Not Much Has Changed for Europe’s Worst Performers

Not Much Has Changed for Europe’s Worst Performers

(Bloomberg) -- Taking Stock made the point last month that strong conviction was needed to be long European banks. Since then, the ECB has cemented the prospect of low rates, while efforts to mitigate the impact are seen as limited. What’s more, global uncertainty poses a risk to lending growth and to bad-loan provisions, while regulation is weighing on capital buffers and potential shareholder returns. So no wonder, then, that many analysts are cautious on the sector ahead of the earnings season, seeing cherry picking as the best way to build exposure.

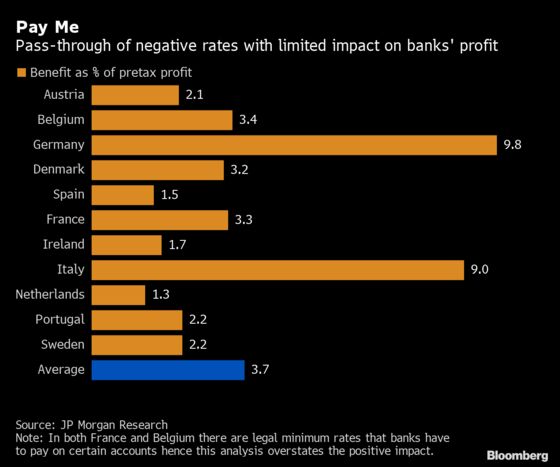

Banks may only derive a small benefit from tiering, which seeks to alleviate the pain of negative rates on money deposited by lenders at the central bank, JPMorgan analysts, led by Kian Abouhossein, estimate. And it remains to be seen how many lenders are willing to pass on negative yields to their clients. Even if they do, the average positive impact on pretax profit might just be shy of 4%.

Although Italian and German banks may benefit the most, tiering isn’t a game changer, JPMorgan said, estimating returns on equity for lenders in the latter nation may improve only modestly to 3% from 2.4%.

The latest European Banking Authority estimates on the effect of the so-called Basel IV rules suggest they still pose a “material risk” to capital returns, according to analysts at Citigroup. The comments are echoed by Mediobanca, which stresses that although lenders’ financial strength still looks adequate at the moment, there’s little excess capital seen in the years ahead, indicating poor prospects for shareholders.

In such a tough environment, it’s little wonder that banks are continuing their pursuit of cost control with reports this week of thousands of job losses from HSBC to Commerzbank.

Bank of America Merrill Lynch sees more risks for banks if monetary policies worldwide are unable to limit the effects of the trade dispute and a global slowdown. An absence of momentum in traditional bank lending and higher credit costs, and the rise of a loosely regulated shadow banking are among the potential threats.

With fundamental challenges unresolved this year, any share price relief in recent months has been brief with the overall picture showing a downtrend.

The misery for shareholders is clear with the Stoxx 600 Banks index down 5.9% this year -- the only sector in red in Europe. It’s also the worst-performer on a five and 10-year basis.

Going forward the risk/reward profile may remain unfavorable. BofAML expects 14% upside for EU banks in a base-case scenario with no global recession, while on the contrary a global downturn could lead to a 25% downside.

Banks’ valuations also present something of a coin flip for some analysts. With levels comparable to those of the 2008 and 2012 crises, either another catastrophe is in the making or there is value worth exploring, Mediobanca analysts wrote in a note earlier this week.

If the cheapness that banking stocks offer on paper is irresistible, stock picking might resemble a treasure hunt. Look for lenders that have made material improvements in de-risking to sustain their returns, the Mediobanca analysts recommend.

In the meantime, Euro Stoxx 50 futures are up 0.2% ahead of the European open, while S&P 500 contracts are down 0.2%.

- Watch luxury stocks, particularly Kering and Hermes, after LVMH reported 3Q fashion and leather sales that RBC called “impressive,” likely allaying some investor concern over the potential impact from protracted social upheaval in Hong Kong.

- Watch the pound and U.K. stocks ahead of a meeting between Prime Minister Boris Johnson and his Irish counterpart Leo Varadkar to try find a compromise. Meanwhile, Johnson’s Labour Party rival Jeremy Corbyn said he is ready and “champing at the bit” for an early U.K. election.

- Watch trade-sensitive stocks as talks resume in Washington amid mixed signals that led to a volatile trading session in Asia. Washington is looking at rolling out a previously agreed currency pact with China as part of an early harvest deal that could also see a tariff increase next week suspended.

COMMENT:

- “Earnings estimates are coming down again for the FTSE 100, and we expect more negatives as companies report 3Q results,” Bloomberg Intelligence strategists Tim Craighead and Laurent Douillet write in a note. “With depressed oil and metal prices dragging down energy and materials heavyweights, and Brexit angst hurting domestic activity, defensive stability in global staples and health care are being overwhelmed.”

NOTES FROM THE SELL SIDE:

- Saint-Gobain offers exposure to attractive end-markets, a good regional footprint, and margin support from organizational restructuring, Morgan Stanley says in upgrading the stock to overweight.

