An 18-Month Chatfest Reveals Limits (and Scope) of Indexer Power

An 18-Month Chatfest Reveals Limits (and Scope) of Indexer Power

(Bloomberg) -- One of the most asked questions as passive investing grows is whether index makers have become too powerful. Based on MSCI Inc.’s failed 18-month quest for benchmark reform, it seems not.

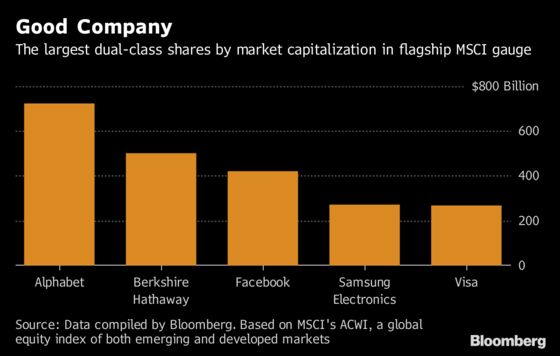

MSCI said on Tuesday that it was scrapping plans to reflect voting power in its benchmarks, following opposition from some investors. The U-turn ends more than a year of agonizing over whether the indexer for almost $14 trillion should police companies that have different classes of shares with unequal voting rights, a structure made popular by the likes of Google parent Alphabet Inc.

But wider questions about the companies behind index funds have only just started to be raised.

With the growth of passive investments like exchange-traded funds, these benchmark giants have gained substantial size and prominence. MSCI and its peers can send cash flooding into a company or country by adding it to a high-profile measure -- or out again, if they remove it. MSCI benchmarks were used by ETFs holding $763 billion as of July 31, the company said in August. Companies, investors and policy makers are still grappling with what this means.

Snap Decision

“We’re disappointed, particularly in light of the weak regulation by stock exchanges at this point,” Ken Bertsch, executive director of the Council of Institutional Investors, said of MSCI’s decision to stand pat. Still, “there’s some valid criticism that they’re not really very good in a quasi-regulatory role.”

The CII, which is based in Washington and lobbies for better corporate governance on behalf of more than 120 pension funds and endowments, is now asking exchanges to step up, Bertsch said.

The latest controversy exploded in March 2017, when Snap Inc. listed shares with no voting rights. A plethora of startups had used multiple share classes to go public without ceding their founders’ control, but Snap proved to be the last straw.

S&P Global Inc. last year barred companies with multiple share classes from joining its indexes, including the S&P 500. FTSE Russell, a unit of London Stock Exchange Group Plc, said public shareholders must control at least 5 percent of a firm’s voting rights to be eligible for its gauges.

Both, however, shied away from hurting companies already in their indexes -- or the funds that follow them. S&P only tweaked a handful of benchmarks and made an exception for companies already in them. FTSE, meanwhile, gave existing constituents until 2022 to get their houses in order.

Money Talks

Why the flexibility? In a word, money.

Indexing is big business. Benchmark providers rely on asset-based fees from ETFs and mutual funds that track their measures. And some of their largest clients weren’t keen on change. BlackRock Inc., the world’s biggest money manager, argued in an open letter to MSCI earlier this year that broad indexes should be as expansive as possible, despite favoring one vote per share itself.

The proposed reforms would require funds to rebalance and “be costly for investors in index products,” Barbara Novick, BlackRock’s vice chairman, wrote in May. “Policy makers, not index providers, should set corporate governance standards.”

Indexers are already under scrutiny from those policy makers -- both in Europe, where the Libor fixing scandal yielded new rules this January, and in the U.S., where the Securities and Exchange Commission is considering whether these companies can continue to avoid registering as investment advisers like fund issuers.

New Gauges

Index providers are increasingly working with asset managers to structure custom gauges that command higher fees and blur the lines between indexer and adviser. MSCI, for example, attributed some of its earnings last quarter to “strong growth in factor and ESG indexes and custom and specialized index products.” ESG refers to environmental, social and governance concerns.

In a concession to critics, MSCI will start new benchmarks in the first quarter of 2019 that penalize companies with unequal voting rights, drawing from its aborted proposal. That plan would have affected roughly 10 percent of companies in its flagship all-country, world gauge known as ACWI, ejecting 12 stocks and decreasing the weightings of another 204, it said in June. Alphabet and Facebook Inc. were among those facing the largest cuts.

Companies with multiple share classes will now stay in MSCI’s flagship benchmarks. And companies like Snap -- which had been excluded -- can join from March 1.

“We wanted to keep the foundation and then offer the option to investors,” Remy Briand, chairman of the MSCI Index Policy Committee, said in an interview on Tuesday. “For quite a lot of investors, actually, the problem should be dealt with by either regulator or stock exchange.”

To contact the reporter on this story: Rachel Evans in New York at revans43@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Eric J. Weiner, Andrew Dunn

©2018 Bloomberg L.P.