Oil Slides as OPEC+ Rejects U.S. Call For More Crude

Oil declined as investors turned their focus to an OPEC+ meeting on production policy after U.S. crude stockpiles expanded.

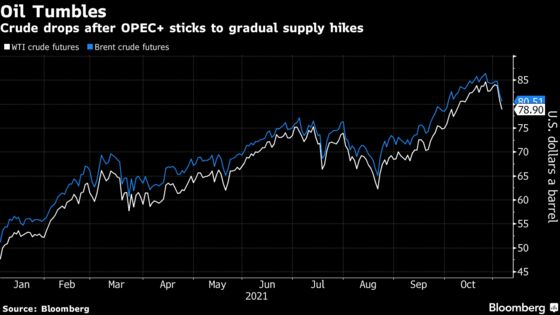

(Bloomberg) -- Oil fell to the lowest in a month after OPEC+ agreed to only maintain its current pace of supply increases despite calls for more output, prompting speculation that the U.S. may tap its strategic reserves.

Futures in New York dropped 2.5% on Thursday in a volatile session. After a brief meeting, OPEC and its allies approved a 400,000 barrel-a-day production hike for December, a delegate said. That’s a pace that major consumer countries say is too slow to sustain the post-Covid economic recovery.

“It makes an SPR release look like a near-certainty I would say,” said Emily Ashford, an analyst at Standard Chartered.

Crude recently rallied to the highest since 2014 as an economic rebound from the pandemic combined with a supply crunch across the energy industry boosted demand. U.S. President Joe Biden has led calls from major consumers for higher OPEC+ production, but Saudi Arabia and others in the alliance pushed back, saying coronavirus outbreaks continue to threaten the market.

The U.S. said Thursday it is encouraging major oil producers to stabilize energy prices. The White House also said it is considering a range of tools to deal with oil prices, according to a National Security council spokesperson after the OPEC+ decision.

“It’s being considered an emergency, or a crisis at this point,” said John Kilduff, a partner at Again Capital LLC. “I would expect the aggressive action on the consumer side.”

Additionally, Russia’s Energy Minister Alexander Novak said Thursday that OPEC and its allies are committed to ensuring market stability and that the group has enough tools to react to a sharp demand recovery.

| Prices |

|---|

|

What happens in the coming weeks will have major implications for a global economy that has been battered by high energy prices, and for the domestic political agenda of a U.S. president whose popularity is sinking as inflation rises. The showdown also puts further strain on America’s increasingly fragile relationship with its strongest Middle Eastern ally -- Saudi Arabia.

“If you released 60 million barrels from the SPR, now you’re looking at maybe $3 a downside,” said Rebecca Babin, senior energy trader at CIBC Private Wealth Management. “What’s starting to get priced in is the fact that the Biden administration painted themselves a little bit in a corner where they have to do something in response to OPEC not doing anything.”

Meanwhile, inventories at Cushing, Oklahoma, the delivery point for benchmark U.S. crude futures, rose by about 1.04 million barrels in the week through Nov. 2, according to traders citing data from Wood Mackenzie on Thursday. That’s a stark reversal after weeks of supply declines.

| Other market news: |

|---|

|

©2021 Bloomberg L.P.