Market Strategists See Light at the End of the Tunnel on Brexit

Market Strategists See Light at the End of the Tunnel on Brexit

(Bloomberg) -- U.K. domestic stocks and the pound slipped after Parliament rejected Boris Johnson’s timetable for taking the country out of the European Union by Oct. 31, raising the prospect of an election.

Still, the House of Commons voted in favor of Johnson’s agreement in principle, the first time lawmakers have backed a departure plan, which makes a no-deal separation less likely. Johnson, who’s promised not to delay Brexit, now must decide whether to call a snap election should the EU agree to extend the U.K.’s departure to Jan. 31.

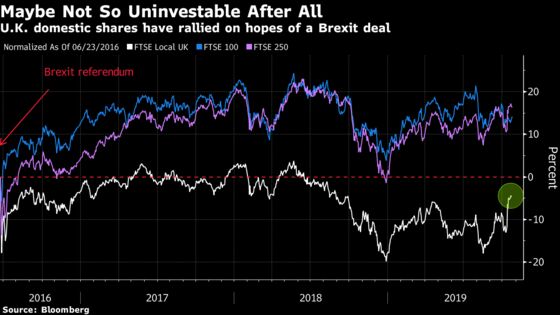

The U.K.’s domestically-focused FTSE 250 was little changed, though Brexit-sensitive stocks including banks and housebuilders declined. The gauge, along with the pound, has rallied in the past two weeks amid optimism about a Brexit deal. The U.K.’s FTSE 100 outperformed Europe’s Stoxx 600 Index, gaining 0.4%, as exporters benefited from the pound’s drop.

Here’s what market participants are saying about the latest developments.

Chris Bailey, Raymond James

- Market moves today and yesterday evening “should be put into the context of the sharpness of last week’s rotation towards FTSE-250/U.K. value names.”

- “Strategically, I think that the game remains the same: an ultimate deal, but quite possibly via an extension and an election.”

- “We still like the rotation trade in favor of U.K. domestic assets including the pound.”

Jim Wood-Smith, Hawksmoor Investment Management

- “There’s more hurdles to go before we can be 100% sure of the final exit arrangement, but yesterday was an important step forwards. We are more confident that the Brexit rally in sterling and domestic stocks has further legs.”

- “For the first time, no deal is genuinely looking less likely. The 30 majority in favor of the second reading is a huge sign that parliament is prepared to pass the Withdrawal Act.”

Ipek Ozkardeskaya, London Capital Group

- “Brexit will likely be delayed, again. But this time, investors can see the light at the end of the tunnel. The only question is how Boris Johnson will spend the next three months.”

- “Snap election talks could dampen investor sentiment and a correction could pull the pound below $1.2820.”

- “Expectations of an orderly Brexit could encourage some investors to purchase promising FTSE stocks before the pound appreciates further.”

Sylvain Goyon, Oddo-BHF

- “Bottom line: For the first time in almost 3 1/2 years, the market is seeing light at the end of the tunnel. The precise date is not known yet, but general principles can be worked on.”

- “I would expect a positive trend on U.K. domestic assets, higher yields on the gilt by anticipation of future budgetary largess and a stabilization in the pound.” A stable currency bodes well for European markets as a stronger pound is correlated with positive development for continental stocks, though that may already be reflected in prices.

Alasdair McKinnon, Scottish Investment Trust

- “In big-picture terms, losing the fast-track vote should not overly concern investors. The greatest worry, until recently, had been the prospect of a no-deal Brexit. If anything, the night’s events suggest that a deal will eventually be agreed.”

David Page, AXA Investment Managers

- “Sterling was reasonably nonplussed with modest declines against the U.S. dollar and euro. Forex –- and wider markets –- remain confident that the prospect of no-deal Brexit has fundamentally shifted following Johnson’s negotiated deal.”

Marcus Morris-Eyton, Allianz Global Investors

- Failure to approve the fast-track legislation “creates yet another period of protracted uncertainty for U.K. investors.”

- Both consumer and corporate confidence is waning, as demonstrated by the quantity of U.K.-related profit warnings in third-quarter results so far.

- Tuesday’s result “ensures the extreme underweight positioning of global investors to the U.K. is unlikely to narrow in the short term.”

Alastair George, Edison

- “PM Johnson made no mention of an election after the vote and eyes will now turn to the EU, which has to approve any extension to Article 50. We expect U.K. equities and sterling to be only modestly lower, on the basis that a short extension will be forthcoming in coming days. Should the EU refuse to extend Article 50 however, both the risk of a no-deal Brexit and a sell-off in U.K. equities would increase significantly.”

David Holohan, Mediolanum

- “The vote result places control of the next steps back with the EU, as investor attention will now focus on securing an extension. If, as is widely anticipated, an extension is provided, it is unlikely that sterling will weaken significantly, thus limiting the downside in FTSE 250 and European equities while FTSE 100 stocks should advance on weaker sterling.”

Ulrich Urbahn, Berenberg

- “This will definitely lift sentiment towards Europe and particularly the U.K., with U.K. domestic stocks and GBP being the main beneficiaries. However, macro data have to improve and the trade war has to be contained for a sustained risk rally as a Brexit deal has been already priced somewhat by the markets.” Caveat is that the U.K.’s exit is delayed.

Stephane Barbier de la Serre, Makor Capital

- “All the above developments bolster our recent conviction that, notwithstanding any elusive ‘value’ considerations, being long U.K. assets at this stage is synthetically equivalent to being long uncertainty. Therefore, keep selling bounces on GBP (towards 1.27 at least, possibly 1.269) and FTSE 250 (toward 19,750). Impact on Footsie 100 to be more blurred as is now usually the case.”

--With assistance from Joe Easton, Michael Msika and Jan-Patrick Barnert.

To contact the reporters on this story: Kit Rees in London at krees1@bloomberg.net;Ksenia Galouchko in London at kgalouchko1@bloomberg.net;Sam Unsted in London at sunsted@bloomberg.net

To contact the editors responsible for this story: Celeste Perri at cperri@bloomberg.net, Phil Serafino, Beth Mellor

©2019 Bloomberg L.P.