Wall Street Goes Slightly Crazy Each Weekday Afternoon. Here’s Why

Just after 4 p.m. each day, Wall Street goes slightly crazy.

(Bloomberg) -- Just after 4 p.m. each day, Wall Street goes slightly crazy. Equity exchanges snap to life for a few seconds as banks, brokers and market makers submit to a process called the closing auction, in which humans and computers pair off $15 billion worth of stock to set a final price for thousands of companies.

It’s a miracle of computer science, one of the securities industry’s big shows of technological force. But it’s not quite the seminal event of equity pricing that many investors assume it to be.

At least, that’s a takeaway from a study by Boston College’s Vincent Bogousslavsky and Michigan State University’s Dmitriy Muravyev, which found that for all the firepower brought to bear, quotes printed in the end-of-day rush have a habit of vanishing after it ends. They found the price of the average stock lurches about 8 basis points as the auction climaxes -- then, when everything subsides, quietly slips back to where it was before.

“The closing price is distorted by the huge trading volume executed in the auction,” said Bogousslavsky in an interview. Past research found auctions improve market efficiency and liquidity, but “there is no price discovery at all at the auction because there is complete reversal” by the next day.

An explanation offered by the authors is that the process has become dominated by players who don’t exactly qualify as the smart money. So many price-insensitive investors -- ETFs, index mutual funds, options arbitragers -- make use of the auctions, that the outcome is briefly warped by the crush of their giant orders. From that perspective, the post-auction drift is just a return to the market’s natural state.

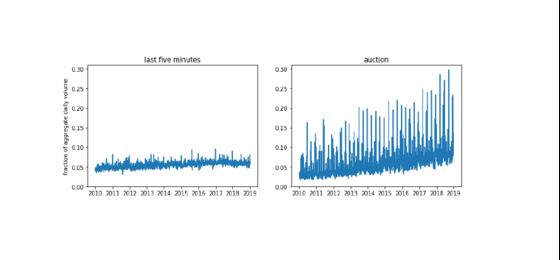

Whatever the quirks, closing auctions have become a focal point of the American equity session, in some respects the only trade that matters for companies listed on the New York Stock Exchange and Nasdaq Stock Market. Orders to buy and sell millions of shares get matched at a single price, formally ending the 6 1/2-hour trading day. The auctions accounted for more than 7% of daily trading dollar volume last year, up from about 3.1% of the daily total in 2010, according to the study.

The exercise is especially important for many types of passive investors, who like to trade at day’s end so their prices are the same as the official close. But the volume being transacted in the auctions have gotten so big it may be warping the process, the authors wrote. That’s likely to get worse as the $4 trillion space continues to grow.

A central irony is that while many Wall Street firms use the auction because it’s where all the liquidity is, the crush of orders that get executed ends up creating imbalances that momentarily yank prices off their moorings. Deviations are large enough to account for 5% of the average daily return in exchange-listed stocks, the paper says.

None of this is to say the closing auction doesn’t work. It may be the best option out there given how many different constituencies make use of it, the authors concede. The study concedes that the deviations they found aren’t huge, often occurring within the spread of the last trade. But the idea that the auctions are a route to finding a sort of sacrosanct quote for stocks, upon which everything from margin calls to derivative prices are based, isn’t quite borne out by their research.

A NYSE spokesperson said its official closing prices “are the benchmark for investors because market participants operate in a real world where supply and demand exist. The NYSE closing auction is the world’s largest single liquidity event for securities trading and results in more stable price discovery than purely electronic markets.” A Nasdaq representative pointed to research from its chief economist, Phil Mackintosh, who found that the end-of-day auction reduces price volatility, among other things.

“Closing auctions handle huge volume, which will only increase as passive investing continues to expand,” Bogousslavsky and Muravyev wrote in the report titled “Should We Use Closing Prices? Institutional Price Pressure at the Close.” But not only does it create price distortions for ETFs, it also results in erroneous and costly executions elsewhere, including margin calls and forced margin selling, they said.

The deviations are more prevalent for small and high-volatility stocks, the authors found, and are “consistently larger” for stocks for NYSE than for Nasdaq auctions. The NYSE auction is less transparent, more complex, and gives priority to floor brokers, they said.

To contact the reporter on this story: Vildana Hajric in New York at vhajric1@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.