Morgan Stanley Quants See Gains In Rolling China Stock Futures

Morgan Stanley Quants See Gains In Rolling China Stock Futures

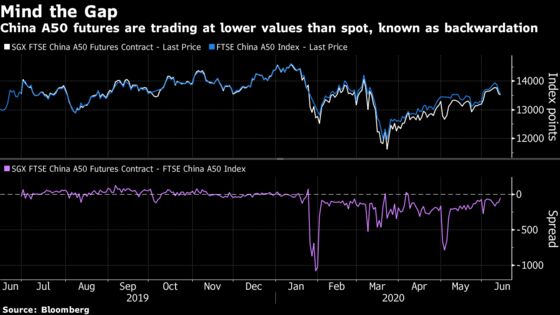

(Bloomberg) -- An unusual bout of backwardation in Chinese equity futures has created an opportunity for traders and suggests sentiment among investors is overly bearish, according to quantitative strategists at Morgan Stanley.

The presence of the phenomenon -- where futures trade at lower values than spot prices -- in contracts tracking the FTSE China A50 Index means they should outperform exchange-traded funds tracking the same gauge if contracts are rolled upon expiry, strategists including Yinan Zhang wrote in a research note Thursday.

The strategy involves closing initial contracts as they expire each month and entering into new, identical positions that are due at a later date - with a trader generating a profit from the convergence of the lower futures price with the more valuable underlying index.

“Our quant analysis suggests that holding and rolling index futures will significantly outperform the index, and that the backwardation level indicates contrarian sentiment,” they wrote.

Singapore-listed contracts tracking the FTSE China A50 index are a popular way for fund managers outside of China to trade, or hedge exposure, to onshore stocks. The underlying gauge is down 5.2% year-to-date, after a 14% rally since the March low.

The appearance of backwardation in the contracts has resulted from a lack of alternative methods for foreigners to short-sell onshore, and also reflects rising demand for hedges among so called market-neutral funds, the Morgan Stanley strategists said.

“The backwardation levels of index futures also act as a contrarian market-sentiment indicator, and have been suggesting an overly bearish sentiment for the CSI 300 index since March 20,” they added.

©2020 Bloomberg L.P.