Oil Closes Under $20 for Second Day Amid Historic Demand Loss

Virus-led demand destruction outweighs an agreement by the world’s biggest crude oil producers to curb supply.

(Bloomberg) -- Oil closed under $20 a barrel for a second day as projections that demand will fall to a 30-year low outweighed an agreement by the world’s biggest producers to curb supply.

Futures in New York ended the day unchanged from the 18-year low set Wednesday. OPEC said it expects demand for its crude to fall to the lowest in three decades as the coronavirus outbreak freezes the global economy, underscoring the urgency of the group’s promised production cuts. OPEC and its allies have agreed to curb output by 10% next month. But even with full compliance, the group would still be pumping more than the market requires in the second quarter.

The cuts “certainly aren’t going to be near enough to balance the market,” said Bart Melek, head of commodity strategy at TD Securities. “There is a good chance, that over the short run, we might even be lower here.”

Inventories from America to Europe and Singapore have all ballooned this week, sending some localized crude prices below $10 a barrel. The glut is looking so severe that the Trump administration is considering paying American companies to leave crude in the ground.

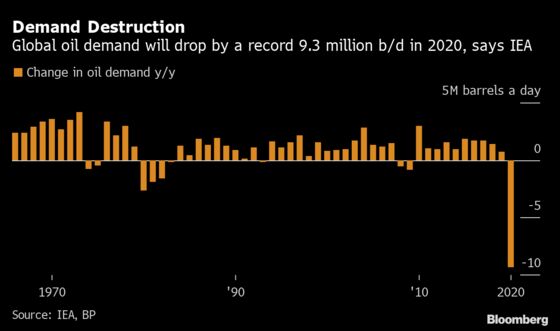

The stock builds come as the International Energy Agency said 2020 may be the worst year in the history of the oil market as lockdowns globally lead to the biggest hit to demand ever.

“This OPEC deal is great and good but it doesn’t help us over the next thirty days,” Rebecca Babin, senior equity trader at CIBC Private Wealth Management, said by phone. “Even with the OPEC agreement, the size and timing of it is not enough to alleviate potential storage issues in the near term.”

All the while physical oil prices, particularly in Europe, are trading far below those of futures. Key North Sea crude swaps are trading at the biggest discount to the headline Brent futures price in almost a decade. The critically important Dated Brent benchmark, which shapes the price of millions of barrels, was assessed by S&P Global Platts at $18.08 on Wednesday, with cargoes across Europe trading at a discount to that value.

As real crude prices and futures markets dislocate, some investors are eyeing a bottom in WTI, with almost $700 million flowing into a key ETF so far this week.

In response to the market downturn, U.S producer ConocoPhillips said it will cut North American output by more than one-fourth and halt all fracking in the continent.

| Prices: |

|---|

|

“What will be the most important determinant for oil markets in the short term is how quickly governments relax social distancing measures,” boosting consumption, said Rystad Energy AS’s head of analysis Bjornar Tonhaugen.

| Other oil-market news |

|---|

|

©2020 Bloomberg L.P.