European Earnings Are Pretty Good, Except for Energy

European Earnings Are Pretty Good, Except for Energy

(Bloomberg) --

Not so bad. That’s the view of most strategists examining the European earnings season. As we approach the reporting period’s final stretch, the picture isn’t as grim as initially feared as most sectors are actually delivering growth. But overall, the region is in an earnings recession and looking forward, companies may struggle to meet expectations for the fourth quarter and for next year without some improvement on the macro-economic front.

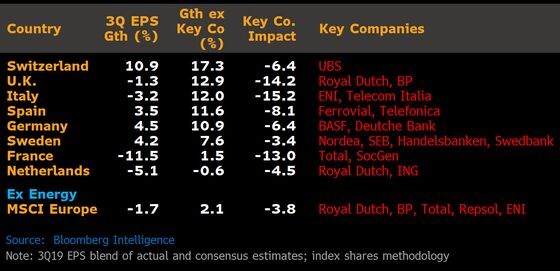

We recently highlighted that Europe might have recorded profit growth in the third quarter if it hadn’t been for the energy sector. Bloomberg Intelligence strategists even show that without a few “bad apples” in each country, companies posted a decent beat.

The table below is pretty clear: energy stocks and financials provided the bulk of the earnings drag. The problem with those laggards is that they carry a heavy weight in indexes. For example, BP and Royal Dutch Shell make up almost 16% of the FTSE 100.

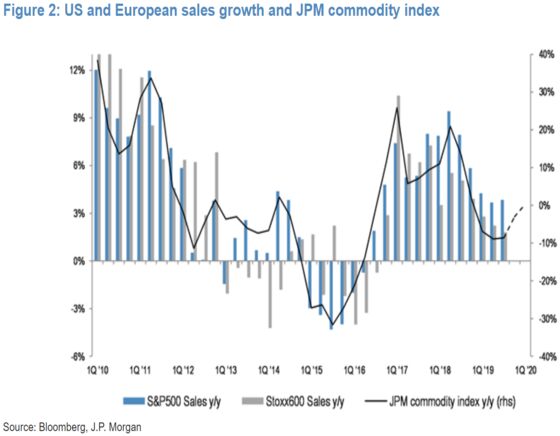

Aside from energy, earnings have not only been brighter than consensus expectations, but also better than that implied by feeble Purchasing Managers’ Index economic data, JPMorgan strategists say.

They also point out that overall, sales growth is 2% year-on-year, which is particularly encouraging given the fall in commodity prices. This is usually a “good lead indicator for revenue growth.” The top line could pick up further, provided that commodity prices stay at current levels or bounce back, JPMorgan says.

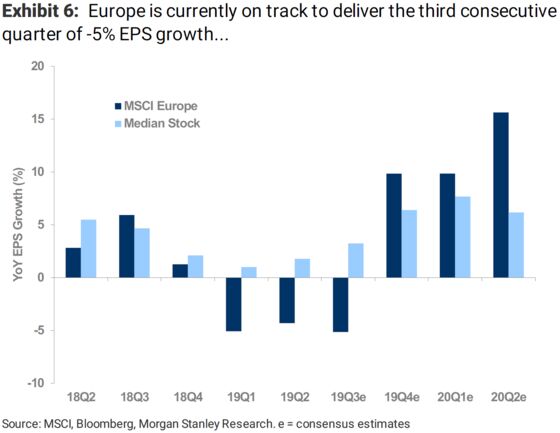

Not everyone is so keen though. Morgan Stanley strategists say the earnings beat has been of “low quality,” and that companies on the MSCI Europe Index are on track to deliver a third consecutive quarter of negative earnings growth on average. Most of all, they struggle to see the validity of the consensus at this stage, with analyst expectations of 10% earnings-per-share growth for the next two quarters and full-year 2020. We probably haven’t seen the end of the earnings downgrades yet.

In the end, as a potential positive outcome on the trade front looks increasingly priced in, it may all come down to the macro improvement. JPMorgan strategists expect European PMIs to follow the improvement in money supply and China export orders, noting that global manufacturing PMIs have been stable for three months. The Stoxx Europe 600 ignored the deterioration in the figures this year and now the composite PMI has stabilized just above the contraction zone. As for Europe’s manufacturing index, the picture is gloomier as shown below.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.