Man Group Dials Up Short Bets as Turkey Stirs Fragile Five Fears

Man Group Dials Up Short Bets as Turkey Stirs Fragile Five Fears

(Bloomberg) -- The market meltdown following Turkey’s central-bank shakeup is reviving a longtime debate among the world’s largest money managers and Ivy League economists over the vulnerability of developing nations.

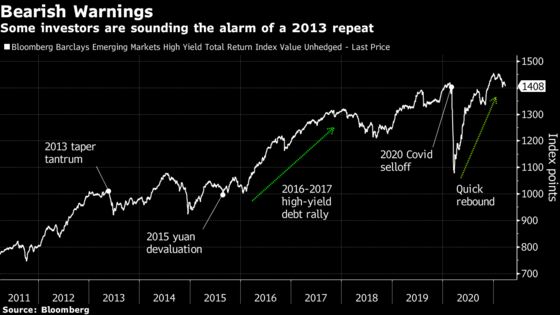

Doomsayers including Man Group Plc, the world’s biggest publicly listed hedge-fund firm, and the Institute of International Finance’s chief economist Robin Brooks warn that the turmoil battering Turkish securities could ripple across emerging markets in a repeat of the 2013 taper tantrum. Yet that gloomy scenario isn’t the dominant narrative in the hallways of Pacific Investment Management Co., BlackRock Inc. and Ashmore Group Plc, which have some of the largest exposures to the nations that might be next in the crosshairs.

“With Turkey beginning to crack, we see significant fragility being under-priced in a number of emerging-market countries,” Man GLG money managers including Patrick Kenney and Santiago Pardo wrote in a report, citing an immediate opportunity to short Turkey, Brazil, Mexico and South Africa.

Brooks, who previously led currency strategy at Goldman Sachs Group Inc., said the combination of U.S. fiscal stimulus and rising Treasury yields makes it harder for developing nations to finance investment. The fact that Turkey and Brazil, two of the largest emerging markets, are taking a hit only elevates the contagion risk, he said. His colleague, Sergi Lanau, added that South Africa also looks vulnerable, particularly with its high fiscal deficit.

‘Fragile Five’

That cautious approach proved a winning formula in 2013 and 2018, when Morgan Stanley’s “Fragile Five” of Turkey, Brazil, South Africa, India and Indonesia suffered. But bulls were vindicated by the rally in high-yield debt from 2016 to 2017 and again by last year’s rebound.

To Ashmore’s Gustavo Medeiros, the risk of contagion is negligible because Turkey’s unorthodox policy stance differs from most developing nations.

The prospect of a weaker dollar, surging commodity prices and rebounding global growth make for a rosier backdrop than in 2013, which may favor the bulls once again, according to Whitney Baker, the New York-based founder of Totem Macro, which advises funds overseeing more than $3 trillion.

“People are anchoring to what happened during the last large yield move -- the Taper Tantrum -- even though conditions are different in pretty much every way,” she said. “As with anything that’s virtually never been cheaper, I think it’s extremely poor risk-reward to short the yielders at this stage.”

BlackRock’s positioning suggests the same. Strategists including Wei Li and Elga Bartsch wrote that the firm is “moderately overweight” global high-yield debt, citing its allure in a yield-starved world. The New York-based money manager is also overweight emerging-market equities and neutral on local debt, which they said could benefit from a stable-to-weaker dollar.

Credit risks are confined to smaller developing nations with low index exposure, such as Romania and Colombia, Lupin Rahman, the London-based head of emerging-market sovereign credit at Pimco, wrote in a report. Meantime, the International Monetary Fund will probably increase its special drawing right allocations this April, boosting many high-yielding emerging markets with low reserves, she said.

Still, some developing nations face the same dilemma as eight years ago: In order to shore up their currencies, they must raise interest rates and impose lending restrictions at the expense of growth. Unlike 2013, they’re also juggling a global pandemic and all the spending needs that have come with it.

Fund Exposure

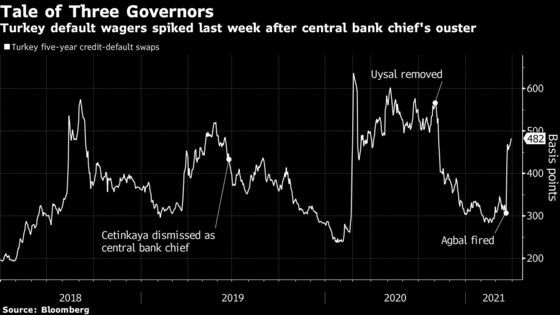

In Turkey, the central-bank governor’s rate-hike strategy cost him his job, sparking a selloff in the lira and the biggest one-week spike in Turkish default wagers since 2008. Funds managed by Pimco, BlackRock and FMR LLC, which are the largest reported holders of the country’s debt, were among the most prominent losers, according to data compiled by Bloomberg.

Pimco holds about $3.7 billion of Turkish bonds across the funds it manages, totaling 1.9% of the nation’s outstanding debt, the data show. BlackRock and FMR own 1% and 0.6% of the bonds, respectively. Still, their losses were spread across many investment vehicles, limiting the damage to any one fund.

Many international funds avoided the drama in Turkey by trimming their exposure well in advance. These days, a minority of investors are overweight the country, even as its benchmark weight has declined. Turkey represents 4.0% of the Bloomberg Barclays Emerging Markets Hard Currency Aggregate Index and just 0.3% of the MSCI Emerging Markets Index.

Here’s a look at exposure to debt from some of the higher-yielding countries:

| Holder Name | Turkey ($196b) | Brazil ($918b) | Mexico ($470b) | South Africa ($234b) |

|---|---|---|---|---|

| Pimco | 1.9% | 0.4% | 0.2% | 1.1% |

| BlackRock | 1.0% | 0.3% | 0.6% | 0.8% |

| FMR | 0.6% | 0.1% | 0.2% | 0.1% |

| Ashmore | 0.1% | 2.1% | 0.1% | 0.3% |

* Holdings data capture the percentage of a nation’s aggregate debt held by a particular firm, according to the latest fund filings compiled by Bloomberg.

©2021 Bloomberg L.P.