Morgan Stanley: Here's S&P 500 Impact of Fed Balance Sheet Cuts

Morgan Stanley: Here's S&P 500 Impact of Fed Balance Sheet Cuts

(Bloomberg) -- With the stock market fixated on the Federal Reserve’s balance sheet, Morgan Stanley analysts built a quantitative model to assess the impact. And they found the extent of the influence is great.

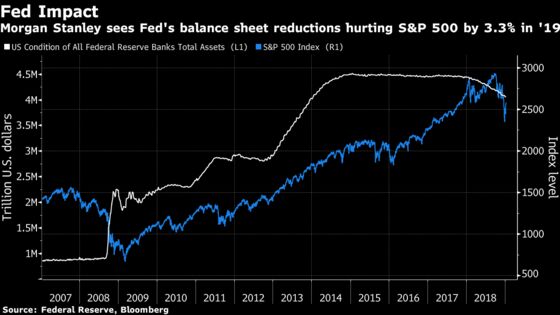

The S&P 500 has shown a positive relationship to central bank action on mortgage backed securities since 2009, with every $20 billion shift in bond holdings equaling a 0.37 percent change in stock prices, strategists led by Brian Hayes found. Should the Fed continue to its pace of $15 billion in reductions a month in 2019, the gauge would drop 3.3 percent, the model shows. That’s roughly a third of its annualized return in the past five years.

Fed Chair Jerome Powell has indicated the intention to remove stimulus put into place following global financial crisis a decade ago, at times triggering losses in stocks. The S&P 500 briefly pared gains Thursday after he said at the Economic Club of Washington that the balance sheet will be “substantially smaller” than it is now, though bigger than it was before the crisis.

“Continued Fed balance sheet reductions are expected to be a modest drag on equities in 2019,” Hayes wrote in a note to clients, adding his model assumes the program will last through December even the firm’s economists expect the central bank to halt its balance sheet normalization in September.

The Fed began in 2008 expanding its balance sheet through purchasing Treasuries and MBS as a means to keep interest rates low to spur economic growth. As the economy found its footing, the stimulus was withdrawn starting in 2017.

The reversal threatens financial markets as it removes a stable source of demand, according to Joseph LaVorgna, chief economist for the Americas at Natixis. Combined with a rise in Treasury issuance, investors may have to make room for the supply by selling other assets, he said.

“Massive Treasury issuance and waning Fed demand for long duration securities raises the possibility of a crowding out of risky assets,” LaVorgna wrote in a note this week. “Put another way, investors will need to buy an ever rising share of Treasuries while the largest incremental buyer (the Fed) is stepping away from the fixed income market.”

How much will it hurt equities? By overlaying the bond purchases with stock performance, Morgan Stanley found that the S&P 500 has shown a significant correlation to changes in MBS holdings but little to those seen in Treasuries.

The equity market’s response mechanism has to do with an investment process known as portfolio rebalancing, where an asset becoming less risky through Fed repurchases would prompt investors to move money to other assets to maintain a desired level of risk, according to Hayes. Because the trajectory of MBS holdings is more difficult to estimate than that of Treasuries, the asset therefore garners more attention from investors, he said.

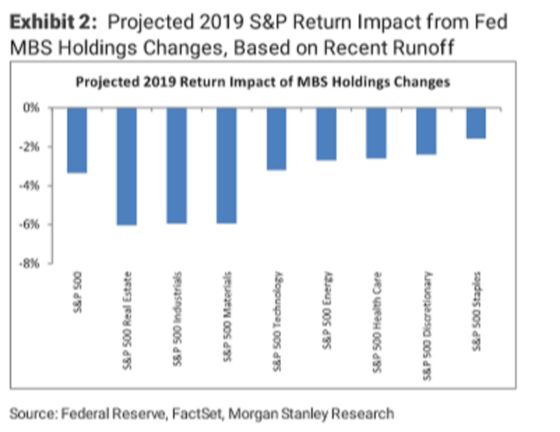

Cyclical stocks, such as automakers, materials producers and transports, are among industries showing the highest sensitivity to changes in the Fed’s balance sheet, Morgan Stanley study found. The current MBS runoff could translate to a 6 percent decline for these stocks this year, their estimates showed.

--With assistance from Christopher Anstey.

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Chris Nagi, Jeremy Herron

©2019 Bloomberg L.P.