Neuberger Says Turkish Stocks to Keep Discount, Even After Rally

Neuberger Says Turkish Stocks to Keep Discount, Even After Rally

(Bloomberg) -- Turkish stocks may have ascended to record highs this week, but they are unlikely to close a gaping discount to historical valuations because of a batch of local factors that temper investor enthusiasm, according to Neuberger Berman.

“When you look at a cheap market, you wonder if it will go back to its historical average,” Marco Spinar, an associate portfolio manager at Neuberger Berman, said in an interview. In Turkey’s case, the market could rally without ending the disparity, said Spinar, who helps oversee $8 billion in developing nation shares at the New York-based money manager, including Istanbul stocks.

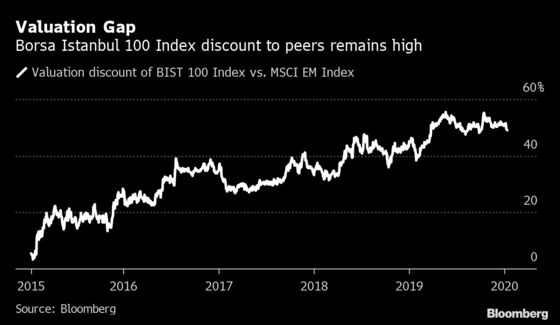

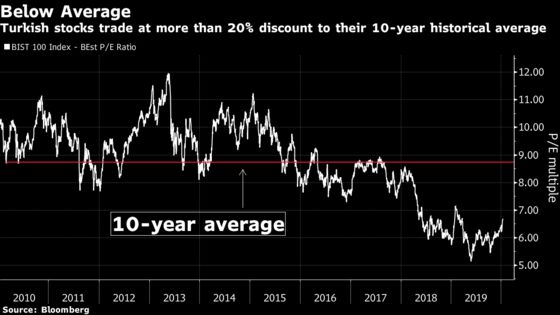

The benchmark index climbed to an all-time high Wednesday, with investors drawn by an upbeat outlook from some local banks, reduced Iran-U.S. tensions and attractive valuations. Turkish stocks trade at about 23% below their 10-year average price to earnings basis, with a gulf of 49% to emerging-market peers.

Valuations have lagged for more than five years, “frustrating” investors, Spinar said. The Turkish market has been battered in this period by the turmoil of three general elections, a local government vote, a referendum on the president’s powers, a failed coup, cabinet changes, terror bombings, a currency crisis, strained relations with the U.S. and an economic slowdown.

The gap is set to remain “as long as Turkey has weak macro institutions,” said Spinar, who has a neutral stance on the market. He cited inflation and a weak central bank among the strongest negative factors.

“There has been a real change in economic policy for the worse that has made it tough to invest in Turkey,” Spinar said. “It’s a much unloved market. It’s very cheap. But we haven’t seen a real change in fundamentals, a return to a better-thought-out, more strategic economic plan.”

In July 2019, President Recep Tayyip Erdogan unexpectedly replaced central bank Governor Murat Cetinkaya. His successor, Murat Uysal, has overseen 1,200 basis points in cuts to the key lending rate. Shortly after the change, Erdogan told a closed meeting of his party’s lawmakers that he expected Uysal and other bureaucrats and politicians to toe the government’s line on monetary policy and his view that higher interest rates cause inflation.

A year earlier, Erdogan also drew investor criticism for appointing his son-in-law as economy czar, completing the gradual removal of a markets-friendly government economic management team.

Given their valuations and with a tailwind of a benign backdrop for emerging markets, Turkish stocks could outperform, even without any investor-friendly changes at these institutions, said Spinar. But the risks leave them “very vulnerable” to a sell-off or deterioration in sentiment.

Spinar’s Turkish holdings are concentrated in companies that he regards as having strong management and a good return on equity, including fashion retailer Mavi Giyim Sanayi Ve Ticaret AS, white-goods manufacturer Arcelik AS, and non-state lenders like Akbank TAS and Turkiye Garanti Bankasi AS.

Neuberger holds a “constructive view” on emerging markets and expects another “reasonably good performance” in 2020, Spinar said. Here are his views on some other countries and regions:

South Africa

- “We’re taking a look at the country, but we’re underweight. We did have enthusiasm originally when Ramaphosa took over, but we became a bit frustrated and started to cut back about a year ago. We’re not yet ready to go back.”

Saudi Arabia

- Seen “amazing” cultural changes and improvement in the quality of company management

- “The market got very expensive going into the nation’s inclusion into the EM index. It has been a pretty big underperformer since then. That can be a pretty typical transition for a country, especially one like Saudi that had no foreign participation at all.”

- “I’m sure Saudi will probably remain a pretty expensive country. Currently we don’t have any exposure. But we definitely have been spending a lot of time looking at the country.”

Eastern Europe

- Russia is of particular interest, Neuberger is overweight on eastern Europe if Russia is included

- “Poland has controlled inflation, quite impressive economic growth.”

- “We have exposure in the Czech Republic financial space. I wish the market was a little more liquid and a little deeper.”

To contact the reporter on this story: Tugce Ozsoy in Istanbul at tozsoy1@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, ;Onur Ant at oant@bloomberg.net, John Viljoen, Paul Jarvis

©2020 Bloomberg L.P.