Morgan Stanley, BNP Brace for the Return of Currency Swings

Morgan Stanley, BNP Paribas See Return of Big Currency Swings

(Bloomberg) -- As waves of volatility lash bond and stock markets, currencies are an island of relative calm. Wall Street says that’s about to change as rifts open between central banks the world over.

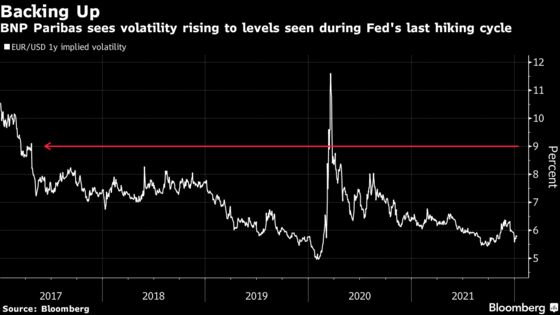

At Morgan Stanley and BNP Paribas SA, strategists are predicting greater price swings as policy makers scale back on stimulus at different rates, opening fault lines under usually stable Group-of-10 currencies. BNP’s Oliver Brennan is predicting one-year implied volatility between the euro and the dollar will advance to around 9%, a level last seen at the height of the pandemic -- and before that, back in 2017, when the Federal Reserve’s previous hiking cycle was in full swing.

It’s a sea change for traders accustomed to near-united monetary largesse that’s kept borrowing costs low -- and markets boring. Yet for many, disparities including those between the newly hawkish Fed and more dovish peers such as the European Central Bank are an unmistakable signal that it’s time to abandon short-volatility bets and switch to strategies that profit from dramatic ups and downs.

“We are in this inflection point and if you don’t start reducing your short vol exposure, it’s very likely you’re going to end up erasing your gains,” said Andres Jaime, a strategist at Morgan Stanley, who entered the currency market in 2006. While he’s seen central-bank policy divergence before, what would be unique this time is the “potential pace of tightening of the Fed,” he said.

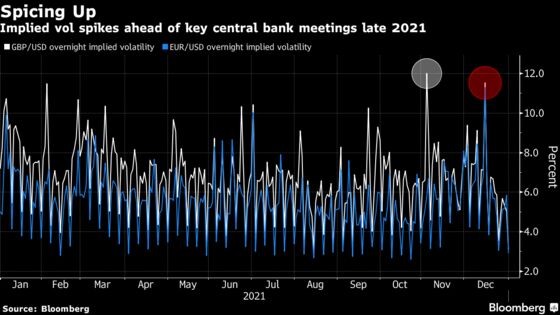

A dollar selloff on Wednesday helped push volatility higher in some pairs, including the yen and the Canadian dollar, and brought the greenback down to its lowest level in two months. With the holiday season over, news events like U.S. inflation data has traders returning to the market, as euro futures volume reached its highest level since the outbreak of the omicron variant in November.

Morgan Stanley’s Jaime sees global FX volatility readings rising to around 10.5 during 2022 -- that compares to about 7.1 on JPMorgan’s Global FX Volatility gauge currently. The bank expects higher volatility in high beta currencies in particular, such as the New Zealand kiwi, which should bear the brunt of price swings as a shift in monetary policy gets underway, he said.

The Fed caught markets off guard when the minutes to its latest meeting showed officials’ increasing preference for quicker rate hikes to help tame inflation running at fastest pace in four decades. Traders are now pricing in more than three 25-basis-point hikes this year, compared with just one 10 basis-point increase by the ECB, which has close to ruled out any hikes until at least 2023.

Central banks in Norway, New Zealand and the U.K. meanwhile have already started raising rates, while Canada is hot on their tails. That’s in contrast to the Bank of Japan and the Swiss National Bank where hiking rates will likely be pushed beyond this year.

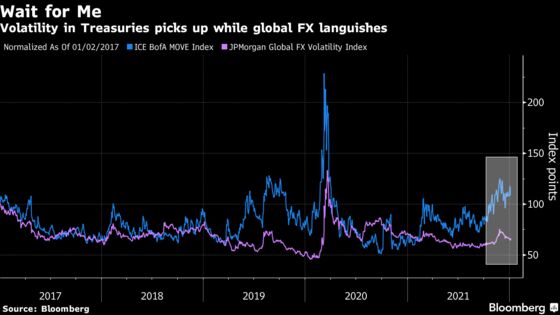

So far, the bond market has felt most of the heat, with a gauge of volatility in U.S. Treasuries hovering close to levels last seen in March 2020. In contrast, the JPMorgan Global FX Volatility index has slipped back to around its average for 2021.

Bank of America analysts expect currency volatility to pick up though, citing historical analogs from 2008, 2011, and 2018, when it trailed the rise in inflation by about three months.

They recommend positioning for higher volatility in the euro and Canadian dollar pair, given the interest-rate path for the economies is diverging and the outlook for the energy market -- a key driver for the loonie -- remains uncertain.

For Unigestion SA portfolio manager Jeremy Gatto, pairs including Britain’s pound and Norway’s krone might offer enticing volatility plays given their sometimes unpredictable central banks. The Bank of England surprised markets with a rate increase in December despite headwinds from omicron.

“Before Covid-19 you could be a generalist, it was pretty much every central bank on the same page,” said Gatto, 38, who started in the industry in 2007. “Now you can’t just say I’m going to be long the dollar, or long or short vol. You’re going to have to pick which cross you’re going to apply that logic to.”

Liquidity Concerns

Political machinations are also feeding into the mix. Eimear Daly, an FX strategist at Barclays, is betting on increased volatility in the euro-dollar pair, stemming from French and Italian elections.

Traders are especially wary of a sudden increase in volatility given financial conditions are becoming less forgiving. Since the financial crisis in 2008, one-year implied volatility in the euro-dollar cross has collapsed from over 20% to 5.7% on Wednesday, weighed down by bond buying programs and record-low interest rates.

“People who have come into the business in recent years have lived in a world of low rates and massive liquidity provision that has been insurance against volatility spikes,” said Michael Melvin, executive director at the Rady School of Management, University of California San Diego and former multi-asset strategist at BlackRock, who has been studying and working in the currency market for 40 years.

READ MORE: ECB Optionality May Leave Volatility Decaying to a Higher Floor

Not everyone is ready to abandon short-volatility strategies that netted gains of 15.4% across assets in 2021, their best year since 2009, according to provisional Eurekahedge data compiled by Bloomberg.

“The sweet spot for us is a little bit of elevated volatility and markets trading sideways,” said Tom Pansegrau, 35, who focuses on short-volatility strategies at 7orca Asset Management. He doesn’t foresee “any major surprises” because the Fed has been “straightforward with its path on raising interest rates,” he said.

But the response to the ins and outs of the Federal Open Market Committee’s debate about policy tightening showed how even well-telegraphed moves can surprise markets. The Nasdaq 100 Stock Index, which includes interest-rate-sensitive technology shares, fell as much as 7.1% in the first six trading days of the year.

“There’s complacency around how much central banks are willing to do to stop inflation -- there’s a belief that the Fed is not going to be able to hike rates a lot,” said Morgan Stanley’s Jaime. “For me that’s a risk and that’s where I see most of the pain coming from.”

©2022 Bloomberg L.P.