Markets Take the Lead When It Comes to Factoring in Recession

Many financial markets are already signaling that the U.S. is more likely than not hurtling toward recession.

(Bloomberg) -- Many financial markets are already signaling that the U.S. is more likely than not hurtling toward recession. But will they prove prescient or overly fretful?

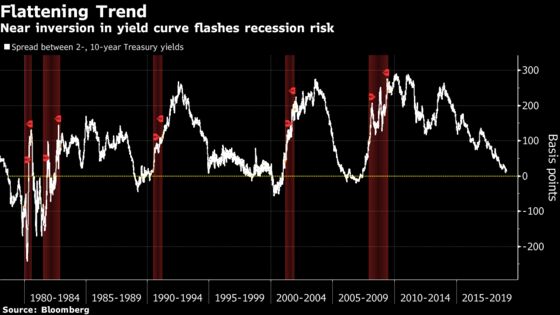

The prospect of a widespread yield inversion in the Treasury market, which has preceded U.S. downturns for more than half a century, has generated the most alarm and is edging even closer to fruition. When falling yields are combined with the declines since the third quarter in stocks and commodities, as well as investment-grade and junk-rated corporate debt, it suggests about a 50 percent probability of an economic contraction within a year, according to JPMorgan Chase & Co.

“The markets have already priced in a lot of downside risk,” said Nikolaos Panigirtzoglou, a JPMorgan global markets strategist in London.

How investors react going forward remains a major question.

Here’s what other markets are indicating:

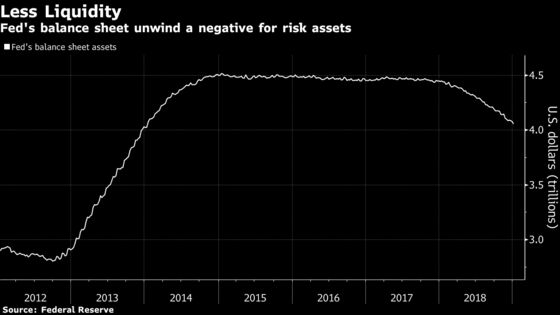

Riskier assets from stocks to credit took a hit late in 2018, while Treasury yields rose as the Federal Reserve looked intent on plowing ahead with its hiking cycle and tightening liquidity even amid signs of ebbing output. While a blockbuster jobs report for December and the Fed signaling a pause in tightening has helped to reverse some of those moves, the threat of trouble still looms.

“Liquidity from central banks has tightened significantly, China is more on the slowdown side of things, and the Trump administration won’t be as aggressive on fiscal stimulus as before,” said Kokou Agbo-Bloua, global head of flow strategy and solutions at Societe Generale SA, which predicts a 2020 downturn. “All the drivers for the bull run we’ve had in risky asset over the past five years are pretty much gone.”

Bank of America’s recession indicators have also jumped noticeably in recent weeks, even as their analysts say the economic data doesn’t show that. One gauge in particular that takes into account movements in the S&P 500 Index and the spread between 3-month and 10-year Treasury yields points to a 64 percent chance of recession over the next year. Goldman Sachs Group Inc.’s market-based model puts recession odds at 50 percent, which is well above the 15 percent probability their economists see for a contraction over the next year.

By some measures, the stock market was the most divorced from the economy in 30 years during the December rout. But since the Christmas Eve meltdown, equities have staged a 10 percent rebound, making some investors wondering a bottom has been found. JPMorgan’s Panigirtzoglou, who says it is most likely that only a mild recession eventually takes place, sees the degree risk-assets have already priced in a contraction as “a bullish message” for equities, high-grade credit and commodities.

“The fundamentals are changing, but not as bad as what the market seems to be pricing in,” said Aaron Clark, a portfolio manager at Boston-based GW&K Investment Management managing $36 billion. “The one risk was that could change, and maybe all this pessimism turns into a self-fulfilling prophecy, and the equity-market and asset-price declines have contagion to the real economy.”

To Rich Guerrini, chief executive officer of PNC Investments, it’s too early for recession talk and he says there’s a “strong case for equities.”

Earnings should grow by about 7 percent this year, even as companies lower guidance and U.S. economic output is set to increase 2.5 percent.

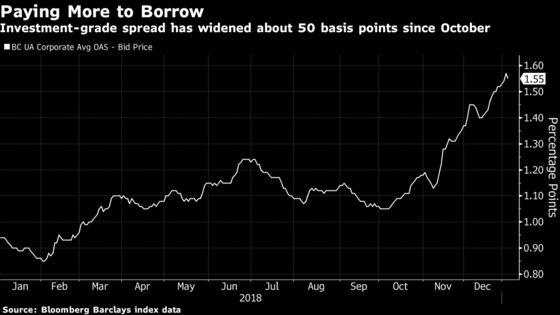

Investment-grade credit spreads over government debt yields widened nearly 50 basis points in the final three months of 2018 as trade tensions added to the mix of other concerns, making the securities one of the worst-performing U.S. asset classes last year.

Distressed-debt money manager Marc Lasry has warned that more pain may be coming and it could be severe. Meanwhile, Guggenheim Partners Chief Investment Officer Scott Minerd has cut his credit exposure to the lowest since the financial crisis. He fears that sustained liquidity constraints could give way to systemic risk.

To Doug Peebles, chief investment officer of fixed income at AllianceBernstein LP, a U.S. or global recession is not a foregone conclusion, and he sees major economies only slowing in 2019. Relatively higher yields for both government debt and credit present opportunities, he said in a Jan. 8 blog post.

“We’re more upbeat on credit markets now than we were for most of 2018," Peebles said in an interview, adding that it’s much more likely that Europe has a recession than the U.S. in 2019.

High-yield debt has been recovering from the convulsions suffered in November and December, and has become one of the best-performing asset class with year-to-date returns of about 3 percent. Leveraged loans and investment-grade bonds are also showing signs of recovery, and all three markets were able to back up strong secondary trading with well-received new issuance.

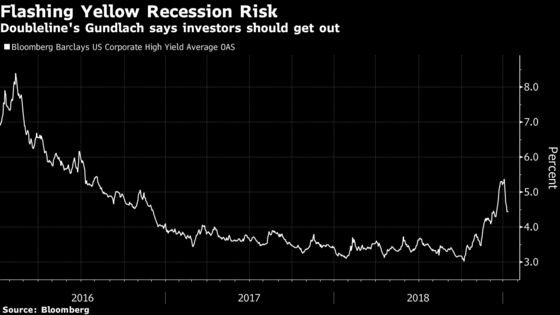

The Bloomberg Barclays High Yield Index just had its best weekly gains in almost a decade. The debt’s yield premium over Treasuries has narrowed from a three-year high earlier this year. But DoubleLine Capital’s Jeffrey Gundlach, who was prescient a year ago with his 2018 calls, isn’t convinced, and says investors should stay clear of junk bonds.

--With assistance from James Crombie and Gowri Gurumurthy.

To contact the reporters on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net;Sarah Ponczek in New York at sponczek2@bloomberg.net;Molly Smith in New York at msmith604@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Dave Liedtka

©2019 Bloomberg L.P.