Money Managers Are Seeking Shelter in the Riskiest Parts of CLOs

Money Managers Are Seeking Shelter in the Riskiest Parts of CLOs

(Bloomberg) -- Credit investors believe they have a sure-fire way to profit even if the economy slows. But their returns could be lower than they expect if a corporate downturn lasts longer than it did a decade ago.

The money managers are buying the riskiest portions of bundles of loans known as collateralized loan obligations. Their thinking is that when corporate debt markets start to sour, CLOs will be able to buy loans on the cheap, which can boost their returns on the other side of any slowdown.

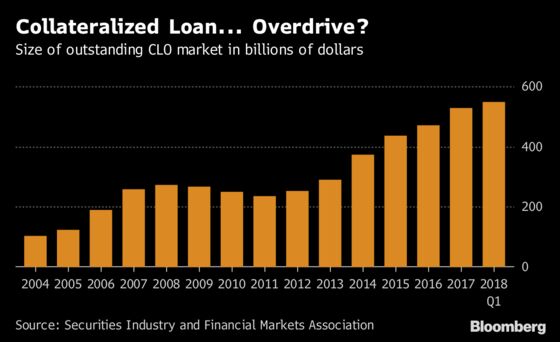

Their wagers have helped fuel a boom in the securities. The volume of outstanding CLOs mushroomed to more than $540 billion this year, up around 80 percent from the start of 2014. The riskiest parts, known as CLO equity, account for about a tenth of the total.

Buying CLO equity played out well during the last crisis. Annual returns for the instruments dipped to 7 percent in 2009, then rose back to 15.3 percent in 2010, according to JPMorgan Chase & Co. data that looked at cash flow returns for older types of the securities known as CLO 1.0, which were issued before 2008.

“Many CLOs issued at the tail end of the last credit cycle proved to be some of the better performers of that era,” said Tom Majewski, managing partner of Eagle Point Credit Management, which had $2.2 billion in assets as of June 30. “The 2018 equity securities could be one of the best performers long term.”

But there are real risks to this investment, cautioned some investors. The last credit crunch hit consumers hardest, while companies recovered fast: The default rate for leveraged loans spiked to more than 12 percent for the twelve months ended November 2009, and was down to 3.49 percent by November 2010.

Read the credit brief: Investors Revive Financing Tool Killed in Crisis

This time around, money managers including Pacific Investment Management Co. and BlackRock Inc. reckon that companies, not consumers, will take the major blow. Default rates may not be high, but could pick up gradually and stay elevated for longer, said Vishwanath Tirupattur, head of fixed income research North America at Morgan Stanley. That’s what happened around the turn of the millennium, when the tech bubble, a recession, and massive corporate frauds like WorldCom resulted in a protracted credit crunch: default rates started rising in 1999, rose above 5 percent in early 2000, and stayed above that level until late 2003.

In this cycle, companies are taking on more debt relative to their assets, and are offering weaker loan safeguards to investors, which could translate to higher credit losses than there have been historically. Those kinds of losses can cut into the interest that CLOs pay to equity holders, because when a portfolio of loans backing a CLO isn’t generating enough income for whatever reason, it has to divert cash flow to other investors instead, reducing its payouts.

"The shape of the default cycle may look different this time," said Tirupattur. "If defaults do not come down as they did in the last downturn, returns for the equity holders could be lower."

And even if CLO equity in aggregate performed relatively well during the crisis, many securities suffered: in the last downturn, the proportion of U.S. CLOs that had to divert cash flow from equity investors peaked at around 56 percent, according to Wells Fargo.

Lower Returns

This year, strong demand for leveraged loans has cut into yields, and therefore the returns that the equity portions of CLOs are generating. Cash yields for the securities for the first half of the year fell to 11.35 percent annualized, from 13.6 percent last year and 22.6 percent the year before, according to JPMorgan Chase data for returns on newer versions of the securities known as CLO 2.0.

CLO equity returns may be falling, but the instruments are still performing better than investment-grade corporate bonds, junk bonds, and most other U.S. asset classes now. Investors like Highland Capital Management view the instruments as a way to ride out the downturn that everyone expects -- but whose timing is hard to forecast. The CLO 2.0 versions of the bonds have more safeguards for investors than their older counterparts.

“We like the long volatility trade and CLO managers who are running a conservative portfolio at the onset would be in a great position to take advantage of this volatility in the next downturn," said Neil Desai, managing director and structured products portfolio manager at Highland, which has around $13 billion in assets under management.

The risk comes from forecasting when the downturn comes. After a CLO sells securities to fund itself, it usually has around five years to buy loans and re-invest principal it gets back, after which it starts to wind down. If the credit crunch happens in year four or five, loan losses may be high, and there may not be enough time to benefit from lower prices on new loans. And CLO equity may generate weak returns if the downturn is longer than a year or two.

“Everyone gets hurt together and right now it’s prudent to have minimal BB, BBB, and equity tranche positions," said Ethan Lai, an associate portfolio manager at Leader Capital Corp, which oversees $230 million.

To contact the reporters on this story: Sally Bakewell in New York at sbakewell1@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net;Adam Tempkin in New York at atempkin2@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins

©2018 Bloomberg L.P.