt. “The Fed will do whatever it takes to support growth. To me, that’s giving the green light.”

There are reasons to be optimistic about the credit. Some of the world’s biggest corporate bond issuers, including AT&T Inc. and General Electric Co., are rated in the BBB tier and are focusing on paying down debt. And with yields having fallen so much this year as the Federal Reserve keeps rate hikes on hold, companies can continue to borrow at a reasonable cost.

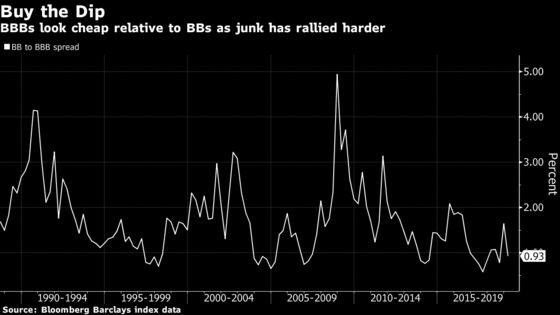

For investors, BBB debt looks cheap by historical standards compared with the safest junk bonds, or those in the BB tier. And while the risks of slowing economic growth now appear higher, few are bracing for a serious recession that would clobber profits.

The debt in the lowest part of the high-grade spectrum has also lagged higher-rated securities since October’s selloff. In the A tier, risk premiums, or spreads, were just 0.06 percentage point wider on Thursday than they were on October 1, soon before the market started weakening. BBB tier notes are 0.21 percentage point wider.

Read More: Growing Love for BBBs; Cutting out Wall Street

In the fourth quarter, investors and strategists began to worry more about BBB credits, which make up about half of the $5.3 trillion market for U.S. investment-grade corporate bonds, and the securities began to suffer. Companies like Anheuser-Busch InBev NV and Verizon Communications Inc. have taken advantage of a decade of near-zero interest rates to help finance acquisitions, often sacrificing credit ratings in the process.

The riskiest part of the market has grown fastest. BBB tier credits make up around half the market, compared with around a quarter in 1993. At the end of 2018, these figures increasingly alarmed investors and strategists and the securities began to suffer. When BBB tier companies get cut, they can end up as junk credits known as fallen angels.

Now strategists at BNP Paribas SA and UBS Group AG are less worried about fallen angels. Companies are cutting their borrowing levels, and net issuance of investment-grade debt has dropped this year, making BBBs a good trade, BNP said in a March 22 report. Also, most fallen angels occur during recessions, which UBS strategists led by Stephen Caprio and Matthew Mish said is a “muted” risk. This year, BBB notes are performing better than the broader investment-grade credit universe, which has gained 5.2 percent through Thursday.

BBB credits also look cheap relative to BBs, with the gap between yields for the two tiers at just 0.93 percentage point as of Thursday, well below its five-year average of around 1.16 percentage point, according to data compiled by Bloomberg. The gap has narrowed as BB bonds have been the main beneficiary from the rally in junk, while BBB bonds have lagged the broader investment-grade recovery.

With the Fed on hold now, it may make sense for some junk bond managers to look at buying BBB notes. The securities on average are longer dated than high-yield debt, and can generate high returns with less credit risk, said John McClain, a portfolio manager at Diamond Hill Capital Management.

“It feels like there’s no catalyst for rates to go higher from here. At this point, duration is your friend,” McClain said. “It’s been all about taking credit risk, but shifting now to taking interest rate risk.”

Investor Confidence

Not everyone is sold on buying longer-dated bonds. For companies, the cost to borrow beyond five years is still relatively high as credit curves have steepened. That may indicate “investors’ latent fears of adding spread duration to portfolios until there is greater confidence in the backdrop for the economy, corporate fundamentals and global flows,” Citigroup Inc. credit strategists Daniel Sorid and Wei Guan said in a March 25 report.

Some investors are taking the Fed’s actions as an opportunity to cash in on profits and de-risk their portfolios. Lon Erickson, portfolio manager at Thornburg Investment Management, said he is reducing credit risk and becoming a little more defensive after having taken a risk-on position for much of the first quarter.

But for some money managers, that fear represents an opportunity.

“I have more BBBs now than I did last year,” said Steven Boothe, lead portfolio manager of the global investment-grade corporate bond strategy at T. Rowe Price, which manages $1 trillion. “There are dislocations across the BBB space that are worth exploring.”

--With assistance from James Crombie.

To contact the reporters on this story: Molly Smith in New York at msmith604@bloomberg.net;Natalya Doris in New York at ndoris2@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Sally Bakewell

©2019 Bloomberg L.P.