Oil’s Slide Favors India’s Bonds Versus Indonesia, JPMorgan Says

For oil-importing India, the implosion in Brent crude prices will give leeway to heal an economy hurt by virus lockdowns.

(Bloomberg) -- Oil’s epic price collapse is giving Indian bonds the upper hand over Indonesian debt in a market where dollars are in short supply and developing nations compete for foreign money, according to JPMorgan Private Bank.

For oil-importing India, the implosion in Brent crude prices this year will give Prime Minister Narendra Modi’s government leeway to heal an economy hurt by virus lockdowns. That puts Indonesia, a country hit with a bigger current-account deficit and an oil-led decline in commodity prices, at a disadvantage.

“India is a clear winner from the collapse in oil prices, whereas Indonesia loses,” said Alexander Wolf, head of Asian investment strategy at JPMorgan in Hong Kong. “Commodity prices will be the key differentiator” at a time when weak global growth and capital outflows increase the challenges for countries with current-account deficits. Indonesia is the world’s largest producer of palm oil and largest shipper of thermal coal.

India’s domestic bonds have handed investors a loss of nearly 2% in dollar terms in 2020 amid an emerging-market rout, albeit better than the decline of more than 11% for Indonesia, according to Bloomberg Barclays indexes. The Indian rupee has also fared better than Indonesia’s rupiah, Asia’s worst performer this year.

Divergent policy paths also favor Indian bonds as Bank Indonesia’s liquidity injection will probably hurt the rupiah. Indonesia’s monetary authority said it will soon start buying bonds directly from the government, turning to unconventional policy tools even though it has access to the U.S. Federal Reserve’s $60 billion repurchase facility. Meanwhile, the Reserve Bank of India has stopped short of announcing massive bond purchases though it has been buying debt in the secondary market to cool yields.

“We’re not bullish on Indonesian local bonds even with BI potentially being a buyer due to the expectation that that would weaken the currency,” Wolf said.

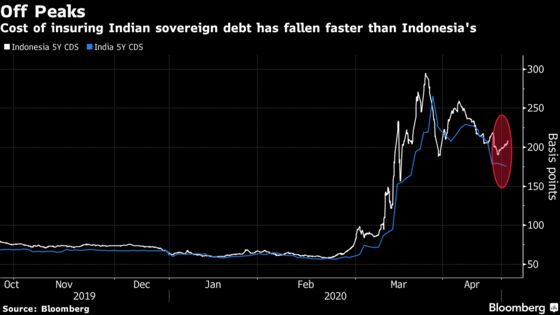

Markets are pricing Indonesian debt as riskier based on credit-default swaps even though it’s rated one level higher than India at BBB by both S&P Global Ratings and Fitch Ratings. Aside from current-account deficits, both countries suffer from a shortfall in their fiscal positions.

Read: Indonesian Bond Yield May Further Narrow Gap to India’s

Indonesia’s local bond market, 32%-owned by foreign investors, is turning into a liability, according to Duncan Tan, currency and rates strategist in Singapore at DBS Group Holdings Ltd. Foreign participation in India’s market, by contrast, is limited by quotas.

“I don’t think Indonesia’s credit rating, being one notch higher, means much,” Tan said. “Ultimately, Indonesian government bonds are a market driven by foreigners and Indian securities by locals. The market dynamics and thus, the impact of central bank action, are very different.”

©2020 Bloomberg L.P.