Market Correction May Be About Half Over, JPMorgan Estimates

The S&P 500 Index climbed Friday in wake of a jobs report that showed hiring continues though at a softer pace.

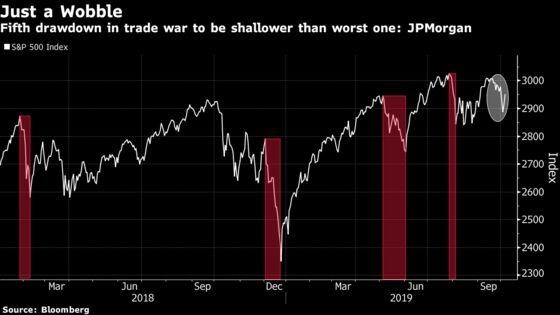

(Bloomberg) -- A range of indicators including investor positioning before the most recent slump in markets suggests that the drawdown is about half finished, and will prove to be less painful than the rout last December, according to JPMorgan Chase & Co. analysis.

“Since corrections tend to be largest when markets are expensive and over-owned and when market depth is poor, these indicators give a sense of vulnerability even if they cannot anticipate the timing of a random shock,” John Normand, head of cross-asset fundamental strategy at JPMorgan, wrote in an Oct. 4 note. “Entering October, vulnerabilities were moderate rather than high.”

While the S&P 500 Index climbed Friday in wake of a jobs report that showed hiring continues though at a softer pace, stocks Tuesday and Wednesday saw the first back-to-back drops of more than 1% this year thanks to a panoply of weakening data. U.S. futures fell again in London Monday.

“A recession is avoidable but recurring drawdowns are not,” Normand wrote. That’s thanks to President Donald Trump’s “impulsiveness and the scope for miscalculation when wielding untested policy tools like tariffs, export bans and capital flow restrictions,” he said.

Though the S&P 500 has -- just barely -- escaped entering down-20%, bear territory since the market ructions that began in early 2018, there’s been a cumulative toll from the episodes of pain since then, JPMorgan highlighted. The total return for the index in that period is less than 2 percentage points more than for cash.

| Asset | Total return Since Jan. 26, 2018 |

|---|---|

| U.S. investment-grade bonds | 12.15% |

| U.S. Treasuries | 11.04% |

| U.S. high-yield bonds | 6.97% |

| S&P 500 | 6.31% |

| Vanguard money-market fund | 3.68% |

| Stoxx Europe 600 (in euros) | 1.43% |

| MSCI emerging market stocks | -17.57% |

| Source: Bloomberg |

Ahead of the current drawdown, JPMorgan analysis shows that positioning was “reasonably neutral-to-defensive.” As for valuations, a multi-asset portfolio showed that the “overshoot” relative to what global growth normally implies was only modest, Normand wrote. Meantime, market depth -- or the degree of reliance on just a small group to drive gains -- is “below average” for U.S. stocks, but with positioning not extreme poses less of a worry, he concluded.

“The message across all indicators is that this correction is about half complete, and should prove much shallower than last year’s,” Normand wrote.

He cautioned that “the great rotations many hope for,” such as out of bonds and into equities, or from developed markets to emerging ones and defensive shares to cyclicals, would probably take a major impetus. Think much more Federal Reserve easing, a rollback in tariffs or sizeable fiscal stimulus from the likes of Germany and China.

To contact the reporter on this story: Christopher Anstey in Tokyo at canstey@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Joanna Ossinger

©2019 Bloomberg L.P.