Once Again, It’s During a Stock Rout That Active Managers Shine

Once Again, It’s During a Stock Rout That Active Managers Shine

(Bloomberg) -- After a decade-long uphill battle against passive investing, active funds are getting a rare moment of respite, courtesy of the worst equity sell-off since 2018.

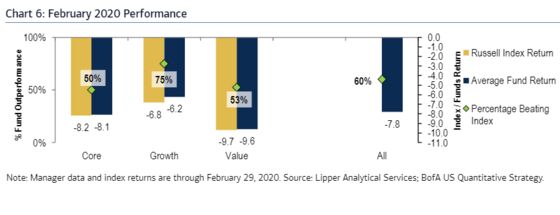

About 60% of large-cap mutual funds beat their benchmarks as the S&P 500 tumbled into a correction in February, the best hit rate in two years, according to data compiled by Bank of America Corp. The outperformance was achieved when the average fund only fell 7.8% over the stretch in question.

This is what life has become for active managers, trying to sell something whose main claim to value is that it fails at a slightly less horrifying rate when shares tumble. That’s how it sometimes seems, going by the last few stock routs: long-only mutual funds are mainly good at beating benchmarks in down markets, while trailing when things are going up.

“It’s frustrating,” said Jeff Sica, chief investment officer of Circle Squared Alternative Investments in Morristown, New Jersey. “The angst of most active managers is that their only time to shine seems to be where the market is collapsing.”

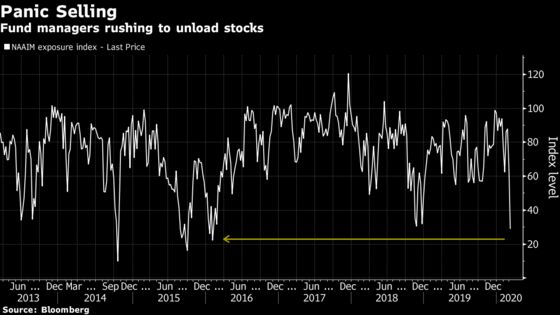

Sica said fund managers have been able to weather the market storm partly because they quickly cut risk. Theoretically, raising cash or trimming big losers would allow a portfolio to avoid deeper losses. During the latest sell-off, money mangers have been selling stocks at the fastest pace since 2014, according to a survey by the National Association of Active Investment Managers.

NAAIM’s exposure index, tracking investment advisers from 200 firms overseeing more than $30 billion, has fallen to 29% from 88% just two weeks go, reaching the lowest level in four years.

To be sure, money mangers who got steamrolled by the proliferation of passive investing are within their rights to feel vindicated, at least for now. Years of steady gains have handed anyone who bought an exchange-traded fund tracking the S&P 500 an annualized gain of almost 17% since 2009.

That kind of return has proved hard to surpass. Over the last 10 years, less than a quarter of all active funds managed to beat their passive rivals, data compiled by Morningstar Inc. showed.

The subpar performance, along with relatively higher fees, has led to massive withdrawals. During the past decade, U.S. equity active funds have lost approximately $1.4 trillion, while their passive counterparts like index mutual funds and ETFs took in about $1.6 trillion, according to data from the Investment Company Institute and Bloomberg Intelligence.

For those hoping that better returns would ease the exodus from active funds, the performance is at least encouraging. Their favorite bets are working, with a Goldman Sachs Group Inc. basket of mutual funds’ most-loved shares beating the S&P 500 by almost 1 percentage point last month.

The top 10 and bottom 10 stock picks contributed to above-market returns totaling 54 basis points for core mutual funds, according to data compiled by BofA strategists including Jill Carey Hall and Savita Subramanian.

Money managers tend to pick stocks on strong fundamentals, and that quality bent may have helped them stand out as winners during times of trouble. Last May, when Wall Street was roiled by U.S.-China trade tensions, active funds made a comeback after holding fewer stocks with China exposure than what’s suggested by benchmarks. Amid the sell-off in early 2018, they experienced muted losses, buttressed by better returns from their favorite bets.

During the latest rout, growth funds fared the best, with 75% of them beating benchmarks, BofA’s data showed. Down 6.2% on average, the return is hardly something to celebrate. Still, anyone who painfully watched stocks wiping out half their values during each of the two last bear markets may welcome any losses that are smaller.

“All of us who believe in active management over the long run have said that some sort of a large sell-off would eventually put a spotlight back on,” said Bill Stone, chief investment officer at Avalon Investment & Advisory. “At least it will give people some taste of the benefit from being different than the index.”

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Chris Nagi

©2020 Bloomberg L.P.