Morgan Stanley Says Rest of 2019 Might Flummox U.S. Markets

The Goldilocks conditions is finally coming to an end.

(Bloomberg) -- The beginning of 2019 has been good for U.S. assets. But the back half might not be as favorable, according to Morgan Stanley.

Markets are currently priced for a “Goldilocks” scenario of solid but non-inflationary growth, and America has outperformed -- but that’s all set to reverse, strategists including Andrew Sheets wrote in a May 12 note. Their skepticism rests on three factors playing out over the remainder of the year:

- The Goldilocks conditions finally coming to an end

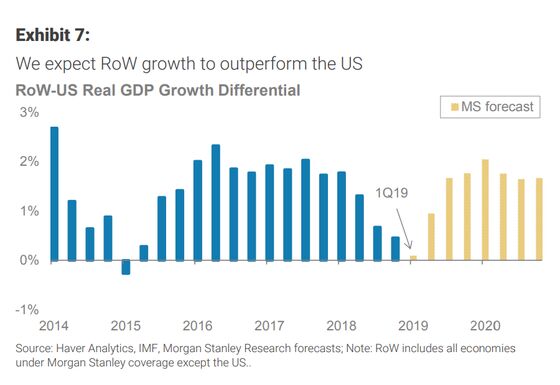

- The divergence between growth in the U.S. and the rest of the world narrowing

- The gap between prices and fundamentals closing

“Investors should hold a defensive tilt and a preference for ex-U.S. risk exposure,” the strategists wrote. “This is supported by where valuations sit versus fundamentals, forecasts that U.S. versus rest-of-world growth reverses and excessive investor confidence that there is little risk of the output gap closing.”

U.S. equities have outperformed so far this year, with the S&P 500 gaining 15% versus the 12% rally in the MSCI All-Country World Index. The 10-year Treasury yield has fallen about 25 basis points and the Bloomberg Dollar Spot Index is up 0.4% even after the dovish pivot by the Federal Reserve.

This backdrop ought to have spurred caution. Yet, “the predominant concern until two weeks ago appeared to revolve around whether markets could go up a lot more,” the strategists wrote, noting that the last week’s escalation in trade tensions have moderated some of the optimism.

Concerns about the narrowing of the output gap -- the difference between the capacity of the economy and its actual output -- relate to some measures of inflation not showing moderation even as markets appear to be pricing in a benign scenario, Morgan Stanley said.

December Clues

If the gap between the U.S. and the rest of the world sounds like a familiar idea, that’s because it is -- Morgan Stanley outlined it in November. Though the prediction has been challenged in 2019, the strategists still maintain that there will be a reversal of America’s outperformance.

“The growth reversal story has been delayed, not derailed,” the strategists said.

In December, when expectations of U.S. versus RoW growth appeared to be reversing, the dollar weakened, stocks outside America outperformed and duration in the U.S. beat Europe, they wrote. “Over the next 12 months, we expect all those performance trends to apply.”

In addition to the challenge from the idea that the rest of the world would outperform, Morgan Stanley has seen its dollar view struggle as well. Late last year, the firm said the greenback was 10%-15% overvalued. But even with the Fed’s dovish pivot and some softening in America, struggles in economies outside the U.S. and continued dovishness from the likes of the European Central Bank and Bank of Japan have kept the dollar buoyant.

On the other hand, the U.S. equity view has done well. Strategist Mike Wilson, whose call nailed the market in 2018, said in the U.S. stocks midyear outlook note that the escalation of trade tensions had increased potential for an economic recession.

“While last week’s correction helped move the risk-reward closer to balanced, we think there is likely more downside than upside” based on a “high-conviction view” that earnings estimates are 5%-10% too high, Wilson wrote in the note.

The investment ideas the strategists led by Sheets propose include:

- Stocks and government bonds over credit

- International equities versus U.S., with Japan a favorite

- U.S. Treasuries over Bunds

“The question remains: is the performance pattern year-to-date a template for the rest of the year, or an aberration?” the strategists said. “We think the latter.”

--With assistance from Rita Nazareth.

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Ravil Shirodkar, Derek Wallbank

©2019 Bloomberg L.P.