Masters of Equities Universe Are Unfazed by Spike in Bond Yields

Masters of Equities Universe Are Unfazed by Spike in Bond Yields

(Bloomberg) -- The recent rise in interest rates triggered a bout of volatility, but it’s not making the pros in the stock market run for the hills just yet.

Some of the world’s biggest fund managers say equities can persevere and continue rallying through the rise in government bond yields. They are focusing instead on prospects for a powerful economic and profit recovery.

In an informal Bloomberg News survey of more than 50 market players, most respondents including State Street Global Advisors and JPMorgan Asset Management said they’re monitoring the pace of the ascent in yields -- and the reasons for it -- rather than awaiting a particular level that will mark a breaking point for stocks. As long as central banks stick to accommodative policies, the equity bull run can power ahead, these investors say.

“Absent a shift in central banks’ thinking, we don’t think yields will rise to a level where it broadly hurts equities,” said Hugh Gimber, a London-based global market strategist at JPMorgan Asset Management. “Provided the Fed sticks to guidance, and remains comfortable, willing to look through any temporary spike in inflation, I don’t see an environment where yields are rising in a way that’s problematic for equities broadly.”

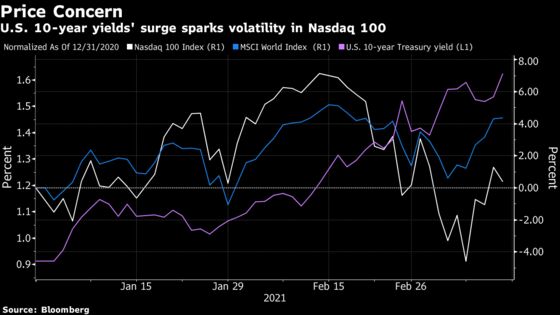

The surge in government bond yields over the past month helped fuel an exit from the frothier parts of the market such as technology and defensive shares, leading to a dip of as much 11% in the Nasdaq 100. But the vaccination push in major economies and bets on a recovery in economic growth as well as consumer spending are filling equity bulls with confidence that they can keep reaping returns despite higher interest rates.

At the same time, the pick-up in yields and the more than 70% rally in stocks from pandemic lows are pushing fund managers to become more selective. The likes of Manulife Investment Management and HSBC Asset Management say that, while this isn’t the time to exit equities, the selloff in bonds will accelerate the rotation out of the more expensive growth parts of the market and into cheaper and laggard equities that can benefit from the economic recovery.

“If rates were rising from a normal range, tech stocks would’ve been fine, but not true when the valuations are what they have been,” said Dave King, a Boston-based portfolio manager at Columbia Threadneedle Investments. “Potential reopening, coinciding with the rise in yields as well as other factors, were positive for the stocks that people didn’t like too much last year, whether it’s banks or energy.”

The energy sector is the best performer in the MSCI World this year, rising about 30%, while financials are next with a 14% gain. More defensive and rates-dependent sectors, such as consumer staples and utilities, are both in the red.

Cult stocks that have been investors’ favorites throughout the pandemic have also had a harsh few weeks. Tesla Inc. was down as much as 36% from its January peak before recouping some of its losses last week. Even market stalwart Apple Inc., the biggest U.S. stock, crashed as much as 19% from its record high.

This environment could also mark a shift from U.S. stocks to other international equities, such as Europe and emerging markets, that have higher exposure to value sectors. Having lagged the S&P 500 during last year’s rally from the March lows, the Stoxx Europe 600 is outpacing the American benchmark so far in 2021.

“The risk of an equity market correction driven by higher yields is highest in the U.S.,” said Joost van Leenders, an Amsterdam-based senior investment strategist at Kempen Capital Management. “The U.S. economy has recovered faster than the European economy, and another major fiscal stimulus bill has just been approved. Inflationary pressure in Europe looks minimal. From a style perspective, growth is more at risk than value. This also means Europe may benefit relative to the U.S.”

Investors who are watching out for a particular Treasury yield level that can significantly hurt global equities pointed to a range between 2% and 3% for 10-year bonds.

“It’s important to remember that historically, rising yields have been consistent with rising markets, because both are driven by growth, and we think that will remain the case this time,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. At the same time, he added that “yields above 2.25-2.5%, if not accompanied by an improvement in the long-term earnings growth outlook and lower risk premia, would start to make current equity valuations look more challenged.”

The pause in the bond market selloff in the middle of the week last week showed how quickly stocks and growth sectors can come rushing back. The Nasdaq 100 on Tuesday surged 4% for its biggest jump since November, signaling that appetite for tech names remains strong.

“If the rise in bond yields is too quick or too high, it’s a negative for equity valuations. However, if controlled and modest over time, equities can absorb the adjustment reasonably well,” said Nathan Thooft, Boston-based global head of asset allocation at Manulife Investment Management. “Especially if the reason for higher rates is better growth rather than just higher inflation.”

©2021 Bloomberg L.P.