‘Eventually It Just Snaps’: Strain Worsens on U.S. Profit View

Megacap U.S. Profit View Dimming and That's Not the Worst Part

(Bloomberg) -- Be it the trade war, slowing overseas growth or a less obvious catalyst, something is driving down U.S. earnings estimates. Smaller companies whose fate is bound closer to the economy are feeling it worse.

The declines are small but come week after week in data with a claim on being the most important plank in an equity bull case that is under assault everywhere else. Amid President Donald Trump’s tariff tweets and plummeting bond yields, profit estimates have for the most part resisted rolling over.

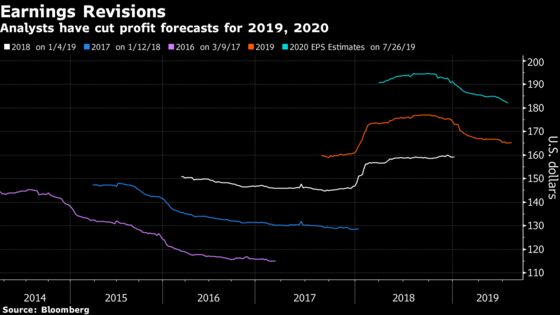

First the good news. Second-quarter results beat Wall Street forecasts and companies managed to post positive numbers on average. The issue is with longer-term projections. According to data compiled by Bloomberg, analysts now see combined S&P 500 earnings of $164.10 a share for 2019, down from $166.80 at the end of May. Next year’s forecasts have dropped to $181 from $184.80 barely three months ago.

“The trade war, all the political uncertainty -- it’s like you’ve got a twig and you’re bending it and it’s just bending, bending, bending,” Lori Calvasina, head of U.S. equity strategy at RBC Capital Markets, said in an interview at Bloomberg’s New York headquarters. “We all know what happens if we bend the stick too long. Eventually it just snaps and it just goes.”

Deeper skepticism is evident among small-cap companies, firms often considered insulated from trade issues due to their domestic orientation. Wall Street expected a weighted average 15.5% EPS growth for Russell 2000 companies this year, according to Calvasina, who calculated the data for profitable companies in the gauge. Come August, that estimate had fallen by almost two-thirds to 5.7%, according to her analysis.

A resolution to the trade war is still far off, Calvasina wrote in a note, and “further erosion of corporate confidence seems unavoidable.” Analysts are overly optimistic on 2020, she says, and after the U.S. and China exchanged tariff threats Friday she expects second-half earnings growth forecasts will need trimming again.

“There’s a negative feedback loop that’s starting to develop. You can absolutely see hints of it,” Calvasina said in an interview. Companies “are being cautious.”

Trade bombast is creating uncertainty for American companies, which steadily undermines earnings prospects for the second half of 2019, according to Bloomberg Intelligence. Growth ticked up slightly in the last quarter and forward guidance “hasn’t been very encouraging,” wrote analysts led by Peter Chung in a recent note.

The “earnings acceleration, which is anticipated for next year, needs to come through,” said Ed Clissold, chief U.S. strategist at Venice, Florida-based Ned Davis Research Inc. “If not, the market’s probably going to face a pretty tough 2020.”

The phenomenon isn’t new. Earnings estimates for 2019 hit a peak in September last year and have been deteriorating since, according to data compiled by Bloomberg Intelligence.

Strategists across Wall Street are slashing their forecasts. Citigroup analysts earlier this month trimmed their outlook for 2019 and next year, citing trade war threats and the overhang of a sluggish economy, among other things. UBS last week lowered its forecasts for the same period, warning that should tariffs rise to 25% in the basket holding mostly consumer goods, the drag could potentially wipe out most, if not all, of the forecast growth in 2020. The company’s global wealth management division said it holds an underweight position in stocks for the first time since the Eurozone crisis.

“We think a reduction in risk is prudent,” Mark Haefele, the firm’s chief investment officer, wrote in a note.

Smaller companies remain vulnerable as economic data deteriorate and risk of recession rises. Earnings results for the second quarter were weaker down the cap spectrum, with just a third of small-cap companies beating on both earnings and sales, according to Bank of America. The bank sees further downside risk to 2020 earnings growth.

The cautious sentiment is starting to translate into company actions. Companies are, by and large, decreasing their redeployment of cash for capital expenditures, a worrying sign for analysts. Corporate buyback rates are also falling and those that have focused on returning cash to shareholders through dividends and share repurchases have started losing their luster recently.

“It all has to do with confidence and uncertainty takes away confidence,” said Matt Maley, equity strategist at Miller Tabak & Co. “Until business confidence can pick up, we can only settle for mediocre growth, at best. At worst, we get a recession. Is that the kind of backdrop that gives investors confidence that we’ll move to new highs? It doesn’t.”

--With assistance from Sarah Ponczek and Wendy Song.

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi, Richard Richtmyer

©2019 Bloomberg L.P.