A Market Linchpin Blamed for Repo Chaos Says It’s Not Culpable

The repo market became unhinged because of technical catalysts and maybe because the Federal Reserve misjudged liquidity needs.

(Bloomberg) -- A major support beam in the U.S. financial system’s infrastructure is pushing back against accusations that a program it created to safeguard the repo market exacerbated last year’s chaos in short-term lending.

Hedge funds are increasingly financing investments using repurchase agreements, through a centrally cleared platform created by Depository Trust & Clearing Corp. That trend “compounded the strains” in short-term lending, fueling the enormous mid-September spike in repo rates, the Bank for International Settlements argued in a recent report.

The repo market -- where those who need cash to finance positions meet those with money to lend -- became unhinged because of technical catalysts and possibly because the Federal Reserve misjudged liquidity needs. DTCC’s sponsored-repo program, in which DTCC serves as the ultimate counterparty in each deal, was also on the list of potential catalysts. But Murray Pozmanter, who’s guided DTCC’s efforts to ensure repo from worsening a future financial crisis like it did in 2008, says that’s way off base.

“We don’t think that cleared repo, or the sponsored program in particular, was either the cause of or had any impact on the severity of the repo-market volatility that we saw in September,” Pozmanter, DTCC’s head of clearing agency services, said in an interview. “It gives dealers balance-sheet relief and reduces systemic risk.”

Lehman Brothers Holdings Inc.’s demise more than a decade ago nearly froze the repo market, a major reason why the ensuing financial crisis was so severe. Through its sponsored-repo system, DTCC has been trying to get more transactions centrally cleared, ensuring there’s a pile of money set aside to back up trades if any market participants fail.

Growth of the sponsored program contributed to the turmoil in September by concentrating funding risk in overnight transactions rather than longer-term -- aka term -- ones, Credit Suisse Group AG analyst Zoltan Pozsar said in November.

An imbalance between those needing overnight funding and those willing to provide it came to a head on Sept. 17, when overnight general collateral rates spiked to a record high of 10% from around 2% days before. While the sponsored program always allowed for term agreements, various factors -- most related to the accounting for a counterparty default -- caused dealers to resist engaging beyond overnight.

Actions by the Fed since September, including operations that temporarily boost liquidity and others that permanently lift reserves in the banking system, have calmed repo markets. The overnight general collateral repo rate is now around 1.6%.

The Fed after the 2008 crisis pushed industry participants to take steps that dimmed systemic risk in repo, and has deemed more central clearing as one avenue for that. While an array of clearing houses tried to play a role, DTCC has been the only one able to do so.

A central counterparty clearinghouse, or CCP, pools members’ capital to ensure losses at one firm don’t harm others -- a kind of firewall from catastrophe. The CCP is ultimately the counterparty for every trade, removing risk tied to a member default. The DTCC, through its Fixed Income Clearing Corp. unit, runs the only platform for repo central clearing.

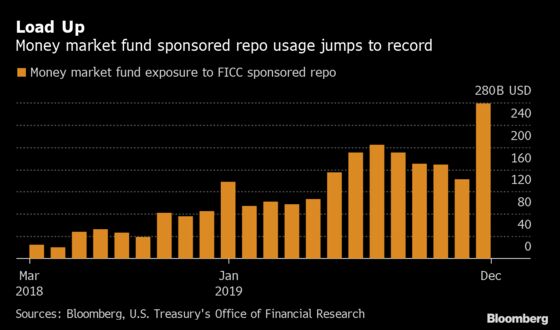

FICC, through its sponsored program, was in December counterparty to about $279 billion of money-market mutual funds’ repo transactions, according to Office of Financial Research data. That was about double the amount seen a year earlier.

DTCC has long served as the CCP for repo between dealers, but in recent years added new venues such as the sponsored program to bring in other firms like asset managers and hedge funds. As the name implies, it allows FICC members to bring in, or sponsor, those who aren’t CCP members. It currently has 12 sponsors, and about that many will probably be added in the next six months.

Teresa Ho, a strategist at JPMorgan Chase & Co., says sponsored repo didn’t cause September’s repo problems. What’s more, she says the program has helped expand the market’s capacity after dealers had stepped back amid the weight of post-crisis regulations. Going through the CCP allows banks to net similar cash lending against borrowing, vanquishing the repo fingerprint on their balance sheet.

“Sponsored repo has been very effective and has been a very good way for dealers to provide liquidity to the market in a balance-sheet-efficient way,” Ho said. “There is capacity for sponsored repo’s size to double from where it is now.”

The U.S. Securities and Exchange Commission is reviewing an FICC rule change that removed purported hurdles to term repo lending. But Pozmanter doesn’t think that will lead to a big shift away from overnight repo lending, which he says backs his thesis that DTCC wasn’t to blame for September. SEC approval should come by the end of February, Pozmanter said.

“I’m very curious to see what happens when this rule filing is approved,” he said. “A large majority of what has been going through the sponsored-program as overnight would be going through repo as overnight anyway, even if it wasn’t being cleared by us. Overall, sponsored repo has been a very, very useful tool for the marketplace.”

--With assistance from Stephen Spratt.

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Nick Baker, Mark Tannenbaum

©2020 Bloomberg L.P.