Markets May Not Need a Deal, But Don't Want War

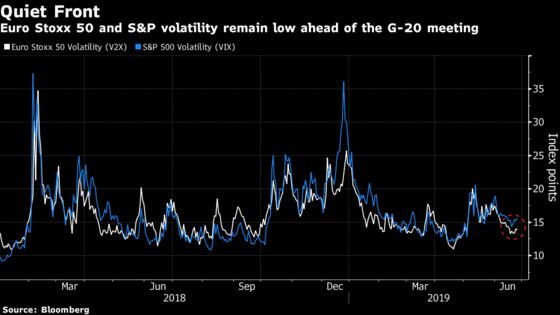

In an eerie calm, stock volatility remains low for both the S&P 500 and the Euro Stoxx 50 ahead of the G-20 meeting.

(Bloomberg) -- With geopolitical tensions and trade fears simmering, all the action is in havens as nervous investors pile up on gold and Swiss francs. The overall market may be resilient for now, but unresolved economic and political issues could still hit confidence and corporate earnings.

In an eerie calm, stock volatility remains low for both the S&P 500 and the Euro Stoxx 50 ahead of the G-20 meeting between U.S. President Donald Trump and China’s Xi Jinping, during a strong month for equities. Europe’s benchmark and the S&P 500 have gained 5% and 6%, respectively in the period.

“I’ve been surprised at how benign the market environment has been during this year so far, given the amount of stuff that’s going on in the wider economic and geopolitical context, both here and internationally,” says Ken Wotton, a fund manager at Gresham House in London. “I just find it very hard to believe there won’t be periods where sentiment, risk appetite retracts and there’s more volatility in the market.”

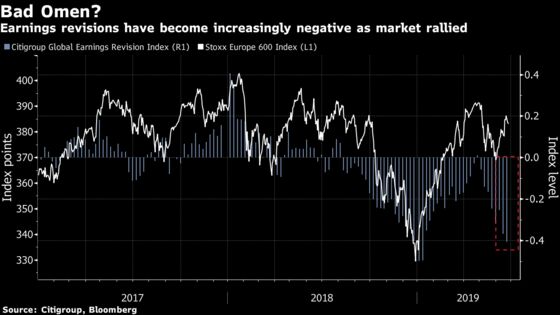

The market’s composure jars with the lack of confidence from analysts, who have been cutting earning estimates as much as in January, according to Citigroup’s earnings revisions index.

The worries are visible in investment flows, though. Bank of America Merrill Lynch’s clients have been net sellers of U.S. stocks in the past week for the first time in seven weeks, in a possible effort to freeze gains ahead of the G-20 summit, the bank’s strategists say. During the past five weeks, foreign-exposed sectors saw bigger outflows than domestics, they add.

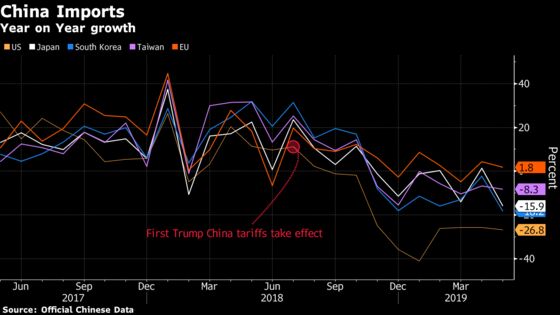

The market may have learned to live with trade tension, counting on dovish central bank policies to act as a cushion, but it doesn’t change the fact that global commerce has been reshaped by tariffs and disputes. China’s imports from Japan, South Korea and the U.S. fell 16%, 18% and 27% respectively last month from a year ago. Those from the European Union are still growing (+1.8%), but at a much slower pace.

That’s also why the Trump-Xi meeting matters, even if a deal is unlikely. UBS Wealth strategists don’t expect any breakthrough on trade, nor extra tariffs immediately. Their base-case scenario is for a prolonged truce between the U.S. and China that would likely extend or consolidate the stock rally. But a breakdown would thump economies and markets, they say.

In the meantime, Euro Stoxx 50 futures are trading down 0.3% ahead of the open.

- Watch tobacco firms after San Francisco became the first U.S. city to pass a ban on e-cigarettes. Watch British American Tobacco and Imperial Brands.

- Watch chipmakers after U.S. group Micron Technology beat earnings expectations and said it has resumed making some shipments to China’s Huawei. Watch Infineon, STMicroelectronics and AMS after U.S. peers rallied.

- Watch oil stocks as crude prices jumped after a report suggesting stockpiles in the U.S. have continued to shrink, and tensions with Iran showed no sign of abating.

- Watch the pound and U.K. stocks after no-deal has also moved to the center of the debate between the two candidates for prime minister, with front-runner Boris Johnson proposing two exit strategies that the EU has already rejected.

- Watch the bond market pricing increasingly lower interest rates. This 100-year bond yields just over 1%, highlighting just how desperate investors are for returns.

