Asia’s Worst Currency Is Diverging From the Local Bond Market

Indonesia’s currency and bond markets are on divergent paths this quarter.

(Bloomberg) -- Indonesia’s bond and currency markets, risk benchmarks that tend to move in tandem, are diverging in signs that the nation’s pandemic response is deterring global funds.

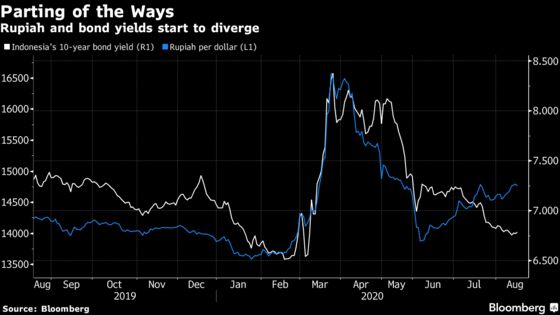

The rupiah is the worst-performing Asian currency this quarter while the nation’s benchmark sovereign bond is outperforming peers. The two markets are usually aligned due to heavy foreign debt holdings.

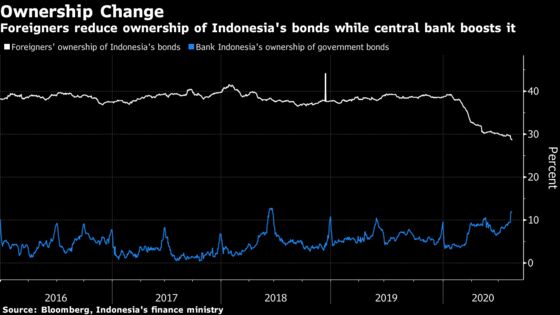

That dynamic started changing as massive borrowings by the government to fund pandemic-recovery stimulus spurred Bank Indonesia to take the unusual step of monetizing debt. Offshore holdings of the nation’s bonds dropped to 29% this month, the lowest since 2012, from as high as 39% at the start of the year, according to data compiled by Bloomberg.

“Fund flow data show that the external inflows into Indonesian sovereigns haven’t really come back as most of the rupiah bond subscriptions have been by domestic entities,” said Yanxi Tan, a foreign exchange strategist at Malayan Banking Bhd. in Singapore. “It’s certainly not supportive for the rupiah.”

Global funds have net sold more than $7 billion worth of Indonesian debt this year, the second-highest in emerging Asia this year after India. While that would normally have driven up borrowing costs, Bank Indonesia has stepped into the breach buying some 300 trillion rupiah ($20.3 billion) of bonds.

Domestic ownership has also risen as local banks bought more sovereign debt after a series of rate cuts lowered their incentive to lend, according to Philip McNicholas, Asean FX and rates strategist at Bloomberg Intelligence.

The result? The benchmark 10-year yield has dropped over 50 basis points in the current quarter, but the rupiah is down 3.6% against the dollar.

The divergence could continue. In the Aug. 14 budget announcement, President Joko Widodo said that the government will ramp up spending to a record high next year and seek the central bank’s help in financing a budget deficit. That raises concerns that BI’s debt monetization, which was supposed to be a temporary measure, may extend into next year.

The ratio of foreign ownership in Indonesian debt could slide further given the government will be looking to build up liquidity in the new 5-year and 10-year bonds, according to McNicholas. “The lines BI has been purchasing as part of burden sharing are deemed tradable, which very likely means they too are being counted in the aggregate number,” he added.

Still, less foreign ownership could have a silver lining for the rupiah.

“Reduced reliance on hot money flows would mean reduced volatility in rupiah markets as well, which would make it easier for authorities to monitor and manage sentiment,” Maybank’s Tan said.

©2020 Bloomberg L.P.