Market Angst Is Off the Charts Even for the Day of a Fed Meeting

Market Angst Is Off the Charts Even for the Day of a Fed Meeting

(Bloomberg) -- Days when the Federal Reserve announces monetary policy are often times of heightened anxiety for financial markets. Wednesday’s has instilled even higher stress.

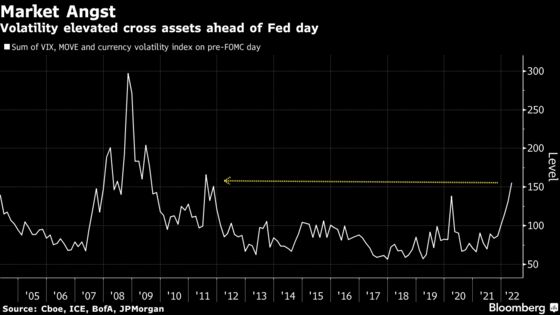

From stocks to bonds and currencies, turbulence is running very high heading into the event, when the central bank is widely expected to raise benchmark interest rates by 50 basis points, the first such move since 2000. Across assets, implied volatility just rose to levels not seen for any pre-Fed session in more than a decade.

Jitters are everywhere after equities and bonds had their worst concerted monthly selloff since the global financial crisis while the dollar surged to a 20-year high. While the turmoil builds a case that the Fed has succeeded in the cause of transparency, the speed and duration of future hikes remain murky. A question looming large for investors is whether the tightening in financial conditions will be fast enough to cool the economy.

“If the answer to that question is no –- economic growth remains well above trend –- financial conditions need to tighten more,” said Dennis DeBusschere, the founder of 22V Research. “Although the moves in nominal and real 10yr yields and the USD have been dramatic, the concern is that they can keep going if the U.S. economy doesn’t slow further.”

Such is the landscape facing investors: With central bankers embarking on a campaign to tackle inflation that is running at a four-decade high, the Fed has quickly transformed from ally to enemy.

The consequences are evident in derivatives markets across assets. At Tuesday’s close, the Cboe Volatility Index, or VIX, a gauge of costs for the S&P 500 options, was about 10 points above its long-term average. The ICE BofA MOVE Index, a similar gauge for Treasuries, hovered near highs hit at the height of the crisis in March 2020. The same was true of the JPMorgan Global FX Volatility Index.

Combined, the total of the three volatility measures surpassed where it was the day before any Fed policy announcement since 2011.

In the past, a low-inflation environment allowed the FOMC to “repeatedly reverse course at the first sign of market volatility, which became standard operating procedure.” said Michael O’Rourke, chief market strategist at JonesTrading. “Today, the central bank is so far behind the curve on inflation policy that it can’t reverse course anytime soon.”

Since Fed chair Jerome Powell raised rates in March for the first time in three years, most major financial assets have fallen in value. Down 4.4% over the span, Treasury bonds endured the worst intra-meeting decline since at least 1997. Corporate credit sold off too, with investment grade losing 5.1%, while high yield debt slipped around 3%.

Stocks initially bounced, only to follow fixed income lower. All told, the S&P 500 dropped more than 4% over the stretch.

Alongside a jumbo rate hike, the Fed is expected to set a date for the start of its quantitative tightening, or QT, that will see it reduce the balance of its bond holdings. At stake is a booming economy that has become the bedrock of corporate earnings.

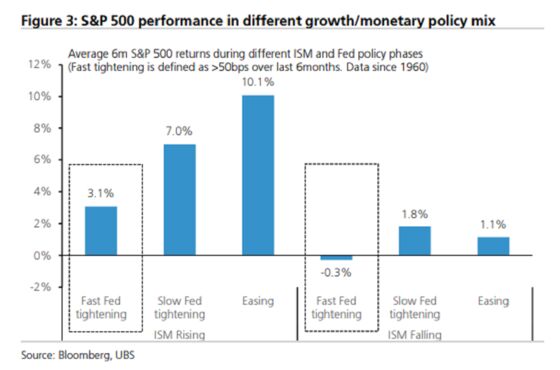

During fast tightening cycles like this, whether growth can hold up makes a big difference for stock investors. Using Institute for Supply Management’s gauge of factory activity as a proxy for economic growth, UBS Group AG strategists led by Keith Parker found that since 1960, the S&P 500 have tended to fall at an annualized rate of 0.6% when ISM declined. By contrast, when ISM rose, the market fared better, rallying roughly 6%.

“The big question for investors is whether economic growth can keep up, supporting equity earnings and a low corporate default rate,” said Lauren Goodwin, economist and portfolio strategist at New York Life Investments. “In our view, it’s too early to be sure that ‘peak hawkishness’ has passed.”

A record increase in employment costs in the first quarter has prompted money-market traders to ramp up the expected pace of 2022 tightening to about 2.6 percentage points from now until year’s end. On Friday, the Labor Department will release its monthly jobs report for April that will shed new light on wage growth.

While Fed Chair Powell has expressed confidence in engineering a soft landing in the economy, recession talks are again creeping up with stock losses deepening in April. To Goldman Sachs Group Inc. strategists led by Dominic Wilson, a recession is far from inevitable and is more likely beyond the next 12 months.

“If that is right, then the pattern we have seen so far this year will probably continue: with equities punching lower and then recovering at least partially as long as recession fails to materialize, and the rates and commodity curves continuing to move higher over time,” the strategists wrote in a note. “For that reason, a period of easing financial conditions again sowed the seeds of its own demise.”

©2022 Bloomberg L.P.