A Declawed Fed Is All That Matters to a Lot of Bulls

A Declawed Fed Is All That Matters to a Lot of Bulls

(Bloomberg) -- You’ve heard all the warnings. Economic growth is wobbly, earnings estimates are down, the trade war rages on. From a vocal category of investors on Wall Street, a rebuttal: Who cares?

There’s no point worrying about stuff that failed to move stocks for years, when the one thing that has -- Jerome Powell’s Federal Reserve -- was beaten into submission. A corps of steadfast bulls has decided the only meaningful thing they’ve seen over the past five months is the triumph of doves at the central bank.

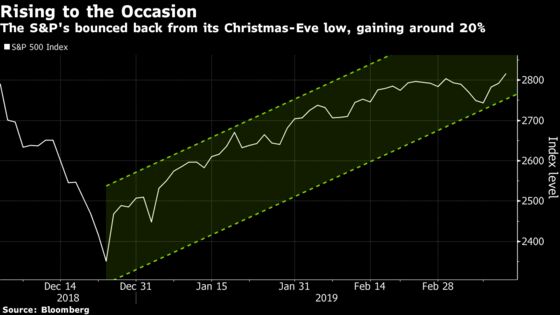

After all, it was only last September that Powell himself framed overheating asset prices as the biggest threat markets were likely to pose to the U.S. economy. Now, after a 10,000-point round-trip in the Dow Jones Industrial Average, asset prices are near where they began. What’s gone is any sense the Fed means what it says when it says it’s getting tough.

“At the end of the day, when push comes to shove, the Fed acquiesces to whatever the market’s view is,” said Brent Schutte, chief investment strategist at Northwestern Mutual Wealth Management Co., which manages about $125 billion. “Which is what happened. The Fed’s economic outlook I don’t believe changed all that much, but the market convinced them that they were wrong.”

Around Wall Street, they’re on board with the rally. Ned Davis Research upgraded U.S. stocks in early February, saying “don’t fight the Fed.” UBS Group AG’s Keith Parker forecasts stocks will reach new highs by June, citing a patient central bank. And Tony Dwyer at Canaccord Genuity expects a sustained market rally, giving significant credit to Powell’s pivot.

To be sure, it’s far from a unanimous view. DoubleLine Capital’s Jeffrey Gundlach said this week that stocks are in a bear market and will probably plunge back below last year’s Christmas Eve low at some point in 2019. Jerry Braakman, chief investment officer for First American Trust, shares the opinion.

“We still think we’re looking at a bear market here,” said Braakman, whose firm manages $1.5 billion. “When you look at what’s working in the market versus what’s struggling, we still see a setup where GDP is slowing, inflation is slowing.”

But neither is raging bullishness an outlier on Wall Street, which has shown itself willing to live with sluggish growth for a decade. Among 25 equity strategists tracked by Bloomberg, forecasts for end-of-year S&P 500 range as high as 3,250, roughly a 15 percent increase from now. Seven are at 3,000 or above.

At the crux of the debate is Powell’s willingness to acknowledge the market’s temper in moderating his hawkishness. He had a chance to stand firm in the face of fairly ordinary turbulence, and didn’t. In relenting, some critics warn, he’s diluted his ability to put a brake on upward volatility that will one day create a bubble.

It had been the risk of markets going berserk to the upside that had most visibly worried the Fed chairman prior to the end of last year. When the Fed raised rates for the first time under Powell’s purview, the chairman described “moderate vulnerabilities” by way of elevated asset prices. Back in September, Powell told business leaders equity prices were high, and while he didn’t see “high vulnerabilities,” prudence was warranted.

All that changed in January, when the chairman put new significance on market volatility -- some even designating sanguine stocks as the Fed’s “third mandate.” Various members have expressed comfort with inflation going considerably higher, with Powell saying Friday that “we need to make sure inflation doesn’t keep slipping” toward nothing.

“The message from the Fed -- that they’re going to tolerate an inflation overshoot -- that message will become more clear in the coming months,” said Ethan Harris, head of global economics research at Bank of America Merrill Lynch. “They’re in the process of reevaluating their framework. That’s a pretty friendly message out of the Fed.”

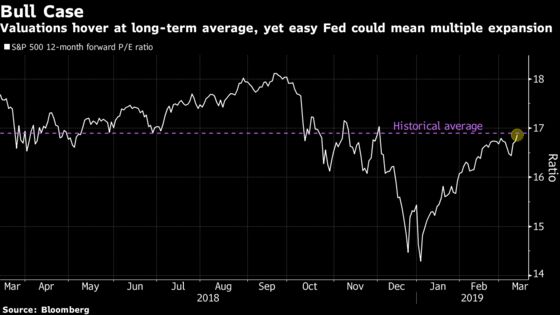

Equity valuations could expand mightily, some say. According to Nathan Thooft, Manulife Asset Management’s head of global asset allocation, it’s not unrealistic that stocks trade at a price-earnings ratio as high as 20 when financial conditions are this loose. With earnings for companies in the S&P 500 expected to come in at $167.50 a share this year, that results in an S&P 500 at 3,350, up 20 percent from current levels.

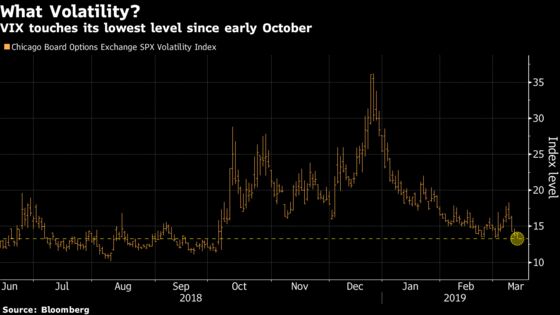

And while the stock rally paused last week, it’s back on now. The S&P 500 just saw three straight days of gains, the strongest advance since early February, with technology stocks again leading the way. The Cboe Volatility Index, or the VIX, is also down, touching the lowest levels since the start of October.

“More likely than not in my view the Fed is going to ignore inflation to an extent, and they’ll let it run hot,” Thooft said. “When you have a Fed turning as accomodative as they have, and the market’s perception being even more accommodative than they probably even are given where the Fed pricing is looking out the next 12 months, that typically warrants an environment where you would trade at a higher equity valuation.”

Of course, Powell has pivoted before, and may do it again.

“If we did see a situation where stock prices surged and credit spreads went down to levels that we saw pre-financial crisis, that would play a role in whether they would be open to hiking rates again,” said Ed Campbell, a managing director and portfolio manager for QMA. “We’ve seen with Chairman Powell that he is swayed by what’s happening in asset prices, at least in one direction. We’ll see going forward, if we ever do get a situation where things get bubbly on the upside, whether that plays a role in policy going forward.”

To contact the reporters on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.