Barnett’s Invesco Exit Brings Curtain Down on Woodford Era

Neil Woodford Protege Mark Barnett Leaves Invesco After 24 Years

Mark Barnett’s departure from Invesco Ltd. after 24 years brings an end to the legend of his once-feted mentor Neil Woodford.

Invesco Chief Investment Officer Stephanie Butcher said on Friday that Barnett’s departure and other changes to the firm’s U.K. equity funds were made after “a period of disappointing performance and listening hard to client feedback.” He took over management of Woodford’s funds when the star stock picker left Invesco in 2014, but struggled to duplicate his mentor’s past performance.

Barnett’s demise owed in part to his continuation of Woodford’s strategy of investing in thinly traded and unlisted companies, a similarity cited by Morningstar Inc. when it downgraded two of his funds late last year. Barnett rejected the comparison and concerns about the liquidity of his funds, but investors thronged toward the exit.

More recently, the coronavirus sell-off dealt Barnett a blow from which he couldn’t recover. The Invesco High Income Fund, which he helped manage, plunged 37.6% this year through May 14, according to data compiled by Bloomberg.

Taking over Woodford’s funds at Invesco was a “poisoned chalice,” said Bev Shah, founder of City Hive, an advocacy group in London that promotes diversity in the investment management industry. “Barnett was handed the funds and expected to continue running them like Neil,” she said.

‘Odd Time’

The clouds quickly gathered over Barnett following the Morningstar downgrade. His run as sole head of Invesco’s U.K. equities came to an end shortly thereafter with the appointment of Martin Walker as his co-pilot. In December, he was fired by Edinburgh Investment Trust Plc as its fund manager. Since the downgrade, the High Income Fund has seen over 1 billion pounds ($1.2 billion) of outflows, according to Morningstar data.

Ben Yearsley, investment director at Shore Financial Planning, said Barnett’s departure had been coming for some time because of poor performance and withdrawals, but the timing of the announcement was somewhat unexpected.

“Invesco has a business to run and has to make a profit for its shareholders,” he said. “They got fed up. Still, it seems an odd time to do this, in the middle of the virus when value and dividend stocks have been hammered and could see a rebound.”

Barnett said in a statement that he’s “extremely proud” of his career at Invesco.

Walker now assumes full control of the U.K. equities division, with James Goldstone and Ciaran Mallon co-managing the open-ended funds Barnett had run, according to the statement.

Star Manager

Barnett’s struggles at Invesco show the difficulty asset managers face when they try to replace a star manager such as Woodford. Swiss investment firm GAM Holding AG saw its assets and market value plunge after it suspended Tim Haywood, who ran some of the firm’s biggest bond funds. After Bill Gross abruptly left Pacific Investment Management Co. in 2014, the firm suffered more than $300 billion in outflows.

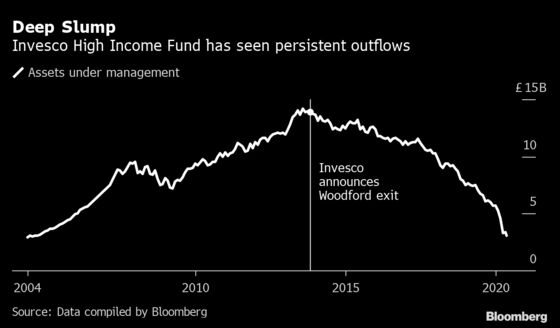

In 79 months since Woodford’s decision to leave Invesco, the High Income Fund suffered outflows in 74, according to Morningstar data. In total, nearly 11 billion pounds ($13.4 billion) have been pulled, shrinking assets to its lowest level since 2004.

Though Barnett came in with his own track record of beating peers, the comparisons with Woodford never stopped. Investors first punished him for not being Woodford by withdrawing billions of pounds, and more recently they fled because his investment style and bets reminded them of his mentor, whose investing empire came crashing down last year under the weight of heavy redemption requests.

Barnett began his investment career in 1992 at Mercury Asset Management. He joined Invesco four years later and worked with Woodford for more than 17 years. Sitting near each other in an open-office plan at the firm’s Henley-on-Thames office about 40 miles west of London, they ran separate funds, but had similar ideas on picking stocks. Both combined macro-economic analysis with company specific trends to buy cheaply valued securities. They also shared the love for small and mid-size and companies even though their funds’ main objective was to build a portfolio of dividend-paying stocks.

©2020 Bloomberg L.P.