Buy the Dip, Wait and See, Add Hedges: Investors on Iran Strike

Investors have taken a variety of approaches, from making short-term bets to taking out hedges to moving to the sidelines.

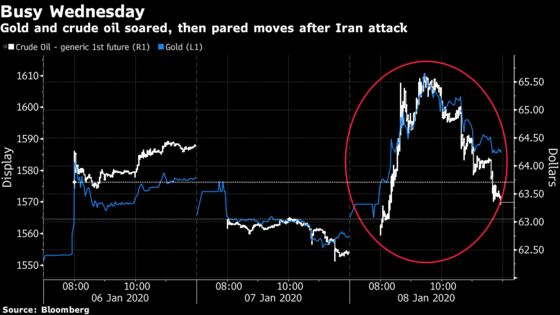

(Bloomberg) -- Financial markets were roiled anew on Wednesday after Iran retaliated against the U.S. for killing one of its top military commanders, spurring investors to reassess geopolitical risks for their portfolios.

Key to the longer-term outlook is whether strikes by one side on the other continue, and shifting indications have spurred volatile moves in stocks, currencies, oil, gold and bonds since Friday. Market participants have taken a variety of approaches, from making short-term bets to taking out hedges to moving to the sidelines.

Risk assets tumbled and havens soared in the immediate reaction to the U.S. killing of Iranian General Qassem Soleimani, but the moves faded by Monday. A similar pattern occurred Wednesday, with a risk-off wave following Iran’s strike on two U.S. targets in Iraq that then eased as Tehran stressed that it wasn’t seeking war.

European stocks slid 0.4% in early trading, less than their Asian counterparts, while U.S. stock index futures trimmed most of their initial decline.

Here are some comments from market participants in the wake of the Iranian strike Wednesday morning Europe time:

Simmering Tensions

“We think it’s going to simmer behind the scenes for most of the year,” Patrick Armstrong, chief investment officer at Plurimi Wealth LLP, said of U.S.-Iran tensions. “We don’t think there’s going to be much of an escalation right now -- just because if Iran escalates, U.S. policy turns to regime change,” he said. “It’ll be a fragile truce but simmering moments where things will spike.”

“I’m a reluctant bull, I suppose -- it’s driven by central banks,” Armstrong said. “I think the path of least resistence for equities is to grind higher.”

Remember Central Banks

“Yes, it is a step up” in tensions, Viktor Shvets, head of Asian strategy at Macquarie Commodities and Global Markets, a unit of Australia’s biggest investment bank, said of the latest Iran move. “But similar steps up and down will go on. How much one should reflect it in equity markets is a big question mark.”

“My view is simple: central banks are flooding the system with liquidity. So long as that is the case, equity investors are quite willing to expect that central banks will fix economic problems, and politics will fix geopolitical problems -- and that is why equity markets remain quite placid.”

Perfunctory Move

“The market’s remarkable resilience is explained by the fact that investors seem to consider overall that Tehran’s latest strikes are essentially a perfunctory move,” said Stephane Barbier de la Serre, a strategist at Makor Securities. “The market kind of says that diplomacy, however bellicose, is simply meant to take over now, each side having drawn its own line in the sand.”

Even so, volatility is set to rule for a while and the recent developments “probably kill off, once and for all, the ongoing market consensus narrative of an impending cyclical upturn with all the investment implication that it will logically entail,” de la Serre said. He recommends buying dips on anything oil and gold-related as well as shares in defense contractors, and the U.S. dollar, while selling bounces on travel and leisure and shifting from cyclical assets to defensive ones.

Markets Were Unprepared

“The key point is that the market was in no condition for bad news of any kind” before this flare-up, said Doug Ramsey, chief investment officer at Leuthold Group. “The market was bound to react badly to anything less than the best news on the economy, trade war, and even geopolitical tensions.”

“We are positioned right in the middle of our normal 30-70% range for equities in our tactical funds. We do not plan to buy to any dip potentially created by this escalation. Rather, we’d be inclined to sell into a first quarter melt-up if one develops,” he said.

Take on Hedges

“We are doing much more hedging to cut the risks in our portfolio,” said Jackson Wong, asset management director at Amber Hill Capital Ltd. “The main thing we’d do is to buy more derivatives related to some ETFs and indexes to hedge against further declines of the general market.”

“No doubt the stocks related to gold and oil will perform better in the short-term, but I’d be cautious to chase it since the bearish situation might change quickly and I’m not that worried yet,” he said.

Buy U.S. Stocks

“I would still be buying U.S. equities,” said Stefan Hofer, chief investment strategist at LGT Bank Asia. “I wouldn’t want to be too brave at this moment. But I mean, we think about the U.S. consumer, the labor market report will be out I think at the end of this week is probably going to be quite decent. Wage growth is strong, earnings are going to be improving into the first quarter.”

“If we can just set aside the whole political risk issue, ultimately on fundamentals the U.S. is the place to be,” Hofer said.

Trumping Trade War

“Iran has replaced the trade war as the biggest risk to markets -- 2020 has been hijacked by escalating Middle East tensions and investors will be re-positioning their portfolios to reflect this,” said Shane Oliver, head of investment strategy in Sydney at AMP Capital. The yen could strengthen to 105 per dollar, but it would require “serious intensification” of the situation to test that level, he said.

Wait and See

“I don’t expect to adjust my positions” in Chinese stocks, said Raymond Chen, a portfolio manager with Keywise Capital Management (HK) Ltd. “It’s a short-term event amid an economic-recovery trend,” though “it’s possible that there may be misjudgment from both sides” he said, referring to the U.S. and Iran. “I’ll wait and see how things pan out first.”

Oil Capped

“The probability of an irretrievable spiral into outright war remains small,” said Gavekal Research’s Tom Holland. “As a result, it remains likely that the geopolitical risk premium being priced into financial markets will abate over the near term, and that even with further bellicose rumblings, oil will remain capped below $70 a barrel” for West Texas Intermediate and $75 a barrel for Brent, he said.

Other Incidents?

“The biggest risk to my overall take that this will end up being ‘a buy-the-dip and fade the risk-off wave’ will be if we got another geopolitical event on top of this,” said Kay Van-Petersen, a global macro strategist at Saxo Capital Markets in Singapore. He flagged the potential for incidents involving North Korea or China and Taiwan.

--With assistance from Ruth Carson, Cindy Wang, Vildana Hajric, Jeanny Yu, Andreea Papuc, David Ingles, Yvonne Man, Nejra Cehic, Michael Msika and Ksenia Galouchko.

To contact Bloomberg News staff for this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Blaise Robinson

©2020 Bloomberg L.P.

With assistance from Bloomberg