COMMENT:

- “Rate cuts/QE, assuming sufficient and timed correctly, would seek to avoid a deep recession and underpin economic growth,” Citi stratetegists write in a note. “We advise taking a step back and asking why (Central Banks) intervention is required? Because all is not well. And it is not just the deepening negative impact of trade wars, many economies were already struggling to grow. Yes, CB stimulus can drive a risk asset rally but cyclical and structural headwinds remain (read Japanification, growing populism, weak bank profitability and capital return uncertainty).”

COMPANY NEWS AND M&A:

- Natixis’s H20 Funds Hemorrhage $6.4 Billion as Crisis Deepens

- UBS CEO Says He Feels a ‘Biting Headwind’ From Swiss Regulators

- Yara Lifts Div Target to 50% Net Income; Widens Improvement Plan

- Schneider Electric Confirms FY and 2021 Targets

- Mediobanca, J.C. Flowers Said in Talks for Julius Baer’s Kairos

- Self Storage Offering Prices 13m Shares at NOK19.25/Share

- Renault’s Senard Said No Discussions W/ Fiat Ongoing Now: Echos

- DSV Extends Panalpina Offer Until July 17 From June 26

- Autos: Europe’s Tough New Emissions Rules Come With $39 Billion Threat

- TechnipFMC Agrees to Pay $301.3 Million to Resolve Bribery Case

- EDP Agrees to Sell EU470m of 2019 Tariff Deficit to Tagus

- DIA Reaches Restructuring Agreement With Syndicated Lenders

- EQT Said to Seek Sept. IPO Valuing Company at EU7b: Borsen

NOTES FROM THE SELL SIDE:

- Buzzi Unicem fundamentals have kept improving since Morgan Stanley assumed coverage in May, and with valuation also turning more favorable plus an upside consensus risk, stock is upgraded to overweight from equal-weight.

- Efficient and well-run U.K. water companies will remain attractive even if there is a significant step-down in allowed regulatory returns, Jefferies says in a note initiating coverage of the sector. Severn Trent started at buy, United Utilities and Pennon at hold.

- The balance of risk for Jupiter Fund Management looks to be moving toward the upside, with flows starting to stabilize even if investment performance remains a little mixed, Peel Hunt says in note, upgrading stock to buy.

- Berenberg raised Adidas to buy from hold, with 53% increase in PT to EU315 (the highest among analysts tracked by Bloomberg), with broker citing overly conservative consensus estimates and a 20% discount to Nike.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 392.7 (July 2018 high); 397.9 (May 2018 high)

- Support at 381.4 (50-DMA); 374.5 (61.8% Fibo)

- RSI: 56.9

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,514 (May high); 3,596 (May 2018 high)

- Support at 3,411 (50-DMA); 3,403 (61.8% Fibo)

- RSI: 58.7

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Adidas upgraded to buy at Berenberg

- Buzzi Unicem raised to overweight at Morgan Stanley; PT 20 Euros

- Jupiter upgraded to buy at Peel Hunt

- Novo Nordisk Upgraded to Buy at SEB Equities; PT 385 Kroner

- Salvatore Ferragamo upgraded to hold at Jefferies; PT 21 Euros

DOWNGRADES:

- BBVA downgraded to sell at SocGen; PT 4.30 Euros

- Eland Oil & Gas cut to hold at Panmure Gordon; PT 1.35 Pounds

- Ted Baker downgraded to sector perform at RBC

INITIATIONS:

- Aena rated new buy at Berenberg; PT 215 Euros

- Aeroports de Paris rated new hold at Berenberg; PT 135 Euros

- Elis rated new overweight at Morgan Stanley; PT 19 Euros

- Flughafen Wien rated new buy at Berenberg; PT 46 Euros

- Fraport rated new sell at Berenberg; PT 57 Euros

- Pennon rated new hold at Jefferies; PT 7.70 Pounds

- Securitas rated new underweight at JPMorgan; PT 145 Kronor

- Severn Trent rated new buy at Jefferies; PT 23.40 Pounds

- United Utilities rated new hold at Jefferies; PT 8.70 Pounds

- Zurich Airport rated new sell at Berenberg; PT 151 Francs

MARKETS:

- MSCI Asia Pacific down 0.3%, Nikkei 225 down 0.7%

- S&P 500 down 0.9%, Dow down 0.7%, Nasdaq down 1.5%

- Euro down 0.07% at $1.1359

- Dollar Index up 0.15% at 96.28

- Yen down 0.22% at 107.44

- Brent up 1.7% at $66.1/bbl, WTI up 2.1% to $59/bbl

- LME 3m Copper down 0.4% at $6015/MT

- Gold spot down 1.1% at $1408.3/oz

- US 10Yr yield up 2bps at 2.01%

ECONOMIC DATA (All times CET):

- 8:45am: (FR) June Consumer Confidence, est. 100, prior 99

- 10am: (IT) 1Q Deficit to GDP YTD, prior 2.1%

- 10:30am: (UK) May UK Finance Loans for Housing, est. 41,000, prior 42,989

* For a daily wrap on developments in European equity capital markets, click here

--With assistance from Lisa Pham.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.