Morgan Stanley Likes Credit, U.S. Stocks in Broad Risk-On View

Morgan Stanley Likes Credit, U.S. Stocks in Broad Risk-On View

(Bloomberg) -- The cycle in financial markets in the wake of the Covid-19 shock should be more “normal” than expected in the second half of the year, with gains likely in credit and value stocks, according to Morgan Stanley.

Markets are underpricing the extent to which things could follow a fairly typical playbook of emergence from a recession, strategists led by Andrew Sheets wrote in a note dated June 14. They added that they’ll be watching the risks from trade tensions, politics and the coronavirus for any signs the recovery could be derailed.

“While outright gains look modest, fundamentals, valuations and technicals all support more rotation toward traditional early-cycle beneficiaries,” the strategists said. “The economic recovery will look more ‘normal’ than abnormal.”

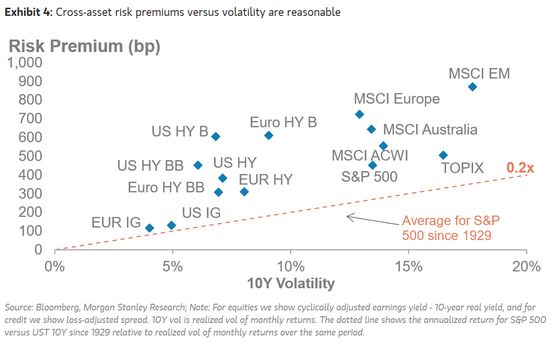

The best reward for the risk involved is in owning credit and selling volatility, they said, while also recommending a reduction in government-bond positioning to underweight.

The trough and recovery of the economy this year have been similar to those of past recessions, including the bottoming in markets ahead of the data, and the fact that equity volatility and credit spreads peaked before stock markets hit bottom, they said.

“Global economic data are weak but set to improve,” they said. “We think that markets care more about the trend in data than the level. As such, while it may sound counter-intuitive, we think that ‘fundamentals’ are currently supportive for risk-taking.”

Morgan Stanley’s strategy for the second half includes:

- Favor U.S. and European stocks over emerging markets; while EM stocks would be a “normal” early-cycle trade, the strategists don’t see it working well this time

- Favor U.S. small-cap equities, cyclicals and European value shares

- Treasury yields are expected to rise, with the 10-year seen just above 1% by year-end

- The dollar should weaken as global growth rebounds and Federal Reserve easing outpaces that elsewhere. The euro will gain thanks in part to a new recovery fund

- In corporate credit, investors are being paid well to move down modestly in quality

- Copper should do well based on a strong China recovery, while the strategists are more cautious on oil and aluminum

©2020 Bloomberg L.P.