Mind the Signals! Things Are Starting to Get Real: Taking Stock

Mind the Signals! Things Are Starting to Get Real: Taking Stock

(Bloomberg) -- Want the lowdown on European markets? In your inbox before the open, every day. Sign up here.

Trade worries live on after the news that a U.S.-China deal isn’t likely until April at the earliest. Investors weren’t too fazed on Thursday though as the market rallied, and European shares are up 12 percent this year. Still, in these uncertain times, here’s a few things to keep in mind:

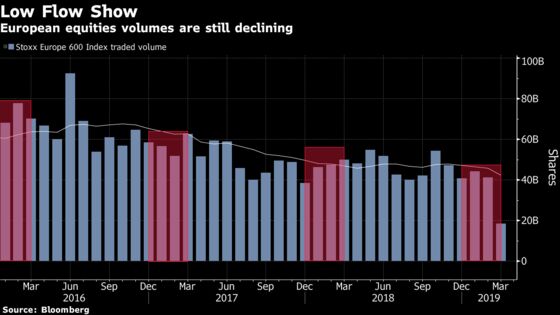

Real money is coming back. Bank of America Merrill Lynch’s positioning note shows that funds reduced cash and increased exposure to stocks in February, with Europe the largest beneficiary ($11.8 billion). But after a lackluster year for volumes in 2018 -- the lowest since 2000 -- there’s no real sign of a related bounce with the rally. Average volume kept falling so there could be scope for stronger positioning, especially since equity flows are still negative, according to the latest EPFR data.

The markets are losing their swing. The Euro Stoxx 50 volatility index (V2X) has reached its lowest level since September, while the S&P’s volatility is beneath Europe’s. A prolonged Brexit saga and delayed trade-talks haven’t triggered any spike. On top of that, the Bull-Bear index is not showing any euphoria, which can also be considered a positive sign.

So, is this sideways consolidation or topping out? Charts are sending a mixed picture to investors. Low trading volume can be the source of erratic moves and cause either bulls or bears to give in easily. Since the Euro Stoxx 50 broke above its 200-day moving average there were multiple times when a “top” was building up, with intraday high and lower close. Yet the uptrend was not broken, and moving averages hint at a bullish picture.

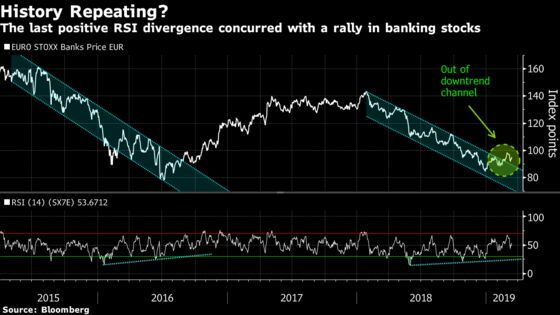

Technically speaking, banks look very interesting. While the latest monetary policy decision was seen as a downer, a low rate environment could be something the market is now used to. The Euro Stoxx Bank Index (SX7E) managed to bounce out of its downtrend, while the Relative Strength Index (RSI) is showing a “positive divergence.”

On this triple witching expiry day, Euro Stoxx 50 futures are little changed ahead of the open.

- Watch technology stocks following reassuring results from Broadcom, which may prop up the chip sub-sector. Watch European chipmakers like Infineon, STMicroelectronics and AMS for read-across from the numbers, plus any impact on chip equipment names like ASML and BE Semiconductor. Separately, software firms Oracle and Adobe disappointed investors, so keep an eye on the likes of SAP, Micro Focus, Dassault Systemes and Nemetschek.

- Watch trade-sensitive stocks after Chinese Premier Li Keqiang wrapped up the National People’s Congress in Beijing by saying the country will stick to its current economic support strategy, resisting the temptation to engage in large-scale stimulus like quantitative easing or a massive expansion in public spending. Chinese stocks rose.

- Watch the pound and U.K. equities after U.K. Parliament voted Thursday to let Prime Minister Theresa May go back to Brussels to request an extension to the divorce from the European Union.

COMMENT:

- “We remain defensive and continue to prefer energy, healthcare and IT over industrials, utilities and communication services,” the Credit Suisse Investment Committee wrote in a report. “We also continue to favor emerging market over euro-zone equities. With IP momentum expected to rebound and central banks having turned more dovish, a potential return of volatility could soon offer an entry opportunity for equities. For now, we continue to prefer option structures to reduce selected equity beta and monetize the current low volatility.”

