Oil Crash Adds New Shock to Limping World Economy

Oil Crash Adds New Shock to Limping World Economy

(Bloomberg) -- The historic collapse in the price of oil is inflicting another shock on a weakened world economy, creating a disinflationary risk for some and severely denting budgets in producers from Saudi Arabia to Russia and Canada.

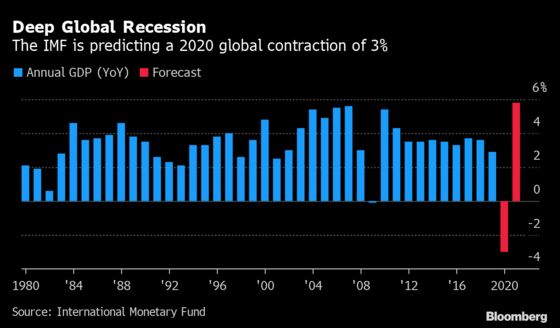

The rock-bottom price comes amid the worst global slump since the Great Depression, which has already led to interest-rate cuts and other stimulus, stretching the capacity of monetary policy makers once again. In addition to hitting crucial revenue for traditional oil producers, the latest price drop also threatens America’s nascent shale revolution.

The upshot is that although cheap fuel typically provides something of a tax cut for many households and businesses, the fact that so many are locked down by the coronavirus means this time it will likely do more harm than good to the recession-hit global economy.

“The latest tumble in the price of crude below zero may prove a temporary aberration, but for the world economy it is a reminder that the wheels of commerce are firmly stuck in the mud, and that it will take some time to extricate them,” said Frederic Neumann, co-head of Asia economic research at HSBC Holdings Plc in Hong Kong.

A deal among OPEC and its allies has so far failed to reverse the trajectory as news on the demand side keeps getting worse. Oil edged up in Asia trade Wednesday after two days of spectacular routs that saw prices turn negative for the first time ever.

“It is not easy for oil producers to turn off the tap, so they need somewhere to store it until they can find a buyer,” said Christian Downie of the Australian National University, whose expertise includes international energy. “The problem is there is very little storage left, so producers are literally paying buyers to take it off their hands, hence the negative prices.”

The oil slump is another challenge for central banks if it persists and feeds through to broader price trends. They’ve already cut interest rates and relaunched massive bond-buying programs to support economies through crippling shutdowns, meaning their capacity to fight another inflation battle is sorely diminished. Oil demand will take “a long time to recover,” former BP CEO John Browne told Bloomberg Television.

Swinging oil prices impact economies in different ways. Countries that are net energy importers would ordinarily see household income and spending get a boost. China is the world’s largest oil importer, but its economy contracted the most in decades over the first three months of the year.

Emerging economies that dominate the list of oil-producing nations are vulnerable to a collapse in revenues that will pressure current-account deficits and tip companies toward default.

Read More: The Economics of Oil

While the extreme moves seen Monday in U.S. prices weren’t reflected in global benchmark Brent, the collapse in energy demand had already blown out budgets across the oil-rich Middle East. Bahrain, one of the most indebted members of the six-nation Gulf Cooperation Council, followed neighbors this week in announcing drastic spending cuts.

Saudi Arabia, which sent prices spiraling when it ramped up production this year to put pressure on rival Russia, is also feeling the pain. The kingdom needs an oil price of around $80 to balance its budget, and with Brent currently below $25, its deficit is expected to more than double this year to around 10% of GDP.

The collapse in prices would also inevitably raise questions over the stability of currency pegs maintained by some oil exporters, as the decline in revenue squeezes foreign-currency reserves. The IMF expects Saudi Arabia’s revenue to drop to 26% of economic output this year, the lowest since 1999.

Some of the stress is reflected in the bond market. Oman, seen as the most vulnerable Gulf Arab economy to oil-price shocks, saw the yield on its Eurobonds due in 2029 rise from under 6% at the beginning of March to about 10.7% on Tuesday, according to data compiled by Bloomberg.

“For large oil producing countries it is a double blow, or even triple blow if they are heavily indebted -- it will amplify the initial hit to these economies and will make it harder for them to recover,” said Rob Subbaraman, head of global macro research at Nomura Holdings Inc. in Singapore.

Read More: Oil Storage Filling Up Is a Real Threat, and Few Options Exist

The U.S. is also vulnerable. The oil and gas industry shed nearly 51,000 drilling and refining jobs in March, according to BW Research Partnership, a research consultancy, which analyzed Department of Labor data combined with the firm’s own survey data.

The last bust in the U.S. shale industry -- when prices went as low as $26 -- contributed to a manufacturing recession in 2016.

U.S. President Donald Trump on Monday told reporters he wants to take advantage of the lower prices to add as much as 75 million barrels of oil to the nation’s Strategic Petroleum Reserve. He also acknowledged that global demand for oil has plummeted.

“The problem is nobody’s driving a car, anywhere in the world, essentially,” said Trump.

©2020 Bloomberg L.P.