Oil Slides Most in Two Weeks as Traders Doubt OPEC+ Supply Cuts

Crude is paring this year’s losses after OPEC+ defied Trump’s call for the producer group to keep taps open.

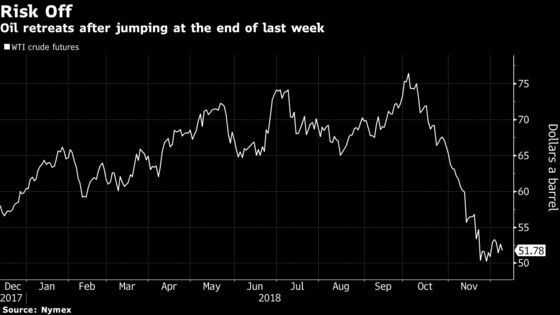

(Bloomberg) -- Oil slid to its worst loss in two weeks as doubts grew about whether OPEC and its allies can deliver enough output cuts to head off a glut.

Futures fell 3.1 percent in New York, evaporating all the gains from last week’s pact between Russia, Saudi Arabia and other top producers to crimp supplies. Worries about demand also took a toll as data showed Chinese imports rising less than expected and Beijing summoned the U.S. ambassador to protest the arrest of a telecom executive.

While the alliance known as OPEC+ agreed to slash about 1 percent of global production, it remains uncertain exactly how the cutbacks will be implemented, analysts at Goldman Sachs Group Inc. and Morgan Stanley noted.

“You can see how the numbers could work out, but it’s not a startling, oh-my-God cut,” said Michael Hiley, head of OTC energy trading at LPS Futures in New York. “It could be enough to turn it positive, but it’s going to be a grind. It’s not a knee-jerk jump upwards.”

American drillers Hess Corp. and ConocoPhillips also announced they’ll maintain or increase spending in 2019, a sign that the recent slide in prices won’t stall the U.S. shale boom.

The Organization of Petroleum Exporting Countries and its partners defied U.S. President Donald Trump’s call to keep the taps open, as producers looked to halt a price collapse. Crude dropped from a four-year high in early October after Washington sought to ease the shock of sanctions targeting Iranian oil exports while American companies pushed output to new records.

West Texas Intermediate futures for January delivery declined 3.1 percent to close at $51 a barrel on the New York Mercantile Exchange.

Brent for February settlement fell $1.70 to $59.97 on London’s ICE Futures Europe exchange. The global benchmark crude traded at a premium of $8.87 to WTI for the same month.

The OPEC+ deal is testament to the strength of Saudi Arabia’s two-year-long cooperation with Russia and showed Crown Prince Mohammed bin Salman is willing to defy Trump’s wishes even after the the murder of journalist Jamal Khashoggi.

Still, uncertainty remains given the OPEC+ deal doesn’t specify country allocations and exempts Libya, Venezuela and Iran, according to Goldman Sachs. While Morgan Stanley said the cuts will probably be sufficient to balance the market in the first half of next year, the bank sees limited upside to prices and cut its Brent price forecast by $10 a barrel for 2019.

In another sign of pessimism about oil prices, the gasoline crack spread -- a rough measure of the profitability of producing fuel -- fell during the day to about $8.70 a barrel. A margin above $10 would encourage refineries to use more crude and is “one of the necessities of any sustained rally,” said Bob Yawger, futures director at Mizuho Securities USA.

| Other oil-market news: |

|---|

|

--With assistance from Sharon Cho.

To contact the reporters on this story: Alex Nussbaum in New York at anussbaum1@bloomberg.net;Grant Smith in London at gsmith52@bloomberg.net

To contact the editors responsible for this story: Simon Casey at scasey4@bloomberg.net, Joe Carroll, Reg Gale

©2018 Bloomberg L.P.