Meme Stock Marauders Aside, the Average S&P 500 Bull Is Worried

Meme Stock Marauders Aside, the Average S&P 500 Bull Is Worried

(Bloomberg) -- Back in December, if you asked the typical investor what the next big move would be for the S&P 500, two-thirds would’ve said “up.” After two months of going-nowhere churn in the indexes punctuated by assorted hysterias in crypto and meme shares, barely half would say so now.

For all the kookiness going on adjacent to more stolid stocks, the recent history in American risk markets is one of psychological retrenching. Institutional managers are reining in exposure. People are buying a lot more protection. Even flows to equity funds are slowing.

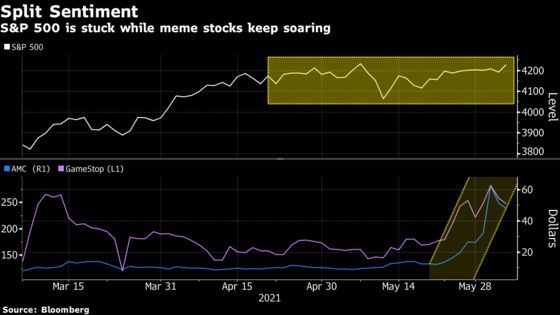

The past week was a microcosm, with flyers like AMC Entertainment Holdings Inc. and GameStop Corp. reprising the crowd-sourced moonshots that first launched in January, while the rest of the market sat still despite a host of catalysts ranging from President Joe Biden’s new tax pitch to weaker-than-expected data on the labor market.

If anything, the gravity-defying rally in meme stocks is arousing angst for anyone who pays attention to business fundamentals. With equities hovering near the highest price-earnings ratios since the dot-com era, the market reflects what Chris Senyek calls a “perfection scenario,” where the economic outlook continues to improve, while inflation stays tame. That may limit future returns, he said.

“Perfection is extremely difficult to attain,” Senyek, chief investment strategist at Wolfe Research, wrote in a note to clients earlier in the week. “We do believe that the next 10% move in U.S. equity markets is down, not up.”

And there’s no shortage of threats on the horizon. President Biden has proposed raising corporate taxes to fund his infrastructure bill, while the Federal Reserve is expected to consider rolling back part of its monetary stimulus later this year. Not to mention the pressure on profit margins that American businesses face from surging prices on everything from lumber to oil and computer chips.

In fact, either inflation or higher interest rates are cited as the biggest risk to equities in the latest survey that Evercore ISI conducted with investors and corporate clients. In the poll, released Friday, the proportion of respondents seeing the next 10% move in the stock market as being up has fallen to 51% from 66% in December.

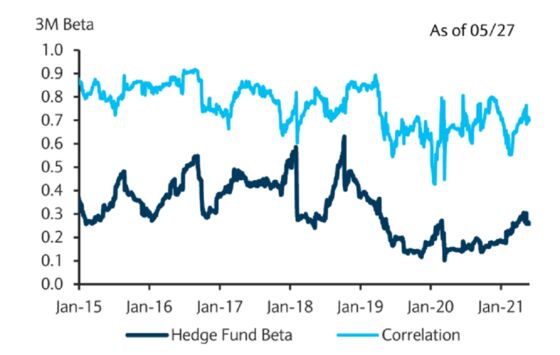

It’s not just investor sentiment that’s starting to crack. Investors are voting with their portfolios. Last month, exposure to equity futures for asset managers slipped from April’s post-pandemic peak, while hedge-fund exposure retreated from a two-year high, data compiled by Barclays show. Meanwhile, inflows to equity funds declined to $18 billion, a third of the average pace seen in the previous two months.

The S&P 500 and Nasdaq 100 each eked out a 0.6% gain over the holiday-shortened week, while the Dow Jones Industrial Average advanced 0.7%.

While movement at the index level was subdued, the retail hordes were furiously at work. AMC shares surged more than 80% for the second straight week and at one point the ailing movie-theater chain saw its market value surpass that of half the companies in the S&P 500.

That kind of blind buying is a sign that there is too much free money sloshing around the system and day traders are chasing winners regardless of fundamentals, according to Matt Maley, chief market strategist for Miller Tabak + Co.

“The action in AMC shows that today’s stock market is not a healthy one,” Maley said. “When the liquidity becomes less plentiful, as it looks like it is going to become in the not-too-distant future, there will be a reckoning.”

The question is, when that happens, will the broad market be able to hold up? For now, the S&P 500 has managed to withstand a series of mishaps, including the retail-fomented short squeeze on hedge funds in January, Archegos Capital Management’s blowup and the carnage in speculative stocks like unprofitable technology firms.

To Mike Wilson, chief U.S. equity strategist at Morgan Stanley, the market has entered a stage where growth is poised to weaken at the same time monetary and fiscal support slows, creating a backdrop that historically has led to lower multiples. The deflating process, which Wilson says already started among richly-valued shares during the first quarter, will spread to the rest of the market.

“Higher real rates and less ability to pass on higher prices would be a bad cocktail for multiples writ large,” Wilson wrote in a note. “Earnings revisions will not be able to offset that de-rating, leaving the overall market vulnerable to a 10-15% correction over the next six months.”

©2021 Bloomberg L.P.