Whatever Is Bugging Bonds, Stock Investors Have Gotten Over It

Whatever Is Bugging Bonds, Stock Investors Have Gotten Over It

(Bloomberg) -- A lot of optimism was baked into equities headed into Wednesday’s Federal Reserve meeting. Turns out, not enough.

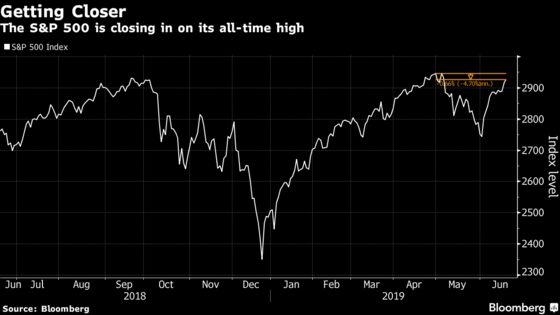

Whatever the reason for all the anxiety gripping bonds -- vanishing inflation, a trade war, the economy -- the stock market has rapidly gotten over it, with the promise of more stimulus leaving bulls in control. Fueled by a friendly Fed, the S&P 500 is poised to open at an all-time high and some strategists see it rising another 10%.

Pushed up as consensus built that the sight of plummeting bond yields will force Jerome Powell to cut rates, the S&P 500 jumped within 20 points of its all-time high Wednesday and futures suggest it will test that record. The Fed indicated a readiness to lower interest rates for the first time in more than a decade, citing “uncertainties” in the outlook that have boosted the case for easing.

“What more could the equity market want?” said Michael Kushma, chief investment officer for global fixed income at Morgan Stanley Investment Management. “What more could the Fed do besides, ‘We are going to take action down the road, most likely, to keep the expansion going.”’

Futures for the S&P 500 jumped 0.8% as of 5:17 a.m. New York-time on Thursday, having closed the previous session within striking distance of its April high of 2,945.83. The Dow Jones Industrial Average sits just 324 points from its October record. The yield on the benchmark 10-year note dipped below 2% for the first time since November 2016.

Investors are pricing in more than two quarter-percentage-point cuts this year, with bond traders nearly certain at least one will come as soon as July.

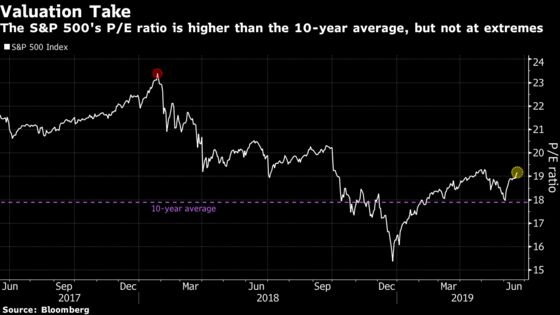

If nothing else, falling borrowing costs make stretched valuations in equities more palatable. The S&P 500’s P/E ratio currently sits at 19 based on trailing earnings -- high by historical standards, but possibly reasonable when compared with fixed-income yields. When stocks plunged at the start of February 2018, for instance, the P/E ratio was hovering above 23 and the 10-year yield topped 2.7%.

“It seems to me that the statement by the Fed does help justify the valuations we’re seeing in the equity market,” Calvin Norris, U.S. rates strategist at Aegon Asset Management, said in a phone interview. “The equity market doesn’t have to worry as much about the Fed acting too slow or not reacting at all to those developments. If anything, it should be somewhat reassuring.”

Stocks are now completely over the trauma inflicted last month by the threat of U.S. tariffs on Mexican goods. The prospect of stimulus has allowed them to brush off worries about the economy. The same cannot be said of Treasuries, where a relentless retreat in yields suggests a greater preoccupation with President Donald Trump’s trade war and the possibility a recession is brewing.

“In some sense the Fed is on the bond market’s side,” said Bruce McCain, chief investment strategist at Key Private Bank. “The stock market is giving you a very positive, optimistic assessment, which is more in line with the president who thinks the economy is in good shape, it just needs more gas. He would be closer to that perspective.”

Through one lens, even Treasuries can be framed as relatively sanguine about what awaits the U.S. economy. While the three-month yield remains well above the 10-year yield, that longer-dated debt still pays out a higher rate than two-year Treasuries. Put together, this cross-asset picture suggests both bonds and stocks see proactive easing as likely sufficient to keep both the longest economic expansion and bull market run in American history intact.

In fact, equities might not be pricing in all the good news the bond market has to offer. According to Gina Martin Adams, Bloomberg Intelligence chief equity strategist, the multiple for the S&P 500 Index should be around 20 if three rate-cuts are coming in the next year. That would put the benchmark stock gauge close to 3,200.

To Mark Heppenstall, chief investment officer of Penn Mutual Asset Management, the two markets have been conveying the same message all along.

“Where we stand in interest rates today, where we stand in persistent low inflation today means that whatever investors are willing to pay for earnings should be higher based on the fact that interest rates are lower,” he said.

--With assistance from Sarah Ponczek and Elena Popina.

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Luke Kawa in New York at lkawa@bloomberg.net

To contact the editor responsible for this story: Jeremy Herron at jherron8@bloomberg.net

©2019 Bloomberg L.P.