The Debate Over This Winning U.S. Equity Trade Is Heating Up

The Debate Over This Winning U.S. Equity Trade Is Heating Up

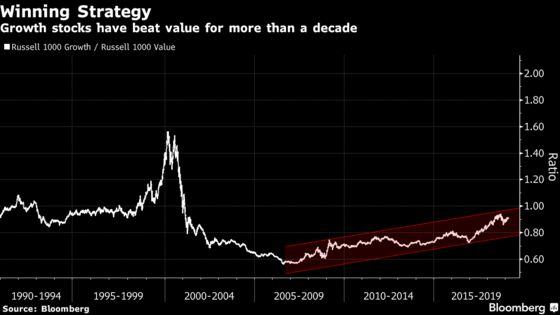

(Bloomberg) -- The debate over a decade-long winning trade is heating up in the U.S. equity market.

Shares of the fastest-growing companies will extend their record stretch of leadership over those seen as cheaper relative to earnings or book value, according to Ned Davis Research. The firm shifted its preference after recommending investors hold growth and value stocks equally based on benchmarks.

Meanwhile, Goldman Sachs, a long-standing bull on growth stocks, is scaling back its optimism, saying stretched valuations mean little room for outsize returns. The firm’s basket of 50 companies with the fastest 2019 revenue growth trades at 21 times forecast earnings, compared with a multiple of 17 for the S&P 500. The premium put the group in the 78th percentile over the past four decades.

“Stable economic growth and elevated basket valuations suggest less potential for outperformance,” Goldman strategists led by David Kostin wrote in a note late Tuesday.

In a quarterly rebalance, Goldman replaced 32 stocks to its sector-neutral growth basket. The new entrants include: Cigna, Twitter, Marathon Petroleum and Berkshire Hathaway.

Ed Clissold, chief U.S. strategist at Ned Davis Research, is less concerned about valuations. Growth stocks deserve higher multiples because they’re a rare species amid an economic slowdown, and a dovish Federal Reserve tends to hurt financial shares, the biggest industry in the value cohort.

“When economic growth has been scarce, investors have flocked to stocks that do not need the economy to grow to generate top-line and bottom line growth. Almost by definition, those are growth stocks,” Clissold wrote in a note Tuesday. “As long as economic growth remains sluggish, the growth premium should remain intact.”

Clissold’s view is at odds with a growing list of strategists who say now is time to favor value stocks. Earlier this month, both Sanford C. Bernstein and Northern Trust Corp. predicted a rebound in cheaper shares after the group’s valuation fell to record relative to growth stocks and the more expensive area of the market.

After beating growth for the first time in two years in the fourth quarter, value stocks have dropped back again in 2019, rising about 10 percent versus their counterparts’ almost 13 percent rally, indexes compiled by Russell show. Growth has beaten value since 2006, an unprecedented stretch over the last nine decades, according to Ned Davis Research.

“The problem for value is that the conditions that have favored growth -– sluggish economic growth, a friendly Fed, and a secular bull for the broad stock market -– remain in place,” Clissold said. “The secular environment means that countertrend rallies in value should be shorter and shallower.”

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Richard Richtmyer, Dave Liedtka

©2019 Bloomberg L.P.