Oil Falls to 18-Year Low After Record Collapse in U.S. Demand

International Energy Agency said demand would slump by a record this year despite a historic production cut deal.

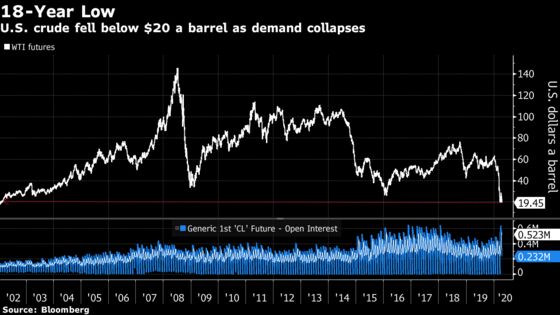

(Bloomberg) -- Oil plunged to the lowest in two decades amid a record collapse in U.S. fuel demand and the biggest ever weekly build in domestic crude supplies.

Futures in New York settled below $20 a barrel for first time since 2002. American gasoline consumption dropped to the lowest level on record while crude supplies ballooned by 19.2 million barrels, according the Energy Information Administration. The government report underscored an earlier forecast by the Paris-based International Energy Administration, which warned that even OPEC+’s historic production cut can’t counter the epic demand decline caused by the coronavirus pandemic.

While Saudi Arabia and other Middle East producers have pledged to cut supply starting next month, they continue to flood the market in April. Meanwhile, U.S. oil production has declined only marginally.

“Whatever production that we are cutting back is not going to offset the demand destruction,” said Stephen Schork, president of the energy consultancy Schork Group Inc.

The oil glut is looking so severe that the Trump administration is considering paying U.S. oil producers to leave crude in the ground.

Oil demand will drop by over 9 million barrels a day this year, wiping out a decade of consumption growth, the IEA said, exhausting storage by mid-year. Consumption in April is expected to fall by almost a third to the lowest level since 1995, making this year the worst in the history of the oil market. Despite OPEC+’s efforts, global inventories will accumulate by 12 million barrels a day in the first half of the year and “overwhelm the logistics of the oil industry” in the coming weeks, the Paris-based agency warned.

| Prices: |

|---|

|

Stockpiles in the U.S. increased for a 12th straight week while European inventories rose the most in more than a year last week. This is weakening key physical market gauges. Swap prices indicate North Sea cargoes are at their biggest discounts to Brent futures in more than a decade.

“At some point, the market will have to start looking forward,” Daniel Ghali, a TD Securities commodity strategist, said by phone. “The OPEC cuts are going to be implemented and also U.S producers will have to reduce their output. Our expectation is we will start to see the market tightening as early as June.”

In talks with OPEC+, the U.S., Canada and Brazil estimated their production will drop by a combined 3.7 million barrels a day

Last week’s decline “should help alleviate any concerns from OPEC+ that the U.S. isn’t doing its part,” Brian Kessens, portfolio manager at Tortoise, said by phone.

| More on the Oil Market |

|---|

|

©2020 Bloomberg L.P.