Old Habit Is Hard to Break as Momentum Stocks Surge Back to Top

Old Habit Is Hard to Break as Momentum Stocks Surge Back to Top

(Bloomberg) -- So much for the share rotation from momentum into value that froze equity traders in their tracks last week.

Or so much for it today, anyway. One week after traders soured on the market’s highest flyers, momentum, a strategy of chasing winners and dumping losers, is back in vogue. A Dow Jones measure of market-neutral momentum rallied 3% as of 11 a.m. in New York, while a similar gauge for value, or buying cheap shares against expensive ones, lost 1.5%. It’s the first time since July 2016 that momentum beat value by this much.

The reversal goes into the column of strategists at firms such as Goldman Sachs and Credit Suisse, who say the preference for value stocks is likely to be short-lived without any support in fundamentals. During the past year, recession fears have spurred investors to pile in on assets perceived as safe, with stocks offering high dividends and long-term growth dominating the ranks of winners while economic-sensitive companies trailed the market.

“Absent an improvement in underlying economics, we believe that the recent shift in leadership is unlikely to persist,” Jonathan Golub, chief U.S. equity strategist at Credit Suisse wrote in a note Monday. He called last week’s rotation from momentum to value “the great factor unwind.”

Tuesday’s comeback in momentum versus value was evident on the sector level as well. Defensive shares, such as real estate and consumer staples, led the market, rising at least 0.8%. Energy and financial shares, among the cheapest in the S&P 500, fell at least 0.5% as Treasury yields declined and oil tumbled following Monday’s surge.

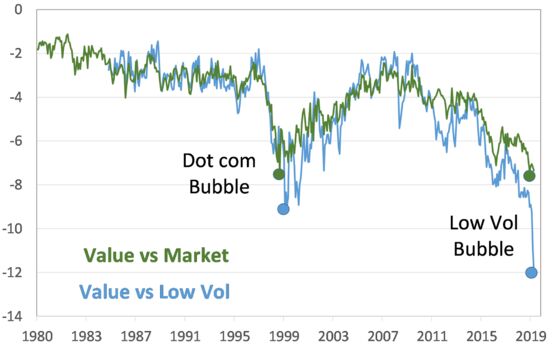

According to JPMorgan Chase, stocks in the value category are trading at a record discount to low-volatility stocks. In a note Monday, a strategist at the firm, Marko Kolanovic, drew a parallel between today’s addition to low-volatility stocks and the persistent bet on market calm in 2017. Back then, that trade imploded, leading to the closure of the VelocityShares Daily Inverse VIX Short-Term ETN, or known as its ticker XIV.

The risk-off trade, as demonstrated by the loathing toward value, is on the cusp of collapsing just like XIV, he said.

“Crowding in this trade reached levels that will ultimately make it another ‘XIV’ (short VIX) trade,” Kolanovic wrote in the note. “We believe the unwind is in its early stages, as evidenced by equity portfolio managers continuing to fight the value rotation towards oil and natural gas sector.”

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.