New Normal for India’s Record Borrowing Puts Heat on Bonds

“You’ll continue to see a reasonably steep government bond curve.”

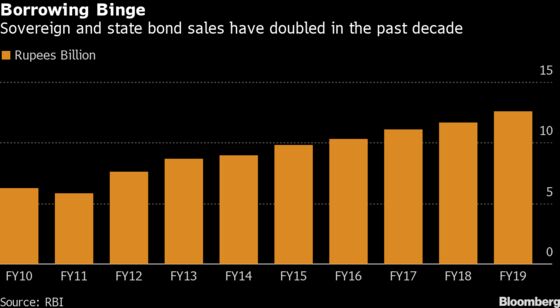

(Bloomberg) -- The Indian government’s record debt sales this year are part of a new normal for the country, and that’s going to keep long-tenor bonds under pressure despite Asia’s most aggressive easing cycle, says a market veteran.

“One possibility is that the size of borrowings year-on-year will remain high and there is unlikely to be a reduction in supply,” Ashish Parthasarthy, treasurer at HDFC Bank Ltd., the nation’s most valuable lender, said in an interview. “You’ll continue to see a reasonably steep government bond curve.”

Last month’s surprise $20 billion tax break for companies and the sluggish growth in tax revenue have sparked concerns about the government missing budget deficit targets. Bonds have struggled in recent weeks despite the central bank cutting interest rates for the fifth time this year in early October.

“Investors are scared of higher borrowings and are staying away,” said Parthasarthy, who has been in the markets for more than two decades. “Till that clarity comes, market sentiment will remain edgy and fragile.”

Further reduction in borrowing costs signaled by the central bank may not spur demand for longer-dated notes as the easing cycle is likely winding down, Parthasarthy said, echoing a view from lenders including Kotak Mahindra Bank Ltd.

“I expect another 25 basis-point cut, and at best 50 basis point cut this fiscal year,” he said.

The yield on the most-traded bonds due in January 2029 fell one basis point to 6.68% on Friday. Yields climbed by 33 points in the two months through September.

Excerpts from the interview:

- “High fiscal deficits of both the center and the state are not going away in a hurry and these are going to continue for the next few years.” Hence, bond yield “curve will be steeper on a secular basis.”

- “Another factor weighing on bonds is the absence of demand from the RBI. As the liquidity is ample, the need to do open-market operations is coming down.”

- “The new 10-year is around 6.50%. Even if you have a cut in December, which is likely, I don’t see it changing significantly because by then you’ll anticipate additional borrowing.”

- “The long-end won’t benefit as majority of the bond supply is there.” We like shorter-maturity bonds up to five years.

To contact the reporters on this story: Kartik Goyal in Mumbai at kgoyal@bloomberg.net;Garfield Reynolds in Sydney at greynolds1@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Ravil Shirodkar

©2019 Bloomberg L.P.