Oil Falls as Hurricane Dorian, Trade Wars Stoke Demand Fears

Oil held losses after its first monthly drop since May as a deepening trade war with no end in sight stoked global growth fears.

(Bloomberg) -- Oil fell as demand concerns weighed on the market with Hurricane Dorian taunting the U.S. East Coast this week, and the U.S.-China trade war unresolved.

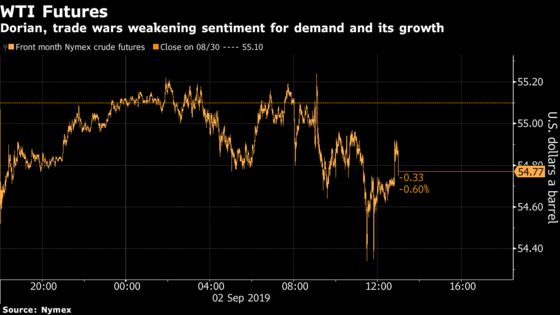

Futures were 0.6% lower at the halt of trading in New York Monday after sinking as much as 1.4% in New York. While Dorian, which reached category 5 strength over the weekend, probably won’t affect U.S. crude production and refining, it will dampen demand for gasoline and diesel.

“Products are leading the market down” and crude is following, said Andy Lipow, president of Lipow Oil Associates LLC. Despite the U.S. Labor Day holiday which ended trading early, “there was decent volume,“ he said.

The storm’s forecast path remains uncertain although it’s expected to move “dangerously close” to the Florida shoreline later Monday or earlier Tuesday.

New U.S. tariffs on Chinese goods, which took effect on Sunday, are fueling demand fears even more. The outlook for Chinese manufacturing deteriorated further in August, the latest evidence that the U.S.-China trade conflict is taking a toll on the global economy. Meanwhile, Chinese and U.S. officials are struggling to agree on the schedule for a planned meeting this month, according to people familiar with the discussions.

“Economic uncertainty will continue to dominate the oil market’s agenda as new U.S. and China trade measures come into effect,” said Harry Tchilinguirian, head of commodity-markets strategy at BNP Paribas SA. “The market is more and more resigned to a protracted stand-off and will be looking toward central-bank easing to shore up risk appetite to help overcome the prevailing hesitancy in going long oil.”

Poor economic data from Germany and U.K. also weighed on the market at a time when the latter is trying to resolve its own trade dispute, Lipow said. Prime Minister Boris Johnson put the U.K. on notice that it faces the threat of an election within weeks, as the political crisis engulfing the country’s divorce from the European Union deepened.

West Texas Intermediate for October delivery fell 33 cents to $54.77 a barrel on the New York Mercantile Exchange at 12.59 p.m., after reaching an intraday low of $54.34. Transactions will be booked Tuesday for settlement because of the U.S. Labor Day holiday. The contract lost $3.48 in August.

Brent for November settlement slid $1.77 to $58.66 a barrel on the ICE Futures Europe Exchange, and traded at a $4.07 premium to WTI for the same month. The October contract expired on Friday, having lost 7.3% last month.

| Other oil-market news: |

|---|

|

To contact the reporters on this story: Grant Smith in London at gsmith52@bloomberg.net;Sheela Tobben in New York at vtobben@bloomberg.net

To contact the editors responsible for this story: David Marino at dmarino4@bloomberg.net, Catherine Traywick, Steven Frank

©2019 Bloomberg L.P.