Oil Slump Offers Scant Relief to Heavily Hedged Airlines

With crude in freefall, hedging positions aimed at protecting against future price increases.

(Bloomberg) --

Plunging oil prices usually boost airlines by bringing down the cost of their biggest expense. But for carriers locked into buying fuel at higher levels, the drop offers little relief from the coronavirus epidemic that has wiped out demand for travel.

With crude in freefall, hedging positions aimed at protecting against future price increases -- such as those taken by Singapore Airlines Ltd., British Airways and Ryanair Holdings Plc -- are now costing carriers money.

Brent tumbled by almost a third to $31 a barrel, the most since the Gulf War in 1991, whereas Singapore Airlines is hedged at $76 on four-fifths of its fuel needs through the end of this month. Among Mideast carriers, the slump could have a more direct effect as it weighs on oil-based economies, hurting demand.

“The dramatic drop in oil prices is nothing to cheer about for airlines this time because virtually no one is traveling,” said Bang Min Jin, an analyst at Eugene Investment & Securities Co. in Seoul, one of the cities worst hit by the outbreak. “Airlines that have little exposure to hedging will be in a better position than those that have bigger exposure.”

That could include leading carriers in the U.S., where high levels of hedging are rare compared with Europe and some other regions.

Devastating Impact

The International Air Transport Association warned on Thursday that airlines may lose $113 billion in sales in 2020 due to Covid-19, almost four times more than estimated two weeks earlier. It also said a fall in fuel prices -- less than what has since occurred -- could cut costs by $28 billion, providing some relief from a “devastating impact” on demand.

Airlines hedge fuel costs in a multitude of ways. Some cover themselves using crude prices, where liquidity is greatest. Others will do so directly in the jet-fuel market. Their actions will often entail the purchase of options enabling them to buy at specific prices.

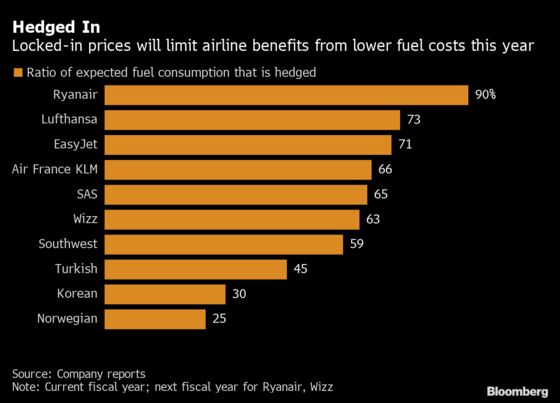

Dublin-based Ryanair has hedged 90% of its fuel requirement at an average of $606 a metric ton for the year beginning April 1, according to a February presentation, equating to about $77 a barrel.

Air France-KLM -- -- which spent 5.5 billion euros ($6.3 billion) on fuel last year -- is locked in at the even higher level of $619 a ton for 2020, or about $78.5 per barrel, though only on two-thirds of its needs, while Deutsche Lufthansa AG is hedged at $63 on close to three-quarters of its annual usage.

British Airways parent IAG SA has hedged more than 90% of its needs in the first three quarters of 2020, it said in an investor presentation last month.

Mideast Blow

Airlines in China and India don’t typically hedge on fuel, though the advantages that Chinese operators in particular will gain from a lower bill are just a drop in the ocean when contending with traffic that’s virtually at a standstill.

Mideast carriers are particularly sensitive to fluctuations in the price of crude. Too low, and bookings from the oil-rich Gulf dries up, too high and the increased bill for jet fuel hurts demand on the inter-continental routes that provide the bulk of business.

Dubai-based Emirates, the world’s largest long-haul carrier, doesn’t hedge against crude and says its ideal price is $60 a barrel, far higher than the current level.

Carriers such as Cathay Pacific Airways Ltd. and Norwegian Air Shuttle ASA have hedged positions below than 40%, potentially conveying an advantage, though for the European discounter the low level is partly a reflection of its debt struggles.

Best Placed

U.S. airlines may be best placed, with larger operators tending not to hedge at all and some of the more domestic-focused ones such as JetBlue Airways Corp. and Southwest Airlines Co. having limited exposure, said George Ferguson, a senior analyst with Bloomberg Intelligence.

“Most of the U.S. carriers are poised to participate in the downside movement to a good degree,” Ferguson said, estimating the oil-price decline could represent “a 20% or 25% cut to their most important cost.”

Should prices stay low for the rest of the year, companies may be able to utilize that to stimulate demand in the second half should an appetite for travel return, he said.

Korean Air Lines Co. hedges only about 30% of its fuel needs, but has cut more than 80% of its capacity due to the coronavirus, so that any benefit from oil’s slide “won’t be much,” a spokeswoman said.

Those carriers that manage to ride out the epidemic may benefit in coming years from being able to hedge at crude’s new lows, with many beginning to lock in prices over the past month.

Read More: Airlines Rush to Hedge Fuel Costs as Virus Triggers Oil Rout

--With assistance from Alaric Nightingale, Jack Wittels, Layan Odeh, Kyunghee Park and Richard Weiss.

To contact the reporters on this story: Siddharth Philip in London at sphilip3@bloomberg.net;Richard Clough in New York at rclough9@bloomberg.net;Kyunghee Park in Singapore at kpark3@bloomberg.net

To contact the editors responsible for this story: Anthony Palazzo at apalazzo@bloomberg.net, Tara Patel, Christopher Jasper

©2020 Bloomberg L.P.