COMPANY NEWS AND M&A:

- Swedbank Made 4 Notifications a Day to Estonia Police in 2018

- Vista Alegre Atlantis FY Adj. Net Up 54% on External Markets

- UBS Ups Legal Provision to $2.83b, Cuts CEO Bonus After Tax Fine

- VW Sued by SEC for Misleading Bondholders on Diesel Cheating

- Daimler, BMW Eye EU7 Bln Savings Through Tech Collaboration: SZ

- WPP Ex-CEO Sorrell to Receive $2.8 Million Payout After Exit

- Billionaire Bollore Hands Over Reins of Empire to Son Cyrille

- Uralkali FY Revenue 173.61 Bln Rubles Vs. 160.93 Bln Rubles Y/Y

- U-Blox 2018 Sales Miss Lowest Estimate, Sees 2019 Ebit Decline

- Nyrstar Says March 15 Bond Interest Coupon Payment Is Deferred

NOTES FROM THE SELL SIDE:

- Citi cut Wirecard to sell from neutral saying co. is likely to take longer to resolve allegations against it than the market is pricing. Price target cut to 100 euros from 144 euros.

- U.K. consumers are reverting to more cautious spending patterns given the political and economic uncertainties they face and this could weigh on food manufacturers, Berenberg writes in a note downgrading its recommendations on Bakkavor and Greencore.

- Britvic is cut to neutral at Citi because of strong share price moves as well as a lack of obvious catalysts such as for material near-term earnings upgrades, the broker says in a note. Citi sees better risk/reward at Coca‑Cola HBC at the moment.

- RBC says the chance for a quick payout from Cairn Energy’s Indian arbitration case has been delayed and there are now few short-term catalysts to get excited about for the London-listed oil explorer. RBC downgrades Cairn to sector perform from outperform, slashes PT to a tangible net asset value-based 225p from an event-driven 380p previously.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 379.9 (23.6% Fibo); 383 (trend line)

- Support at 369.3 (200-DMA); 365.1 (38.2% Fibo)

- RSI: 69

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,358 (trend line); 3,466 (23.6% Fibo)

- Support at 3,315 (38.2% Fibo); 3,281 (200-DMA)

- RSI: 69.4

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Cerved upgraded to buy at HSBC; Price Target 10 Euros

- Dufry upgraded to buy at Baader Helvea; Price Target 116 Francs

- GEA Group upgraded to overweight at Barclays; PT 28 Euros

- Galenica upgraded to buy at Kepler Cheuvreux; PT 54 Francs

- Raiffeisen raised to equal-weight at Morgan Stanley

DOWNGRADES:

- Bakkafrost downgraded to sell at DNB Markets; PT 400 Kroner

- Bakkavor downgraded to sell at Berenberg

- Britvic downgraded to neutral at Citi

- Cairn Energy downgraded to sector perform at RBC; PT 2.25 Pounds

- Greencore Group downgraded to hold at Berenberg

- Grieg Seafood downgraded to sell at DNB Markets; PT 110 Kroner

- Leroy downgraded to sell at DNB Markets; PT 63 Kroner

- Mowi downgraded to sell at DNB Markets; PT 170 Kroner

- Norway Royal Salmon cut to sell at DNB Markets; PT 170 Kroner

- Salmar downgraded to hold at Berenberg

- Schaeffler cut to hold at Pareto Securities; PT 7.50 Euros

- Scottish Salmon downgraded to sell at DNB Markets; PT 16 Kroner

- Wirecard downgraded to sell at Citi; PT 100 Euros

INITIATIONS:

- B&M European reinstated overweight at Barclays; PT 4.50 Pounds

MARKETS:

- MSCI Asia Pacific down 0.3%, Nikkei 225 up 0.8%

- S&P 500 down 0.1%, Dow little changed, Nasdaq down 0.2%

- Euro up 0.14% at $1.132

- Dollar Index down 0.14% at 96.65

- Yen up 0.04% at 111.66

- Brent up 0.2% at $67.4/bbl, WTI up 0.3% to $58.8/bbl

- LME 3m Copper up 0.5% at $6438/MT

- Gold spot up 0.4% at $1301.6/oz

- US 10Yr yield down 1bps at 2.62%

MAIN MACRO DATA (all times CET):

- 10am: (IT) Jan. Industrial Sales WDA YoY, prior -7.3%

- 10am: (IT) Jan. Industrial Sales MoM, prior -3.5%

- 10am: (IT) Jan. Industrial Orders NSA YoY, prior -5.3%

- 10am: (IT) Jan. Industrial Orders MoM, prior -1.8%

- 10:30am: (IT) Jan. General Government Debt, prior 2.32t

- 11am: (IT) Feb. CPI FOI Index Ex Tobacco, prior 102.2

- 11am: (EC) Feb. CPI Core YoY, est. 1.0%, prior 1.0%

- 11am: (EC) Feb. CPI MoM, est. 0.3%, prior -1.0%

- 11am: (EC) Feb. CPI YoY, est. 1.5%, prior 1.4%

- 11am: (IT) Feb. CPI EU Harmonized YoY, est. 1.2%, prior 1.2%

--With assistance from Joe Easton.

To contact the reporters on this story: Michael Msika in London at mmsika4@bloomberg.net;Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Celeste Perri

©2019 Bloomberg L.P.