Muni-Bond Slide Leaves Test: Will Key Buyers Flee in Droves?

Muni-Bond Slide Leaves Big Test: Will Key Buyers Flee in Droves?

(Bloomberg) -- Municipal bonds suffered their worst week since early February, but the real test of the market lies ahead: Will slow-to-react individual investors pull their money out in droves, as they have during previous downturns?

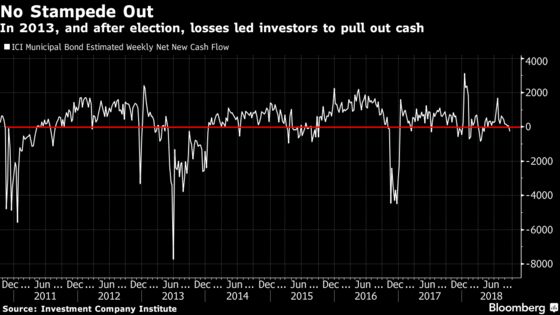

Individuals, who own more than half of all state and local governments bonds directly or through mutual funds and don’t follow the minute-by-minute movement of interest rates, haven’t hit the sell button yet. They pulled just $44 million from municipal debt funds in the week ended Wednesday, according to Lipper U.S. Fund Flows data, even after the securities posted their worst monthly return since January.

Prices have slipped steadily since Wednesday and continued to edge down Friday, when the U.S. Labor Department reported that the unemployment rate hit a nearly half-century low. That pushed benchmark 30-year yields up 0.14 percentage point this week to 3.4 percent, a more than three-year high.

“Rates have moved but there hasn’t been a material sell-off," said Nicholos Venditti, a municipal-bond portfolio manager with Thornburg Investment Management in Santa Fe, New Mexico. “Until you see more dramatic outflows, either because people are afraid of rates or because they want to get out of munis and go buy Amazon.com stock, that test isn’t going to take place."

Even though state and local government debt is one of the world’s safest investments, buyers are still prone to so-called headline risk, or bad news stories that undermine its perception as a haven and cause investors to sell when they should stay put.

That happened in 2010, when banking analyst Meredith Whitney triggered a sell-off by predicting that recession-battered governments would default on "hundreds of billions of dollars" of bonds. That forecast proved widely off the mark, and in 2011 municipals returned 11 percent.

Since municipal bonds don’t trade heavily, spikes in inflows or outflows can have a larger impact on prices than in other markets.

The pace of selling may quicken when investors start opening their statements and see losses, or if the pace of new debt sales picks up, Venditti said. Fixed-rate municipal-bond issuance has declined 12 percent compared to last year, adding ballast to the market. But the pace may quicken in the closing months of the year.

“Bankers want to do their deals before year-end, especially when it’s in conjunction with a rising rate environment," said Robert DiMella, executive managing director and co-head of MacKay Municipal Managers.

Tax loss selling could bring further pressure, he said. With the S&P 500 Index up more than 7 percent this year, bondholders may sell to offset gains in stocks to cut next year’s tax bills. But DiMella said a downturn could be a good thing: He and other professional investors may have a chance to pick up bonds on the cheap.

To contact the reporter on this story: Martin Z. Braun in New York at mbraun6@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, William Selway, Michael B. Marois

©2018 Bloomberg L.P.