COMPANY NEWS AND M&A:

- Philips Sees Lower ‘19 Adj. Ebitda Margin Raise on Headwinds (2)

- LVMH 3Q Sales Beat Estimates Despite Difficult Hong Kong Context

- LafargeHolcim Is Said to Decide Against Bid for BASF Unit

- UCB to Buy Ra Pharmaceuticals for $48/Share in Cash

- BBVA Seeks to Sell EU1.3B Real Estate Portfolio: Confidencial

- Uniper Deputy Chairman Says Fortum Is Still Hostile to Interests

- Pandora Director Opens Door to Products Besides Jewelry: Borsen

- Salini Impregilo Gets EU388m Railway Contract in Norway

- Euronext Sept. Equity Derivatives Avg. Daily Volume -0.6% Y/Y

- Givaudan 3Q Sales 1.3% Below Estimates (1)

- Suedzucker Maintains FY Operating Profit EU0 To EU100 Mln

- Ukraine Seeks to Add Ferrexpo CEO to International Wanted List

- Tryg Third Quarter Pretax Profit Misses Estimates

- Bossard Confirms FY Sales, Ebit Margin Targets (1)

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 380.5 (50-DMA); 395.1 (July high); 397.9 (June 2018 high)

- Support at 376.8 (200-DMA); 365.5 (50% Fibo)

- RSI: 44.1

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,573 (July high); 3,596 (May 2018 high)

- Support at 3,436 (50-DMA); 3,403 (61.8% Fibo); 3,365 (200-DMA)

- RSI: 47.6

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Hurricane Energy upgraded to overweight at Barclays; PT 55 Pence

- Neoen upgraded to buy at SocGen; PT Set to 27.50 Euros

- Pennon upgraded to overweight at Barclays; PT 10 Pounds

- Rio Tinto upgraded to buy at HSBC; PT 48.50 Pounds

- Saint-Gobain raised to overweight at Morgan Stanley; PT 42 Euros

- Veolia upgraded to outperform at Macquarie; PT 27.50 Euros

DOWNGRADES:

- Ferrexpo downgraded to underweight at Barclays; PT 1.10 Pounds

- Rheinmetall cut to hold at Deutsche Bank; PT Set to 115 Euros

- SIG downgraded to hold at Panmure Gordon; PT 1 Pound

- Suez downgraded to add at AlphaValue

- Wartsila Downgraded to Hold at Pareto Securities; PT 10 Euros

INITIATIONS:

- BPER Banca resumed at citi with Neutral; PT 3.80 Euros

- DSV Panalpina A/S resumed at citi with Neutral; PT 675 Kroner

- Moncler rated new buy at China Renaissance; PT 40 Euros

- TeamViewer Rated New Buy at Commerzbank; PT 36 Euros

- Titan Cement International rated new underperform at Exane

MARKETS:

- MSCI Asia Pacific down 0.5%, Nikkei 225 up 0.4%

- S&P 500 up 0.9%, Dow up 0.7%, Nasdaq up 1%

- Euro up 0.16% at $1.0988

- Dollar Index down 0.09% at 99.03

- Yen down 0.03% at 107.51

- Brent down 0.1% at $58.3/bbl, WTI down 0.1% to $52.5/bbl

- LME 3m Copper up 0.7% at $5722/MT

- Gold spot up 0.1% at $1506.7/oz

- US 10Yr yield down 1bps at 1.58%

ECONOMIC DATA (All times CET):

- 8:45am: (FR) Aug. Industrial Production YoY, est. 0.1%, prior -0.2%

- 8:45am: (FR) Aug. Manufacturing Production YoY, est. -0.2%, prior -0.3%

- 9am: (SP) Aug. House transactions YoY, prior 3.8%

- 10am: (IT) Aug. Industrial Production MoM, est. 0.1%, prior -0.7%

- 10am: (IT) Aug. Industrial Production NSA YoY, prior 2.4%

- 10am: (IT) Aug. Industrial Production WDA YoY, est. -1.8%, prior -0.7%

- 10:30am: (UK) Aug. Index of Services MoM, est. -0.1%, prior 0.3%

- 10:30am: (UK) Aug. Monthly GDP (3M/3M), est. 0.1%, prior 0.0%

- 10:30am: (UK) Aug. Manufacturing Production MoM, est. 0.2%, prior 0.3%

- 10:30am: (UK) Aug. Manufacturing Production YoY, est. -0.4%, prior -0.6%

- 10:30am: (UK) Aug. Construction Output MoM, est. -0.4%, prior 0.5%

- 10:30am: (UK) Aug. Construction Output YoY, est. -0.2%, prior 0.3%

- 10:30am: (UK) Aug. Industrial Production YoY, est. -0.8%, prior -0.9%

- 10:30am: (UK) Aug. Index of Services 3M/3M, est. 0.2%, prior 0.2%

- 10:30am: (UK) Aug. Visible Trade Balance GBP/Mn, est. £10.0b deficit, prior £9.14b deficit

- 10:30am: (UK) Aug. Trade Balance Non EU GBP/Mn, est. £2.8b deficit, prior £1.93b deficit

- 10:30am: (UK) Aug. Trade Balance GBP/Mn, est. £1.05b deficit, prior £219.0m deficit

- 10:30am: (UK) Aug. Monthly GDP (MoM), est. 0.0%, prior 0.3%

- 10:30am: (UK) Aug. Industrial Production MoM, est. 0.1%, prior 0.1%

--With assistance from Michael Msika, William Canny and Chiara Remondini.

To contact the reporter on this story: Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.